Answered step by step

Verified Expert Solution

Question

1 Approved Answer

need help with this Part III Phased-in Reduction Complete Part IIf only if your taxable income is more than $164,900 but not $214,900 ( $164,925

need help with this

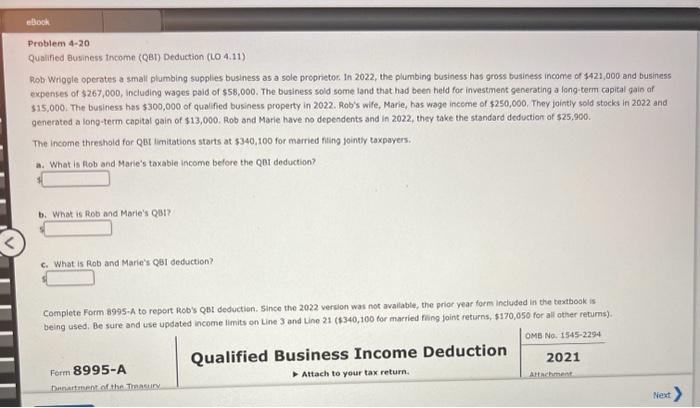

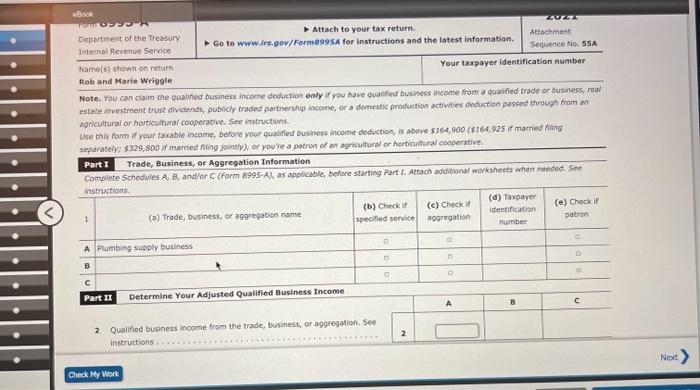

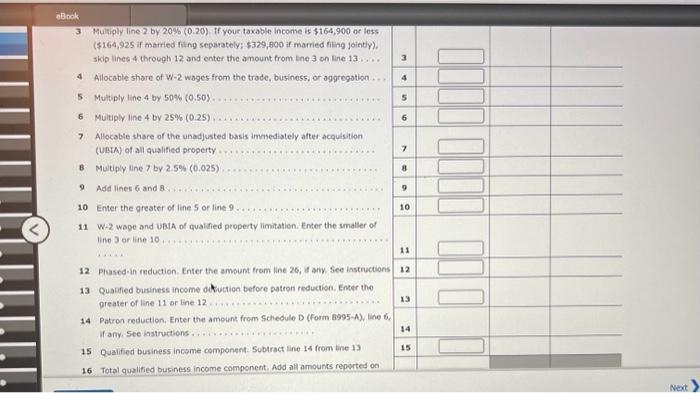

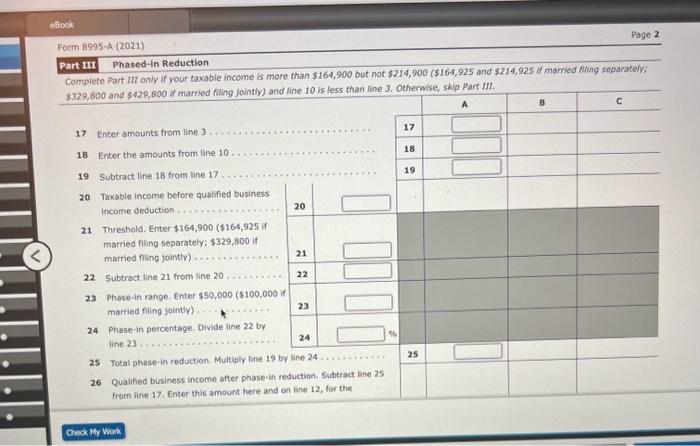

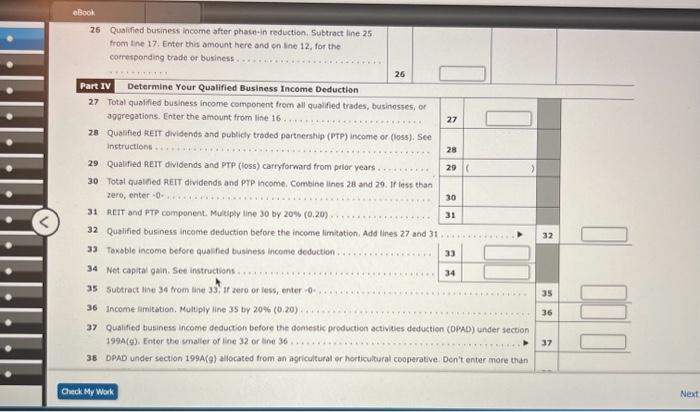

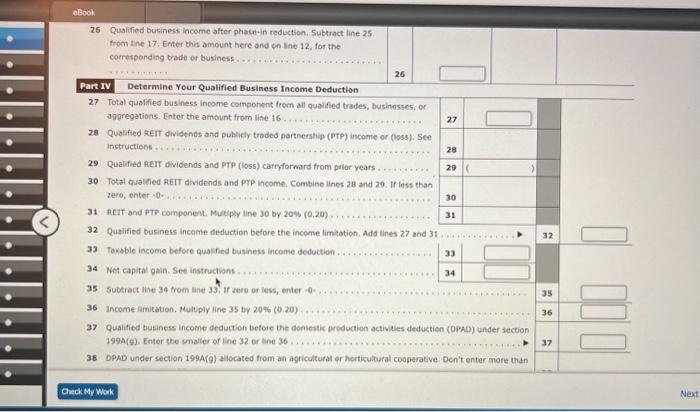

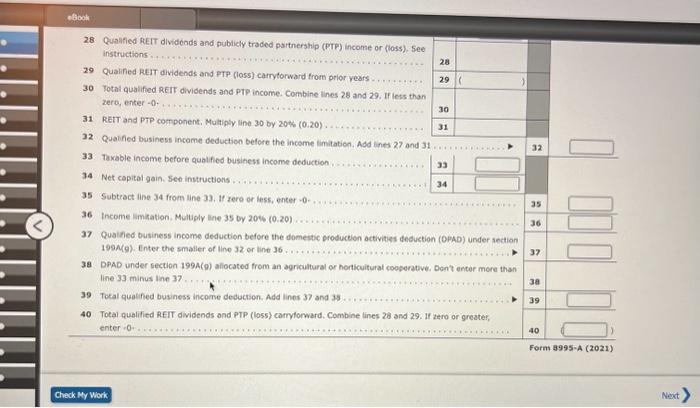

Part III Phased-in Reduction Complete Part IIf only if your taxable income is more than $164,900 but not $214,900 ( $164,925 and $214,925 if married fwing scparately: 3 Ruitiply line 2 by 20%(0.20), If your taxable income is $164,900 or less (\$164,925 if married fithy separately: $329,800 if married filing jointly). skip lines 4 through 12 and enter the anount from lne 3 on line 13... 4 Allocable share of W-2 wages from the trade, business, or aggregation. 5. Multiply tine 4 by 50%(0.50) 6 Multiply line 4 by 25%(0.25) 7 Allocable share of the unadjusted basis immediately after acquisition (UBLA) of all qualified property B Multiply line 7 by 2.5%(0.025) 9 Add lines 6 and 8 . 10 Enter the greater of line 5 or line 9 11 W-2 wage and UBIA of qualined property limitation. Enter the smaller of line 3 or line 10 12. Phased-in reduction. Enter the amount from line 26, if any See instructions 13 Qualfied business income atuction before patron reduction, Enter the preater of line 11 or line 12 . 14 Patron reduction, Enter the amouns from Schedule D (form B995-A), line 6 . if any, See instructions 15 Qualified business income component. Subtract line 14 from line 13 16 Total qualified business income component. Add all amounts reported on Qualified Business trucome (QBI) Deduction (LO 4.11) Rob Wriggle operates a small plumbing supplies