Answered step by step

Verified Expert Solution

Question

1 Approved Answer

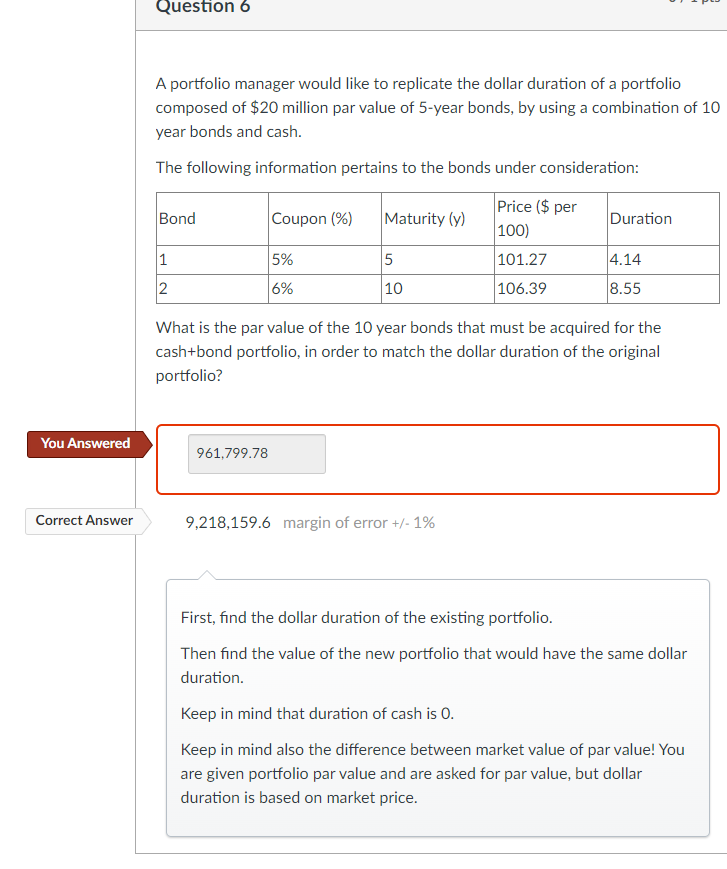

Need the correct excel formulas please Question 6 A portfolio manager would like to replicate the dollar duration of a portfolio composed of $20 million

Need the correct excel formulas please

Question 6 A portfolio manager would like to replicate the dollar duration of a portfolio composed of $20 million par value of 5-year bonds, by using a combination of 10 year bonds and cash. The following information pertains to the bonds under consideration: Bond 1 2 Coupon (%) 5% 6% Maturity (y) 5 10 Price ($ per 100) 101.27 106.39 Duration 4.14 8.55 What is the par value of the 10 year bonds that must be acquired for the cash+bond portfolio, in order to match the dollar duration of the original portfolio? You Answered Correct Answer 961,799.78 9,218,159.6 margin of error +1- 1% First, find the dollar duration of the existing portfolio. Then find the value of the new portfolio that would have the same dollar duration. Keep in mind that duration of cash is O. Keep in mind also the difference between market value of par value! You are given portfolio par value and are asked for par value, but dollar duration is based on market price.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance For Managers

Authors: E. Martinez Abascal

1st Edition

0077140079, 9780077140076