Answered step by step

Verified Expert Solution

Question

1 Approved Answer

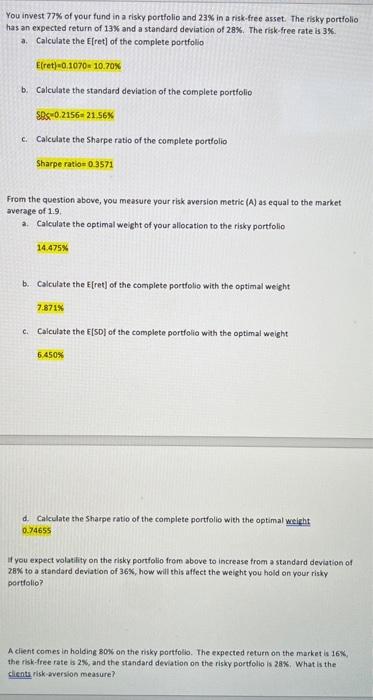

Need help with the last parts of the question please You invest 77% of your fund in a risky portfolio and 23% in a risk-free

Need help with the last parts of the question please

You invest 77% of your fund in a risky portfolio and 23% in a risk-free asset. The risky portiolio has an expected return of 13% and a standard deviation of 28%. The risk-free rate is 3%. a. Calculate the [iret] of the complete portfolio b. Calculate the standard deviation of the complete portfolio SBK=0.2156=21.56K c. Calculate the Sharpe ratio of the complete portfolio From the question above, you measure your risk aversion metric (A) as equal to the market average of 1.9 . 2. Calculate the optimal weight of your allocation to the risky portfolio b. Calculate the E[ret] of the complete portfolio with the optimal weicht 7.871% c. Caiculate the E[SO] of the complete portfolio with the optimal weight 6.450% d. Cakculate the Sharpe ratio of the complete portfolio with the optimal weicht 0.74655 If you expect volatility on the risky portiolio from above to increase from a standard deviation of 28K to a standard deviation of 36K, how will this affect the weight you hold on your risky portiolio? A client comes in holding 80x on the risky portfolio. The expected return on the market is 16X, the risk-free rate is 2%, and the standard deviation on the risky portfolio is 28%. What is the clicnts risk-wersion measure Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Tidy Finance With R

Authors: Christoph Scheuch, Stefan Voigt, Patrick Weiss

1st Edition

1032389346, 978-1032389349