business as a sole proprietoc. In 2022, the plumbing business has gross business income of $421,000 and business expenses of $267,000, including wages paid of $8,000. The business sold some land that had been heid for investment generating a long-term capital gain of \$15,000. The business has $300,000 of qualified business property in 2022. Rob's wife, Marie, has wage inceme of $250,000, They jointly sold stocks in 2022 and generated a long-term capital gain of $13,000. Rob and Marie have no dependents and in 2022, they take the standard deduction of $25,900. The income threshold for QBt limitations starts at 5340,100 for married filing fointly taxpayers. a. What is Rob and Marie's taxabie income before the got deduction? b. What is Rob and Marie's QB? c. What is Rob and Marie's Qeil deduction? Complete Form 8995A to report Rob's QB! deduction. Since the 2022 version was not avaliable, the prior year form inctuded in the textbook is being used, Be sure and use updated income limits on Line 3 and Line 21 (\$340,100 for married fing foint returns, $170,050 for all other retums). 25 Qualified business income after phasto-in reduction. Subtract line 25 from tine 17. Enter this amount here and on line 12, for the correrponding trade or business. 26 Part IV Determine Your Qualified Business Income Deduction 27. Total qualified business income component from all quaified trades, businosses; of apgregations. Enter the amount from line 16. 28 Qualfied REIT dividends and publidy traded partnership (PTP) income or (loss). See instructions 29 Qualified RET dividends and PTP (loss) carryforward from prior vears 30 Total qualfed PEIT dividends and PTP income. Combine lines 28 and 29 . If less than zero, enter - 0 - 31 R.IT and PTP component. Multipty line 30 by 20%(0.20) 32 Qualified business income deduction before the income limitation, Add lines 27 and 31 33 Toxable income before quasined business income deduction 34 Net capital gain. See instructions. 