Answered step by step

Verified Expert Solution

Question

1 Approved Answer

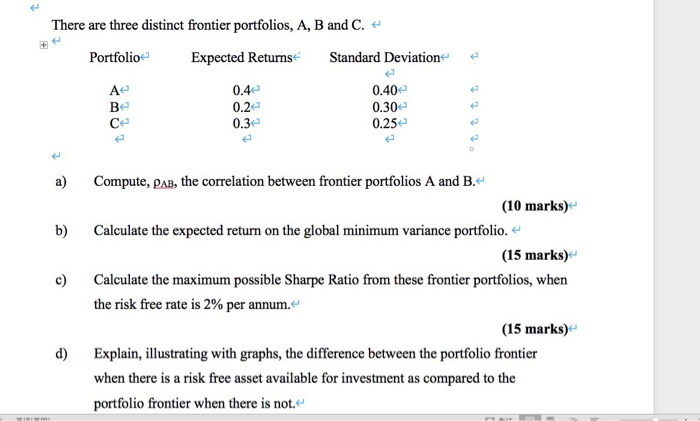

No more information! that is all the question give us There are three distinct frontier portfolios, A, B and C. Portfolio Expected Returns Standard Deviation

No more information! that is all the question give us

There are three distinct frontier portfolios, A, B and C. Portfolio Expected Returns Standard Deviation e A 0.4 0.2 0.32 0.40 0.30 0.25e a) c) Compute, pas, the correlation between frontier portfolios A and B. (10 marks) Calculate the expected return on the global minimum variance portfolio. (15 marks) Calculate the maximum possible Sharpe Ratio from these frontier portfolios, when the risk free rate is 2% per annum. (15 marks) Explain, illustrating with graphs, the difference between the portfolio frontier when there is a risk free asset available for investment as compared to the portfolio frontier when there is not. d) There are three distinct frontier portfolios, A, B and C. Portfolio Expected Returns Standard Deviation e A 0.4 0.2 0.32 0.40 0.30 0.25e a) c) Compute, pas, the correlation between frontier portfolios A and B. (10 marks) Calculate the expected return on the global minimum variance portfolio. (15 marks) Calculate the maximum possible Sharpe Ratio from these frontier portfolios, when the risk free rate is 2% per annum. (15 marks) Explain, illustrating with graphs, the difference between the portfolio frontier when there is a risk free asset available for investment as compared to the portfolio frontier when there is not. d) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Products An Introduction Using Mathematics And Excel

Authors: Bill Dalton

1st Edition

0521863589,0511434006