Answered step by step

Verified Expert Solution

Question

1 Approved Answer

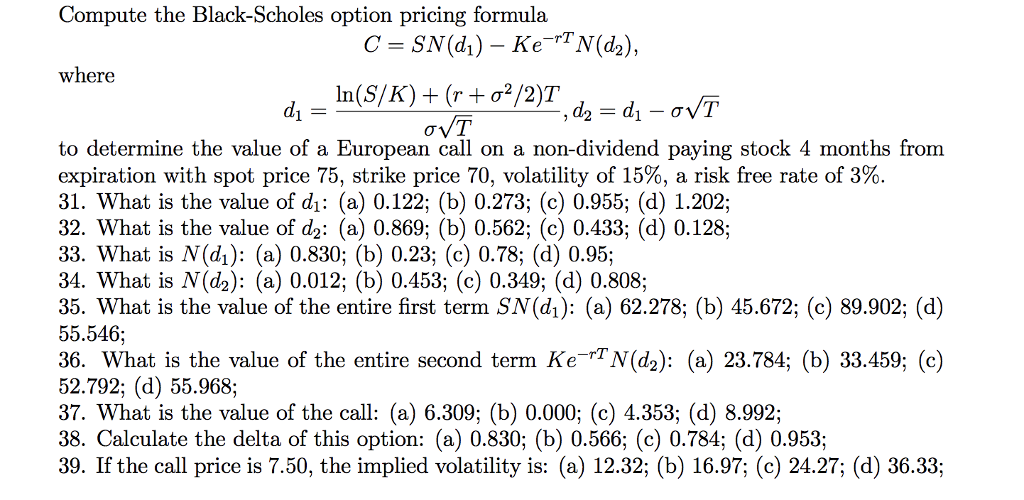

need help with these questions. Compute the Black-Scholes option pricing formula where to determine the value of a European call on a non-dividend paying stock

need help with these questions.

Compute the Black-Scholes option pricing formula where to determine the value of a European call on a non-dividend paying stock 4 months from expiration with spot price 75, strike price 70, volatility of 15%, a risk free rate of 3%. 31. What is the value of di: (a) 0.122; (b) 0.273; (c) 0.955; (d) 1.202; 32. What is the value of d2: (a) 0.869; (b) 0.562; (c) 0.433; (d) 0.128; 33. What is N(di): (a) 0.830; (b) 0.23; (c) 0.78; (d) 0.95; 34. What is N(d2): (a) 0.012; (b) 0.453; (c) 0.349; (d) 0.808; 35. What is the value of the entire first term SN(di): (a) 62.278; (b) 45.672; (c) 89.902; (d) 55.546; 36. What is the value of the entire second term Ke TN(d2): (a) 23.784; (b) 33.459; (c) 52.792; (d) 55.968; 37. What is the value of the call: (a) 6.309; (b) 0.000; (c) 4.353; (d) 8.992; 38. Calculate the delta of this option: (a) 0.830; (b) 0.566; (c) 0.784; (d) 0.953; 39. If the call price is 7.50, the implied volatility is: (a) 12.32; (b) 16.97; (c) 24.27; (d) 36.33Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Energy Finance And Economics Analysis And Valuation Risk Management And The Future Of Energy

Authors: Betty Simkins, Russell Simkins

1st Edition

1118017129, 978-1118017128