Answered step by step

Verified Expert Solution

Question

1 Approved Answer

NOTE: All Information to solve question is provided. Only the Highlighted part in green needs to be solved. Thank you! Thunder Bay Outdoor Adventures (TBOA)

NOTE: All Information to solve question is provided. Only the Highlighted part in green needs to be solved. Thank you!

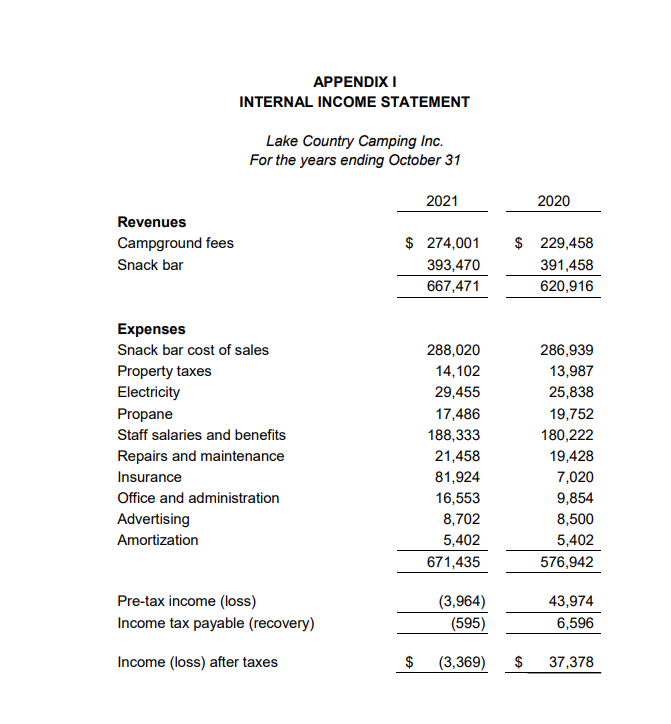

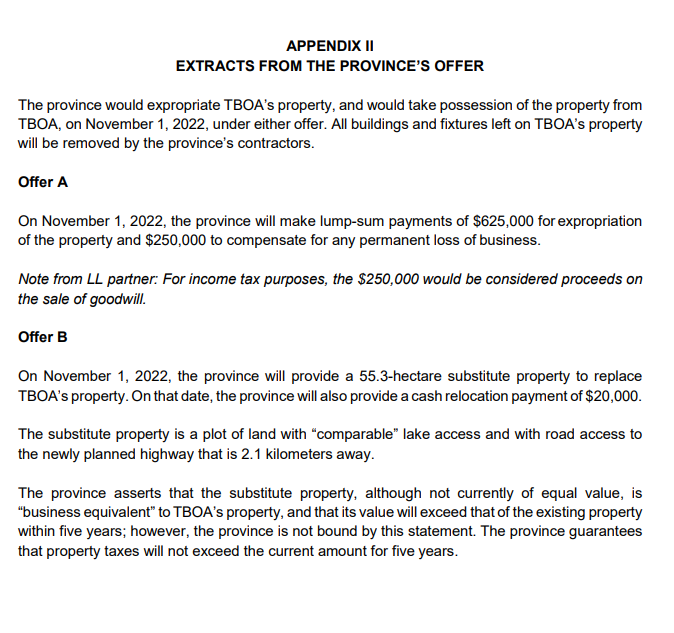

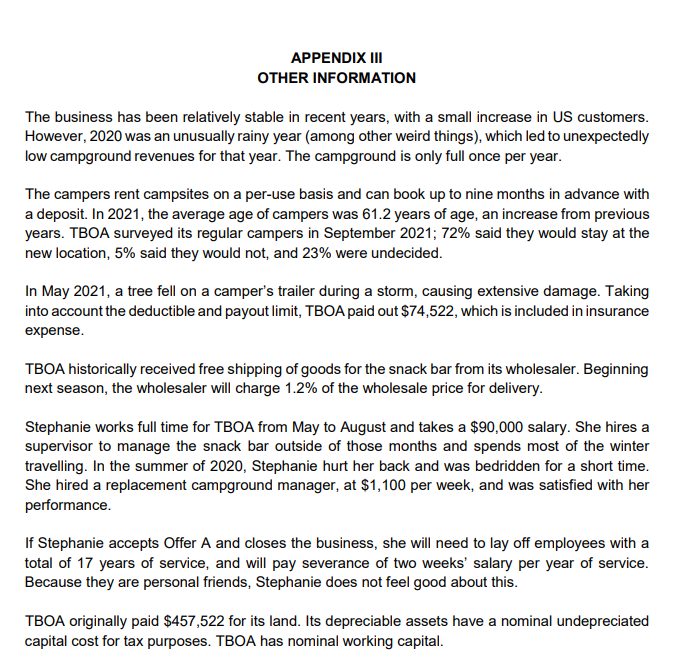

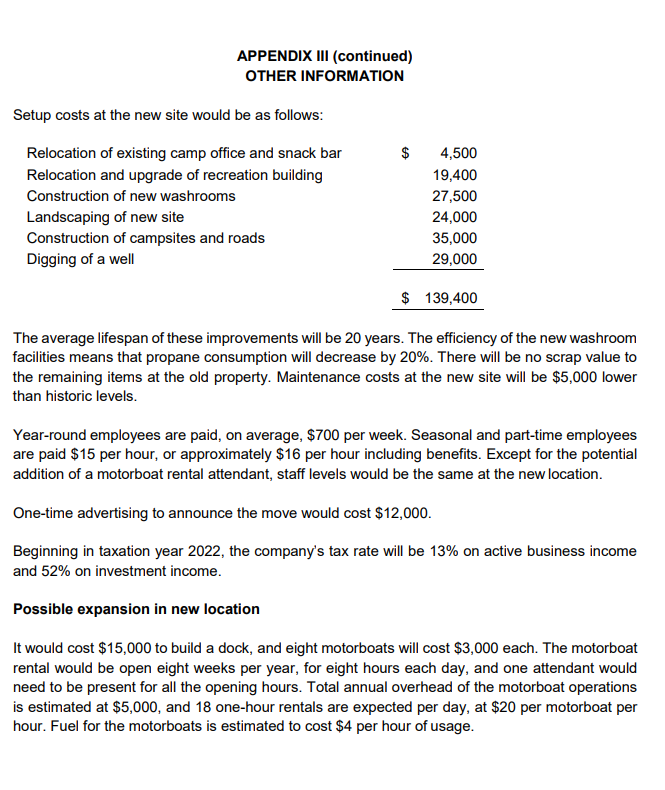

Thunder Bay Outdoor Adventures (TBOA) was incorporated in 2009 and is wholly-owned by Stephanie McManus, who is single and 58 years old. TBOA operates a campground and snack bar just off Highway 11-17, in a wilderness area that provides access to various lakes in Northwestern Ontario. Except for snack bar revenues, which are earned year-round from people who drive by, most revenue is earned in the camping season (May to August). TBOA's income statement for its year ended October 31, 2021, is in Appendix I. Today is November 28, 2021. Although she enjoys operating the campground, Stephanie is planning to retire to British Columbia. Stephanie has asked Lento & Lento LLP (LL) to assist with some major decisions. You, CPA, work at LL. On June 1, 2021, the provincial government (the province) announced that Highway 11-17 will be widened, requiring expropriation of all of TBOA's 49.2 hectares of land. The province offered TBOA two options. TBOA must select either Offer A or Offer B by December 31, 2021 (Appendix II). Other relevant information is presented in Appendix III. Offer A would mean closing down the business and would allow Stephanie to retire right away. Offer B would provide a substitute property and a cash relocation allowance. The substitute property would accommodate more campsites. If she chooses Offer B, Stephanie would hire a full-time manager to replace her and would retire after a short transition period. To help Stephanie assess Offer B, the partner asks you to forecast the normalized annual revenues and expenses. The partner would then like you to use this to value the business for Stephanie under Offer B. In this industry, a normalized after-tax earnings multiplier of between 4 and 7 would apply. The partner would like you to use this valuation to provide both a quantitative and a qualitative comparison of Offer A and Offer B, and to recommend to Stephanie which option to choose. The partner would like you to calculate and discuss the tax implications of each offer. The substitute property also provides the opportunity to offer motorboat rentals. While she does not want you to include this in your assessment of Offer B, Stephanie asks you to calculate the contribution margin and required breakeven volume, and assess the qualitative factors, for the potential motorboat rentals. TBOA has never had its financial statements audited. Under Offer B, TBOA would likely have an audit performed in the future. Stephanie is interested in knowing what substantive procedures would be performed on several accounts: campground fees; snack bar revenue; snack bar cost of sales; and repairs and maintenance. APPENDIX 1 INTERNAL INCOME STATEMENT Lake Country Camping Inc. For the years ending October 31 2021 2020 Revenues Campground fees Snack bar $ 274,001 393,470 667,471 $ 229,458 391,458 620,916 Expenses Snack bar cost of sales Property taxes Electricity Propane Staff salaries and benefits Repairs and maintenance Insurance Office and administration Advertising Amortization 288,020 14,102 29,455 17,486 188,333 21,458 81,924 16,553 8,702 5,402 671,435 286,939 13,987 25,838 19,752 180,222 19,428 7,020 9,854 8,500 5,402 576,942 Pre-tax income (loss) Income tax payable (recovery) (3,964) (595) 43,974 6,596 Income (loss) after taxes $ (3,369) $ 37,378 APPENDIX 11 EXTRACTS FROM THE PROVINCE'S OFFER The province would expropriate TBOA's property, and would take possession of the property from TBOA, on November 1, 2022, under either offer. All buildings and fixtures left on TBOA's property will be removed by the province's contractors. Offer A On November 1, 2022, the province will make lump-sum payments of $625,000 for expropriation of the property and $250,000 to compensate for any permanent loss of business. Note from LL partner: For income tax purposes, the $250,000 would be considered proceeds on the sale of goodwill. Offer B On November 1, 2022, the province will provide a 55.3-hectare substitute property to replace TBOA's property. On that date, the province will also provide a cash relocation payment of $20,000. The substitute property is a plot of land with comparable" lake access and with road access to the newly planned highway that is 2.1 kilometers away. The province asserts that the substitute property, although not currently of equal value, is "business equivalent" to TBOA's property, and that its value will exceed that of the existing property within five years; however, the province is not bound by this statement. The province guarantees that property taxes will not exceed the current amount for five years. APPENDIX III OTHER INFORMATION The business has been relatively stable in recent years, with a small increase in US customers. However, 2020 was an unusually rainy year (among other weird things), which led to unexpectedly low campground revenues for that year. The campground is only full once per year. The campers rent campsites on a per-use basis and can book up to nine months in advance with a deposit. In 2021, the average age of campers was 61.2 years of age, an increase from previous years. TBOA surveyed its regular campers in September 2021; 72% said they would stay at the new location, 5% said they would not, and 23% were undecided. In May 2021, a tree fell on a camper's trailer during a storm, causing extensive damage. Taking into account the deductible and payout limit, TBOA paid out $74,522, which is included in insurance expense. TBOA historically received free shipping of goods for the snack bar from its wholesaler. Beginning next season, the wholesaler will charge 1.2% of the wholesale price for delivery. Stephanie works full time for TBOA from May to August and takes a $90,000 salary. She hires a supervisor to manage the snack bar outside of those months and spends most of the winter travelling. In the summer of 2020, Stephanie hurt her back and was bedridden for a short time. She hired a replacement campground manager, at $1,100 per week, and was satisfied with her performance. If Stephanie accepts Offer A and closes the business, she will need to lay off employees with a total of 17 years of service, and will pay severance of two weeks' salary per year of service. Because they are personal friends, Stephanie does not feel good about this. TBOA originally paid $457,522 for its land. Its depreciable assets have a nominal undepreciated capital cost for tax purposes. TBOA has nominal working capital. APPENDIX III (continued) OTHER INFORMATION Setup costs at the new site would be as follows: $ Relocation of existing camp office and snack bar Relocation and upgrade of recreation building Construction of new washrooms Landscaping of new site Construction of campsites and roads Digging of a well 4,500 19,400 27,500 24,000 35,000 29,000 $ 139,400 The average lifespan of these improvements will be 20 years. The efficiency of the new washroom facilities means that propane consumption will decrease by 20%. There will be no scrap value to the