Answered step by step

Verified Expert Solution

Question

1 Approved Answer

need project note on all The following data is also given - Corporation Tax Rates China India USA 25% 34% 40% Currency Exchange Rates 1

need project note on all

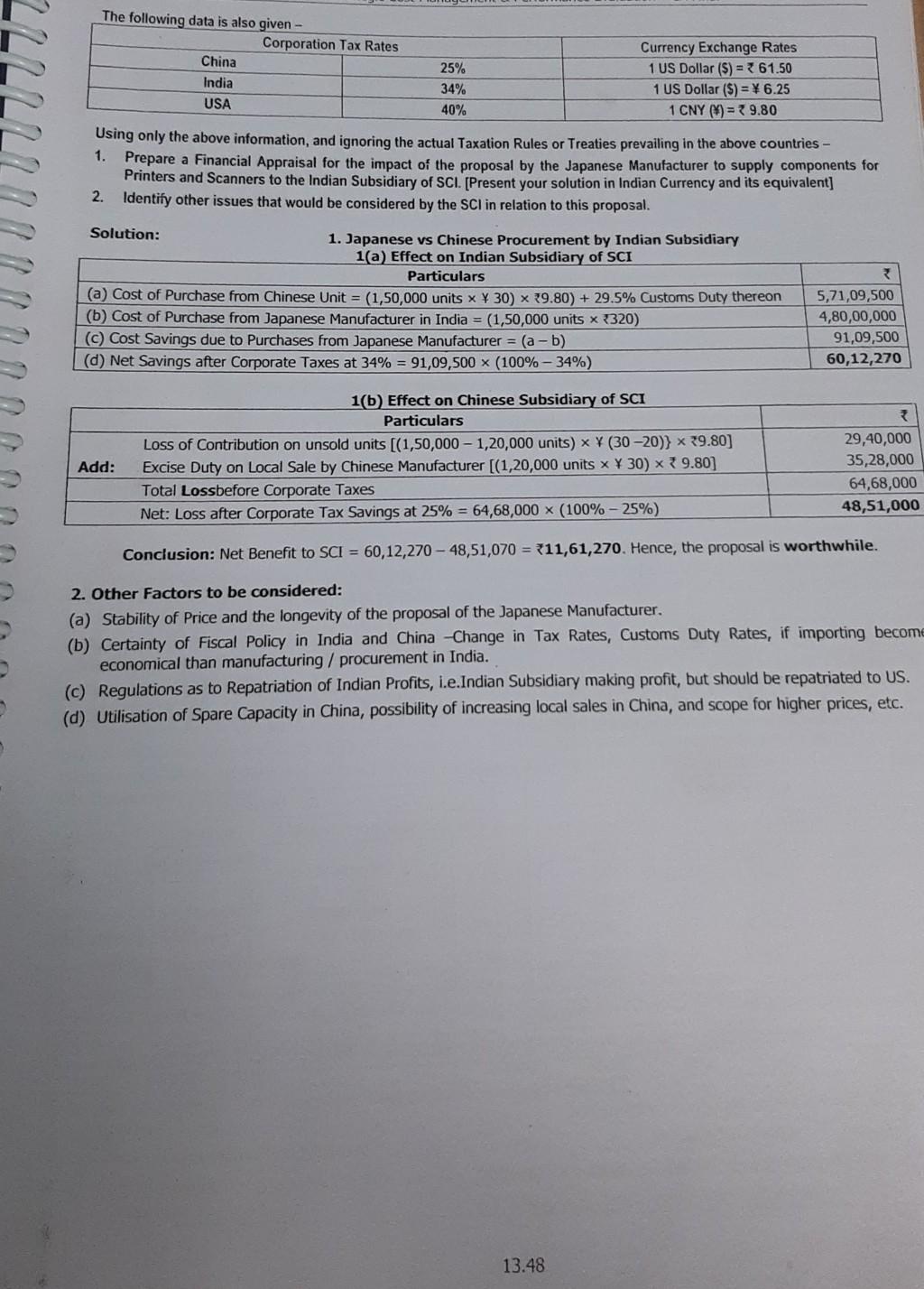

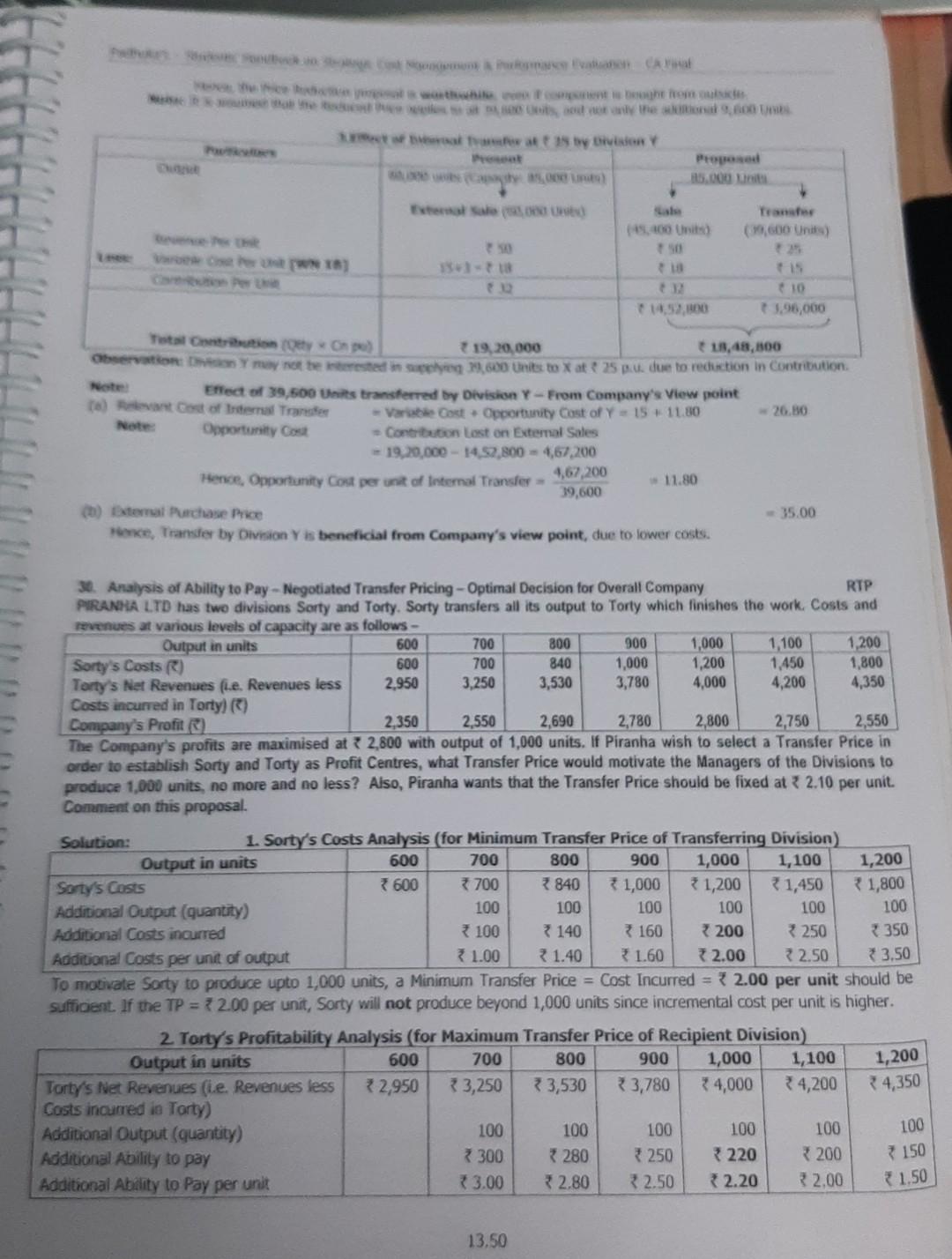

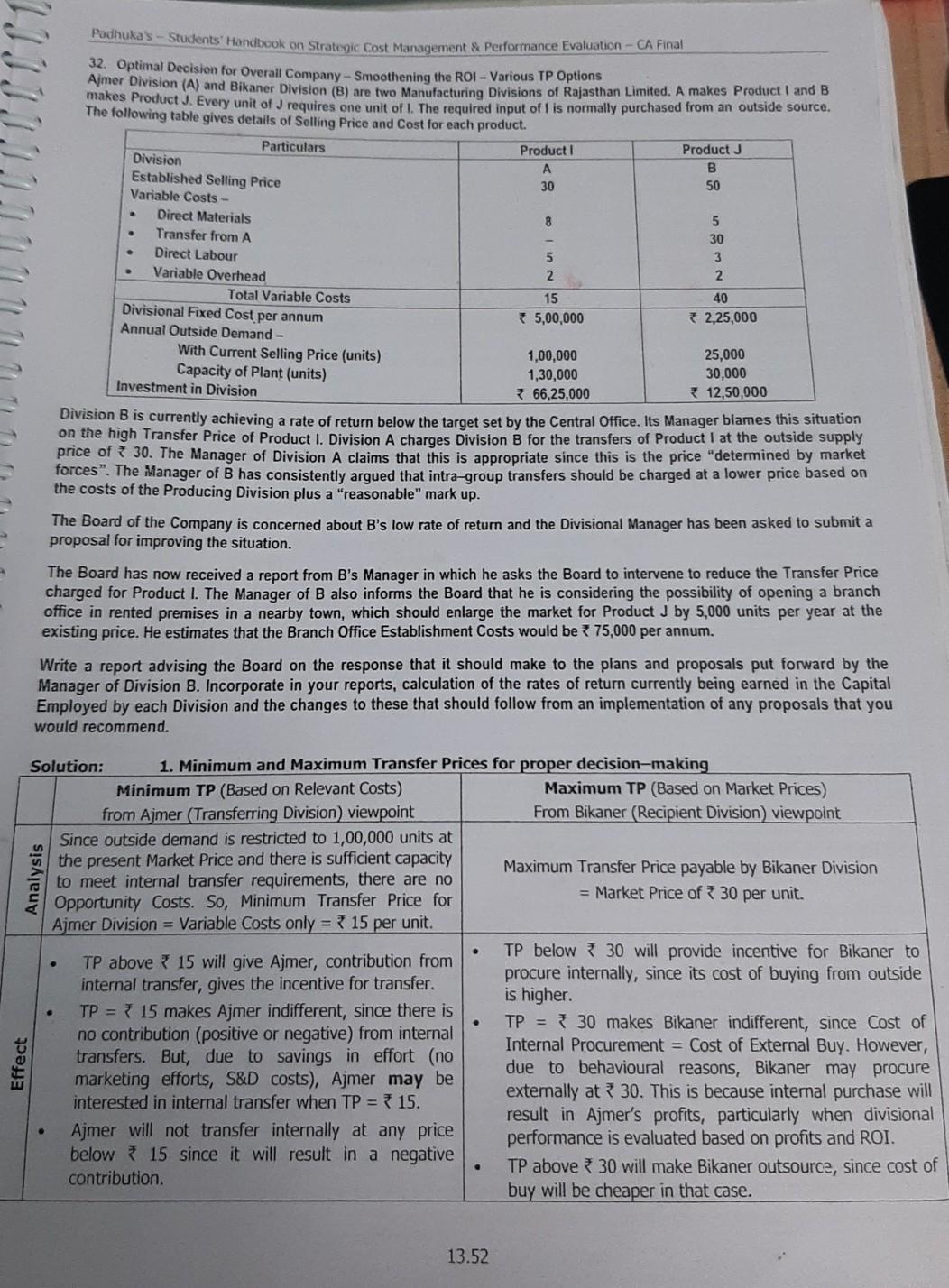

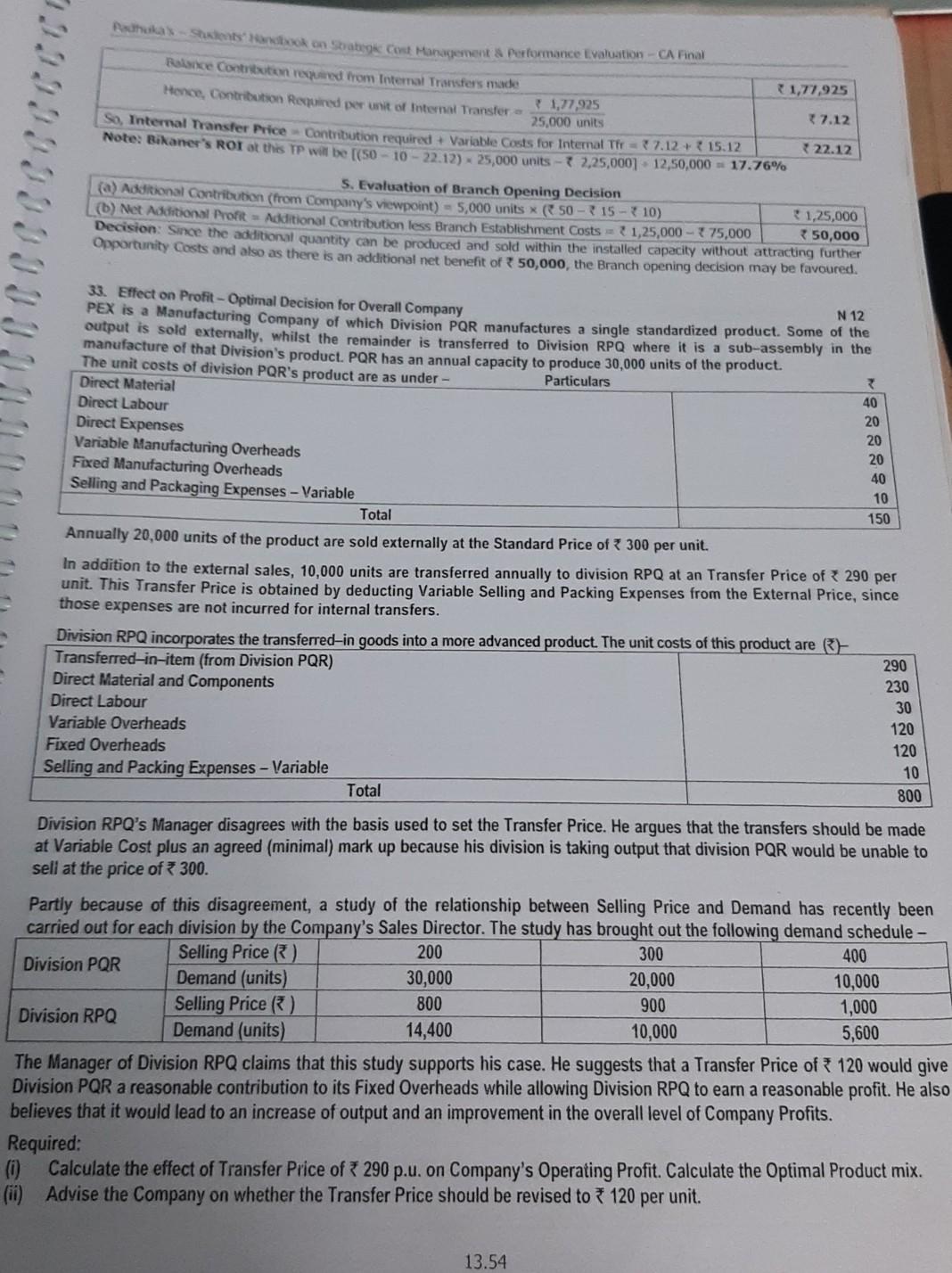

The following data is also given - Corporation Tax Rates China India USA 25% 34% 40% Currency Exchange Rates 1 US Dollar ($) = 61.50 1 US Dollar ($) = \6.25 1 CNY () = 9.80 1. Using only the above information, and ignoring the actual Taxation Rules or Treaties prevailing in the above countries - Prepare a Financial Appraisal for the impact of the proposal by the Japanese Manufacturer to supply components for Printers and Scanners to the Indian Subsidiary of SCI. [Present your solution in Indian Currency and its equivalent] 2. Identify other issues that would be considered by the SCI in relation to this proposal. Solution: 1. Japanese vs Chinese Procurement by Indian Subsidiary 1(a) Effect on Indian Subsidiary of SCI Particulars (a) Cost of Purchase from Chinese Unit = (1,50,000 units x 30) x 19.80) + 29.5% Customs Duty thereon (b) Cost of Purchase from Japanese Manufacturer in India = (1,50,000 units x 8320) (c) Cost Savings due to purchases from Japanese Manufacturer = (a - b) (d) Net Savings after Corporate Taxes at 34% = 91,09,500 X (100% -34%) 2 5,71,09,500 