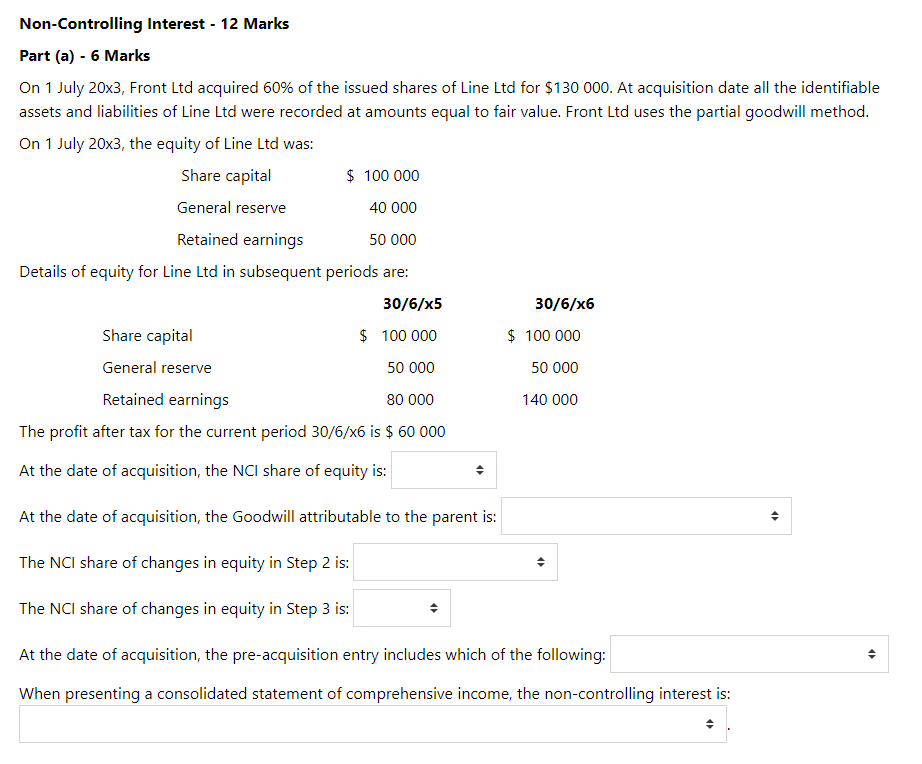

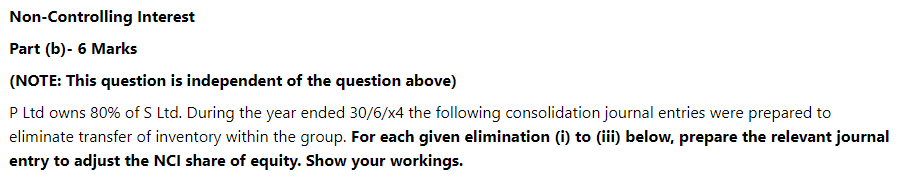

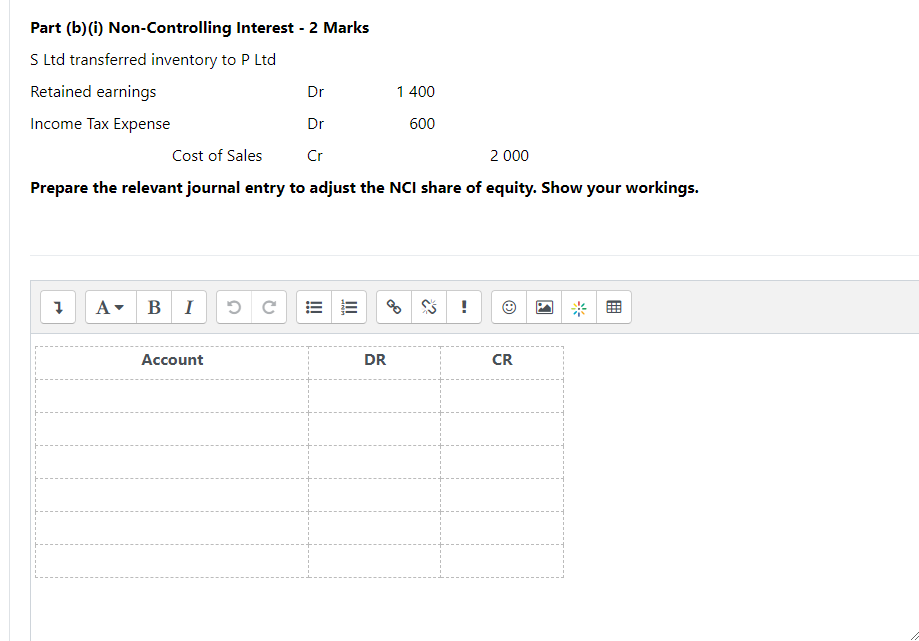

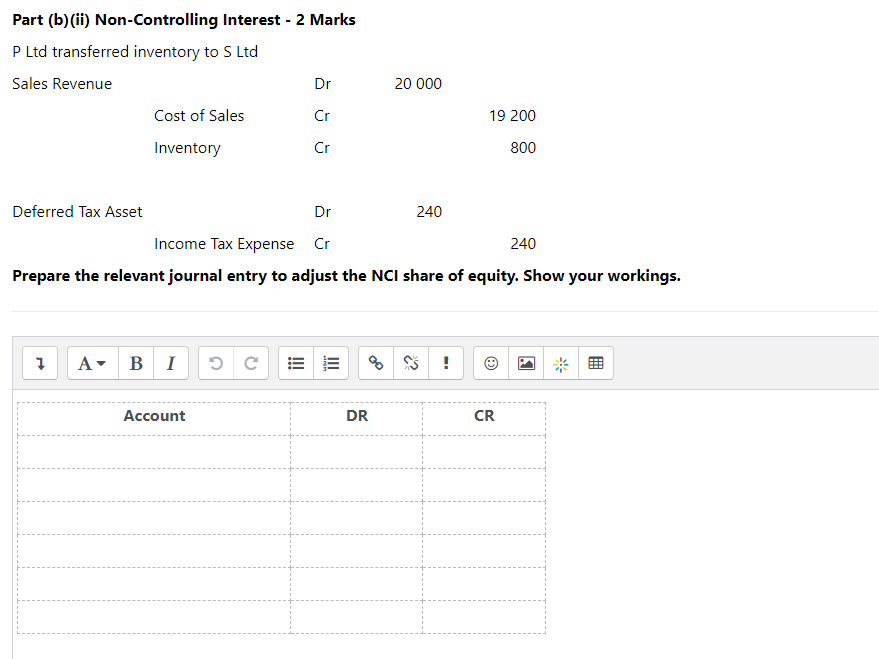

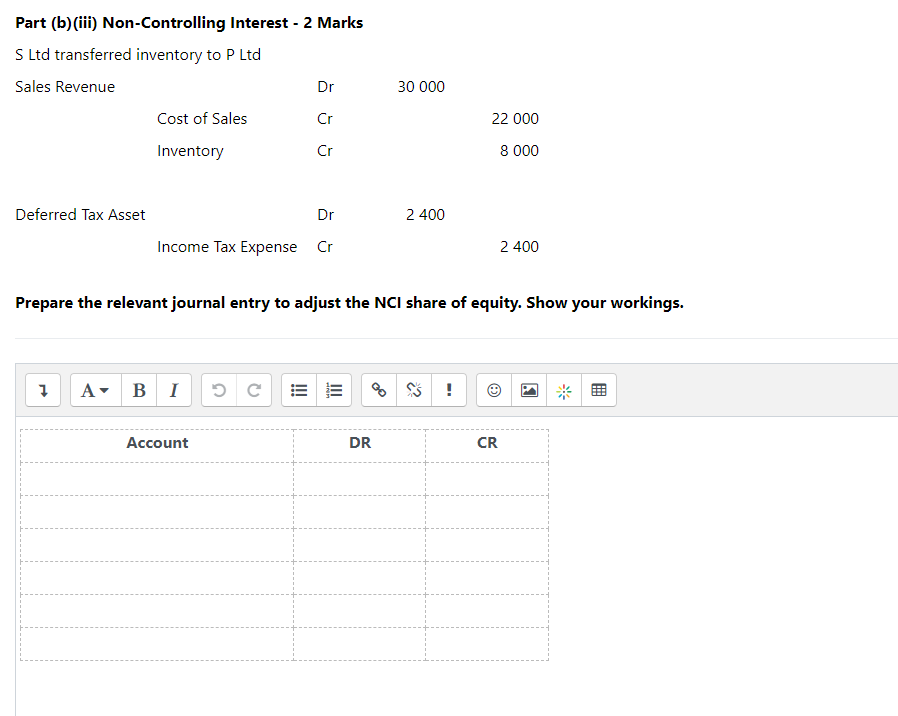

Non-Controlling Interest - 12 Marks Part (a) - 6 Marks On 1 July 20x3, Front Ltd acquired 60% of the issued shares of Line Ltd for $130 000. At acquisition date all the identifiable assets and liabilities of Line Ltd were recorded at amounts equal to fair value. Front Ltd uses the partial goodwill method. On 1 July 20x3, the equity of Line Ltd was: Share capital $ 100 000 General reserve 40 000 Retained earnings 50 000 Details of equity for Line Ltd in subsequent periods are: 30/6/x5 30/6/x6 Share capital $ 100 000 $ 100 000 General reserve 50 000 50 000 Retained earnings 80 000 140 000 The profit after tax for the current period 30/6/x6 is $ 60 000 > At the date of acquisition, the NCI share of equity is: At the date of acquisition, the Goodwill attributable to the parent is: The NCI share of changes in equity in Step 2 is: The NCI share of changes in equity in Step 3 is: At the date of acquisition, the pre-acquisition entry includes which of the following: When presenting a consolidated statement of comprehensive income, the non-controlling interest is: Non-Controlling Interest Part (b)- 6 Marks (NOTE: This question is independent of the question above) P Ltd owns 80% of S Ltd. During the year ended 30/6/x4 the following consolidation journal entries were prepared to eliminate transfer of inventory within the group. For each given elimination (i) to (iii) below, prepare the relevant journal entry to adjust the NCI share of equity. Show your