Need to solve problem 11 to do problem 12 Problem 11: Option valuation You own a one-year call option to buy one acre of Los

Need to solve problem 11 to do problem 12

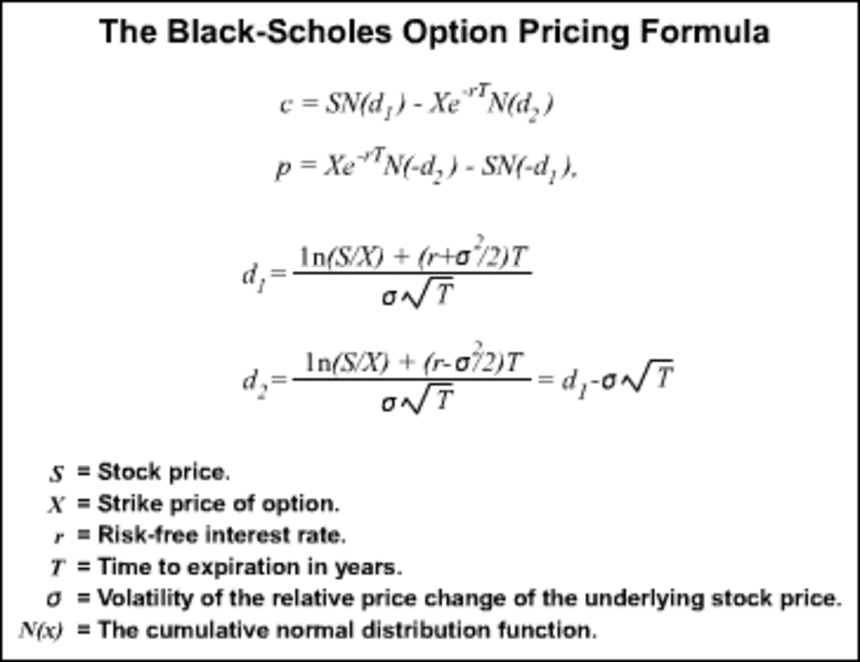

Problem 11: Option valuation You own a one-year call option to buy one acre of Los Angeles real estate. The x exercise price is $2 million, and the current, appraised market value of the land is $1.7 million. The land is currently used as a parking lot, generating just enough money to cover real estate taxes. The annual standard deviation is 15% and the interest rate 12%. How much is your call worth? Use the BlackScholes formula. You may find it helpful to go to the spreadsheet for Chapter 21, which calculates BlackScholes values (visit this books website, www.mhhe.com/bma).

Problem 12:Option valuation A variation on Problem 11: Suppose the land is occupied by a warehouse generating rents of $150,000 after real estate taxes and all other out-of-pocket costs. The present value of the land plus warehouse is again $1.7 million. Other facts are as in Problem 11. You have a European call option. What is it worth?

The Black-Scholes Option Pricing Formula rT. ONT on T S Stock price XE Strike price of option. r Risk-free interest rate. T -Time to expiration in years o Evolatility of the relative price change of the underlying stock price. Nx The cumulative normal distribution functionStep by Step Solution

There are 3 Steps involved in it

Step: 1

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: CFP Board

2nd Edition

1119094968, 978-1119094968