Answered step by step

Verified Expert Solution

Question

1 Approved Answer

not sure how to do this problem. Please help solve this, will rate, thank you! MASTERING EXERCISE 6.7.3 #1) [[[Consider discrete time periods 0, 1,

not sure how to do this problem. Please help solve this, will rate, thank you!

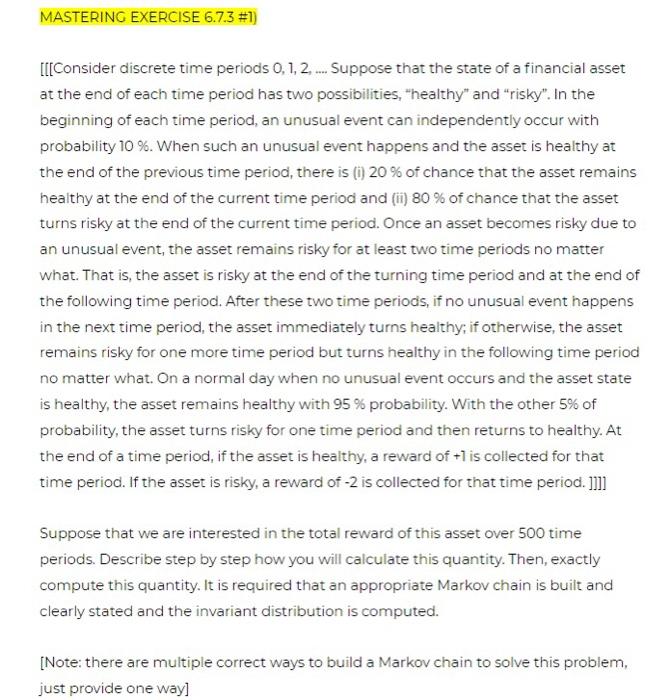

MASTERING EXERCISE 6.7.3 #1) [[[Consider discrete time periods 0, 1, 2, ... Suppose that the state of a financial asset at the end of each time period has two possibilities, "healthy" and "risky". In the beginning of each time period, an unusual event can independently occur with probability 10 %. When such an unusual event happens and the asset is healthy at the end of the previous time period, there is (1) 20 % of chance that the asset remains healthy at the end of the current time period and (ii) 80 % of chance that the asset turns risky at the end of the current time period. Once an asset becomes risky due to an unusual event, the asset remains risky for at least two time periods no matter what. That is, the asset is risky at the end of the turning time period and at the end of the following time period. After these two time periods, if no unusual event happens in the next time period, the asset immediately turns healthy, if otherwise, the asset remains risky for one more time period but turns healthy in the following time period no matter what. On a normal day when no unusual event occurs and the asset state is healthy, the asset remains healthy with 95 % probability. With the other 5% of probability, the asset turns risky for one time period and then returns to healthy. At the end of a time period, if the asset is healthy, a reward of +1 is collected for that time period. If the asset is risky, a reward of -2 is collected for that time period. ]]]] Suppose that we are interested in the total reward of this asset over 500 time periods. Describe step by step how you will calculate this quantity. Then, exactly compute this quantity. It is required that an appropriate Markov chain is built and clearly stated and the invariant distribution is computed. [Note: there are multiple correct ways to build a Markov chain to solve this problem, just provide one way] MASTERING EXERCISE 6.7.3 #1) [[[Consider discrete time periods 0, 1, 2, ... Suppose that the state of a financial asset at the end of each time period has two possibilities, "healthy" and "risky". In the beginning of each time period, an unusual event can independently occur with probability 10 %. When such an unusual event happens and the asset is healthy at the end of the previous time period, there is (1) 20 % of chance that the asset remains healthy at the end of the current time period and (ii) 80 % of chance that the asset turns risky at the end of the current time period. Once an asset becomes risky due to an unusual event, the asset remains risky for at least two time periods no matter what. That is, the asset is risky at the end of the turning time period and at the end of the following time period. After these two time periods, if no unusual event happens in the next time period, the asset immediately turns healthy, if otherwise, the asset remains risky for one more time period but turns healthy in the following time period no matter what. On a normal day when no unusual event occurs and the asset state is healthy, the asset remains healthy with 95 % probability. With the other 5% of probability, the asset turns risky for one time period and then returns to healthy. At the end of a time period, if the asset is healthy, a reward of +1 is collected for that time period. If the asset is risky, a reward of -2 is collected for that time period. ]]]] Suppose that we are interested in the total reward of this asset over 500 time periods. Describe step by step how you will calculate this quantity. Then, exactly compute this quantity. It is required that an appropriate Markov chain is built and clearly stated and the invariant distribution is computed. [Note: there are multiple correct ways to build a Markov chain to solve this problem, just provide one way] Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Eco Capitalism Carbon Money Climate Finance And Sustainable Development

Authors: Robert Guttmann

1st Edition

3319923560,3319923579