remaining items at the old property. Maintenance costs at the new site will be $5,000 lower than historic levels. Year-round employees are paid, on average, $700 per week. Seasonal and part-time employees are paid $15 per hour, or approximately $16 per hour including benefits. Except for the potential addition of a motorboat rental attendant, staff levels would be the same at the new location. One-time advertising to announce the move would cost $12,000. Beginning in taxation year 2022, the company's tax rate will be 13% on active business income and 52% on investment income. Possible expansion in new location It would cost $15,000 to build a dock, and eight motorboats will cost $3,000 each. The motorboat rental would be open eight weeks per year, for eight hours each day, and one attendant would need to be present for all the opening hours. Total annual overhead of the motorboat operations is estimated at $5,000, and 18 one-hour rentals are expected per day, at $20 per motorboat per hour. Fuel for the motorboats is estimated to cost $4 per hour of usage. Thunder Bay Outdoor Adventures (TBOA) was incorporated in 2009 and is wholly-owned by Stephanie McManus, who is single and 58 years old. TBOA operates a campground and snack bar just off Highway 11-17, in a wilderness area that provides access to various lakes in Northwestern Ontario. Except for snack bar revenues, which are earned year-round from people who drive by, most revenue is earned in the camping season (May to August). TBOA's income statement for its year ended October 31, 2021, is in Appendix I. Today is November 28, 2021. Although she enjoys operating the campground, Stephanie is planning to retire to British Columbia. Stephanie has asked Lento & Lento LLP (LL) to assist with some major decisions. You, CPA, work at LL. On June 1, 2021, the provincial government (the province) announced that Highway 11-17 will be widened, requiring expropriation of all of TBOA's 49.2 hectares of land. The province offered TBOA two options. TBOA must select either Offer A or Offer B by December 31, 2021 (Appendix II). Other relevant information is presented in Appendix III. Offer A would mean closing down the business and would allow Stephanie to retire right away. Offer B would provide a substitute property and a cash relocation allowance. The substitute property would accommodate more campsites. If she chooses Offer B, Stephanie would hire a full-time manager to replace her and would retire after a short transition period. To help Stephanie assess Offer B, the partner asks you to forecast the normalized annual revenues and expenses. The partner would then like you to use this to value the business for Stephanie under Offer B. In this industry, a normalized after-tax earnings multiplier of between 4 and 7 would apply. The partner would like you to use this valuation to provide both a quantitative and a qualitative comparison of Offer A and Offer B, and to recommend to Stephanie which option to choose. The partner would like you to calculate and discuss the tax implications of each offer. The substitute property also provides the opportunity to offer motorboat rentals. While she does not want you to include this in your assessment of Offer B, Stephanie asks you to calculate the contribution margin and required breakeven volume, and assess the qualitative factors, for the potential motorboat rentals. TBOA has never had its financial statements audited. Under Offer B, TBOA would likely have an audit performed in the future. Stephanie is interested in knowing what substantive procedures would be performed on several accounts: campground fees; snack bar revenue; snack bar cost of sales; and repairs and maintenance. APPENDIX 1 INTERNAL INCOME