workings. Part (b)(i) Non-Controlling Interest - 2 Marks S Ltd transferred inventory to P Ltd Retained earnings Dr 1 400 Income Tax Expense Dr 600 Cost of Sales Cr 2 000 Prepare the relevant journal entry to adjust the NCI share of equity. Show your workings. 1 A B 1 !!! III 5 9 * Account DR CR Part (b)(ii) Non-Controlling Interest - 2 Marks P Ltd transferred inventory to S Ltd Sales Revenue Dr Cost of Sales Cr Inventory Cr 20 000 19 200 800 240 Deferred Tax Asset Dr Income Tax Expense Cr 240 Prepare the relevant journal entry to adjust the NCI share of equity. Show your workings. 7 A B 1 !!! III c? ! * Account DR CR Part (b)(iii) Non-Controlling Interest - 2 Marks S Ltd transferred inventory to P Ltd Sales Revenue Dr Cost of Sales Cr Inventory Cr 30 000 22 000 8 000 Deferred Tax Asset Dr 2400 Income Tax Expense Cr 2 400 Prepare the relevant journal entry to adjust the NCI share of equity. Show your workings. 1 A B 1 !!! ! * Account DR CR Non-Controlling Interest - 12 Marks Part (a) - 6 Marks On 1 July 20x3, Front Ltd acquired 60% of the issued shares of Line Ltd for $130 000. At acquisition date all the identifiable assets and liabilities of Line Ltd were recorded at amounts equal to fair value. Front Ltd uses the partial goodwill method. On 1 July 20x3, the equity of Line Ltd was: Share capital $ 100 000 General reserve 40 000 Retained earnings 50 000 Details of equity for Line Ltd in subsequent periods are: 30/6/x5 30/6/x6 Share capital $ 100 000 $ 100 000 General reserve 50 000 50 000 Retained earnings 80 000 140 000 The profit after tax for the current period 30/6/x6 is $ 60 000 > At the date of acquisition, the NCI share of equity is: At the date of