4,80,00,000 91,09,500 60,12,270 Add: 1(6) Effect on Chinese Subsidiary of SCI Particulars Loss of Contribution on unsold units [(1,50,000 - 1,20,000 units) * (30 -20)} * 29.80) Excise Duty on Local Sale by Chinese Manufacturer [(1,20,000 units X 30) x 9.80] Total Lossbefore Corporate Taxes Net: Loss after Corporate Tax Savings at 25% = 64,68,000 X (100% - 25%) 29,40,000 35,28,000 64,68,000 48,51,000 Conclusion: Net Benefit to SCI = 60,12,270 - 48,51,070 = 11,61,270. Hence, the proposal is worthwhile. 2. Other Factors to be considered: (a) Stability of Price and the longevity of the proposal of the Japanese Manufacturer. (b) Certainty of Fiscal Policy in India and China Change in Tax Rates, Customs Duty Rates, if importing become economical than manufacturing / procurement in India. (c) Regulations as to Repatriation of Indian Profits, i.e.Indian Subsidiary making profit, but should be repatriated to US. (d) Utilisation of Spare Capacity in China, possibility of increasing local sales in China, and scope for higher prices, etc. 13.48 het ca wasthi bhrom het slow the ato ty ORY Proposed Transfer (9,600 Unis) 11. 18 10 14.52,00 3.96,000 Tots but type) 19,20,000 1,48,300 Observation may not be herested in 13.600 Unies to x at 35 p. due to reduction in Contribution Note Effect of 39,500 Units transferred by Division Y - From Company's View point (t cost of real Transfer Varie Cast Opportunity Cost of Y = 15 11.30 26.30 Opportunity cost Contribution test on Extemal