35 Subtract line 34 from line 334, It zero or iess, enter -0 - 36 Income lamitation. Multiply line 35 by 20%(0.20) 37 Qualified business income deduction before the domestic production activies deduction (OPAD) under section 199A(g). Enter the smaller of line 32 or line 36 36. DPAD under section 199A(9) allocated from an agricultural or horticultural cooperative. Den't enter more than Creck wy Wak 25 Qualified business income after phasto-in reduction. Subtract line 25 from tine 17. Enter this amount here and on line 12, for the correrponding trade or business. 26 Part IV Determine Your Qualified Business Income Deduction 27. Total qualified business income component from all quaified trades, businosses; of apgregations. Enter the amount from line 16. 28 Qualfied REIT dividends and publidy traded partnership (PTP) income or (loss). See instructions 29 Qualified RET dividends and PTP (loss) carryforward from prior vears 30 Total qualfed PEIT dividends and PTP income. Combine lines 28 and 29 . If less than zero, enter - 0 - 31 R.IT and PTP component. Multipty line 30 by 20%(0.20) 32 Qualified business income deduction before the income limitation, Add lines 27 and 31 33 Toxable income before quasined business income deduction 34 Net capital gain. See instructions. 35 Subtract line 34 from line 334, It zero or iess, enter -0 - 36 Income lamitation. Multiply line 35 by 20%(0.20) 37 Qualified business income deduction before the domestic production activies deduction (OPAD) under section 199A(g). Enter the smaller of line 32 or line 36 36. DPAD under section 199A(9) allocated from an agricultural or horticultural cooperative. Den't enter more than Creck wy Wak Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Freedom

Authors: Timothy Turner

1st Edition

1801573573, 978-1801573573