acquisition, the Goodwill attributable to the parent is: The NCI share of changes in equity in Step 2 is: The NCI share of changes in equity in Step 3 is: At the date of acquisition, the pre-acquisition entry includes which of the following: When presenting a consolidated statement of comprehensive income, the non-controlling interest is: Non-Controlling Interest Part (b)- 6 Marks (NOTE: This question is independent of the question above) P Ltd owns 80% of S Ltd. During the year ended 30/6/x4 the following consolidation journal entries were prepared to eliminate transfer of inventory within the group. For each given elimination (i) to (iii) below, prepare the relevant journal entry to adjust the NCI share of equity. Show your workings. Part (b)(i) Non-Controlling Interest - 2 Marks S Ltd transferred inventory to P Ltd Retained earnings Dr 1 400 Income Tax Expense Dr 600 Cost of Sales Cr 2 000 Prepare the relevant journal entry to adjust the NCI share of equity. Show your workings. 1 A B 1 !!! III 5 9 * Account DR CR Part (b)(ii) Non-Controlling Interest - 2 Marks P Ltd transferred inventory to S Ltd Sales Revenue Dr Cost of Sales Cr Inventory Cr 20 000 19 200 800 240 Deferred Tax Asset Dr Income Tax Expense Cr 240 Prepare the relevant journal entry to adjust the NCI share of equity. Show your workings. 7 A B 1 !!! III c? ! * Account DR CR Part (b)(iii) Non-Controlling Interest - 2 Marks S Ltd transferred inventory to P Ltd Sales Revenue Dr Cost of Sales Cr Inventory Cr 30 000 22 000 8 000 Deferred Tax Asset Dr 2400 Income Tax Expense Cr 2 400 Prepare the relevant journal entry to adjust the NCI share of equity. Show your workings. 1 A B 1 !!! ! * Account DR CR