Sales 19,20,000 - 14.52,800 = 4,67,200 Hence, Opportunity Cost per unit of Interal Transfer 4,67,200 11.80 39,600 (h) External Purchase Price - 35.00 Hence, Transfer by Division Yts beneficial from Company's view point, due to lower costs. 4,350 Analysis of Ability to Pay - Negotiated Transfer Pricing - Optimal Decision for Overall Company RTP PIRANHA LTD has two divisions Sorty and Torty. Sorty transfers all its output to Torty which finishes the work. Costs and revenues at various levels of capacity are as follows - Output in units 600 700 800 900 1,000 1,100 1,200 Sorty's Costs ) 600 700 840 1,000 1,200 1.450 1,800 Torty's Net Revenues fie. Revenues less 2,950 3,250 3,530 3,780 4,000 4,200 Costs incurred in Torty)) Company's Profit) 2,350 2,550 2,690 2,780 2,800 2,750 2,550 The Company's profits are maximised at 2,800 with output of 1,000 units. If Piranha wish to select a Transfer Price in order to establish Sorty and Torty as Profit Centres, what Transfer Price would motivate the Managers of the Divisions to produce 1,000 units, no more and no less? Also, Piranha wants that the Transfer Price should be fixed at 2.10 per unit. Comment on this proposal. Solution: 1. Sorty's Costs Analysis (for Minimum Transfer Price of Transferring Division) Output in units 600 700 800 900 1,000 1,100 1,200 Sorty's Costs 7600 3700 7840 31,000 31,200 31,450 31,800 Additional Outpat (quantity) 100 100 100 100 100 100 Additional Costs incurred 100 3140 3160 200 3250 7350 Additional