Answered step by step

Verified Expert Solution

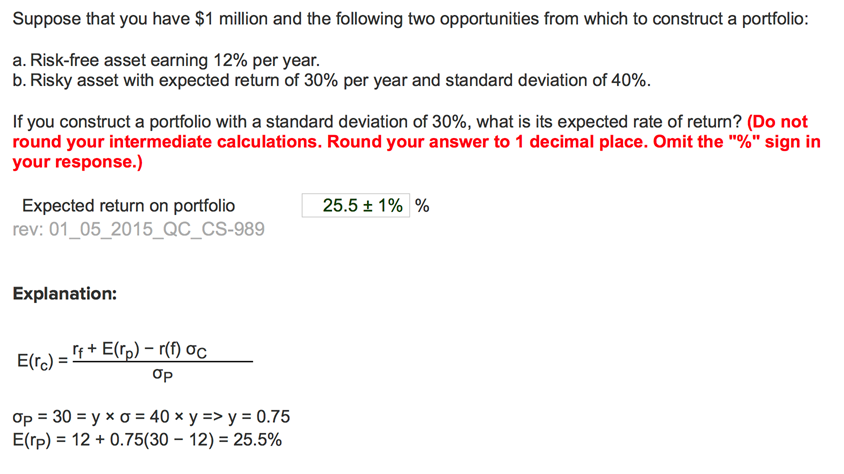

Question

1 Approved Answer

Not understanding the explanation to the answer given in the problem. Did they solve for beta then use CapM? It's unclear to me what they

Not understanding the explanation to the answer given in the problem. Did they solve for beta then use CapM? It's unclear to me what they have done to solve for Y. Please provide detailed explanation.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Pricing Analytics Models And Advanced Quantitative Techniques For Product Pricing

Authors: Walter R. Paczkowski

1st Edition

1138623938, 9781138623934