Costs per unit of output 1.00 3 1.40 1.60 72.00 22.50 73.50 To motivate Sorty to produce upto 1,000 units, a Minimum Transfer Price = Cost Incurred = * 2.00 per unit should be sufficient. If the TP = 2.00 per unit, Sorty will not produce beyond 1,000 units since incremental cost per unit is higher. 2 Torty's Profitability Analysis (for Maximum Transfer Price of Recipient Division) Output in units 600 700 800 900 1,000 1,100 1,200 Torty's Net Revenues (ie. Revenues less 2,950 33,250 33,530 33,780 34,000 34,200 Costs incurred in Torty) Additional Output (quantity) 100 100 100 100 Additional Ability to pay 280 250 * 220 7200 Additional Ability to Pay per unit 73.00 3 2.80 32.50 2.20 32.00 1.50 4,350 100 100 7150 3300 13.50 . 8 5 30 3 2 5 2 Podhuka's - Students' Handbook on Strategic Cost Management & Performance Evaluation CA Final 32. Optimal Decision for Overall Company - Smoothening the ROI - Various TP Options Ajmer Division (A) and Bikaner Division (8) are two Manufacturing Divisions of Rajasthan Limited. A makes Product I and B makes Product J. Every unit of J requires one unit of 1. The required input of I is normally purchased from an outside source. The following table gives details of Selling Price and cost for each product. Particulars Product 1 Product J Division B Established Selling Price 30 50 Variable Costs - Direct Materials Transfer from A Direct Labour Variable Overhead Total Variable Costs 15 40 Divisional Fixed Cost per annum * 5,00,000 32,25,000 Annual Outside Demand- With Current Selling Price (units) 1,00,000 25,000 Capacity of Plant (units) 1,30,000 30,000 Investment in Division 66,25,000 12,50,000 Division B is currently achieving a rate of return below the target set by the Central Office. Its Manager blames this situation on the high Transfer Price of Product 1. Division A charges Division B for the transfers of Product I at the outside supply price of 30. The Manager of Division A claims that this is appropriate since this is the price "determined by market forces". The Manager of B has consistently argued that intra-group transfers should be charged at a lower price based on the costs of the Producing Division plus a "reasonable" mark up. The Board of the Company is concerned about B's low rate of return and the Divisional Manager has been asked to submit a proposal for improving the situation. The Board has now received a report from B's Manager in which he asks the Board to intervene to reduce the Transfer Price charged for Product I. The Manager of B also informs the Board that he is considering the possibility of opening a branch office in rented premises in a nearby town, which should enlarge the market for Product J by 5,000 units per year at the existing price. He estimates that the Branch Office Establishment Costs would be

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cornerstones of Managerial Accounting

Authors: Mowen, Hansen, Heitger

3rd Edition

324660138, 978-0324660135