STATEMENT Lake Country Camping Inc. For the years ending October 31 2021 2020 Revenues Campground fees Snack bar $ 274,001 393,470 667,471 $ 229,458 391,458 620,916 Expenses Snack bar cost of sales Property taxes Electricity Propane Staff salaries and benefits Repairs and maintenance Insurance Office and administration Advertising Amortization 288,020 14,102 29,455 17,486 188,333 21,458 81,924 16,553 8,702 5,402 671,435 286,939 13,987 25,838 19,752 180,222 19,428 7,020 9,854 8,500 5,402 576,942 Pre-tax income (loss) Income tax payable (recovery) (3,964) (595) 43,974 6,596 Income (loss) after taxes $ (3,369) $ 37,378 APPENDIX 11 EXTRACTS FROM THE PROVINCE'S OFFER The province would expropriate TBOA's property, and would take possession of the property from TBOA, on November 1, 2022, under either offer. All buildings and fixtures left on TBOA's property will be removed by the province's contractors. Offer A On November 1, 2022, the province will make lump-sum payments of $625,000 for expropriation of the property and $250,000 to compensate for any permanent loss of business. Note from LL partner: For income tax purposes, the $250,000 would be considered proceeds on the sale of goodwill. Offer B On November 1, 2022, the province will provide a 55.3-hectare substitute property to replace TBOA's property. On that date, the province will also provide a cash relocation payment of $20,000. The substitute property is a plot of land with comparable" lake access and with road access to the newly planned highway that is 2.1 kilometers away. The province asserts that the substitute property, although not currently of equal value, is "business equivalent" to TBOA's property, and that its value will exceed that of the existing property within five years; however, the province is not bound by this statement. The province guarantees that property taxes will not exceed the current amount for five years. APPENDIX III OTHER INFORMATION The business has been relatively stable in recent years, with a small increase in US customers. However, 2020 was an unusually rainy year (among other weird things), which led to unexpectedly low campground revenues for that year. The campground is only full once per year. The campers rent campsites on a per-use basis and can book up to nine months in advance with a deposit. In 2021, the average age of campers was 61.2 years of age, an increase from previous years. TBOA surveyed its regular campers in September 2021; 72% said they would stay at the new location, 5% said they would not, and 23% were undecided. In May 2021, a tree fell on a camper's trailer during a storm, causing extensive damage. Taking into account the deductible and payout limit, TBOA paid out $74,522, which is included in insurance expense. TBOA historically received free shipping of goods for the snack bar from its wholesaler. Beginning next season, the wholesaler will charge 1.2% of the wholesale price for delivery. Stephanie works full time for TBOA from May to August and takes a $90,000 salary. She hires a supervisor to manage the snack bar outside of those months and spends most of the winter travelling. In the summer of 2020, Stephanie hurt her back and was bedridden for a short time. She hired a replacement campground manager, at $1,100 per week, and was satisfied with her performance. If Stephanie accepts Offer A and closes the business, she will need to lay off employees with a total of 17 years of service, and will pay severance of two weeks' salary per year of service. Because they are personal friends, Stephanie does not feel good about this. TBOA originally paid $457,522 for its land. Its depreciable assets have a nominal undepreciated capital cost for tax purposes. TBOA has nominal working capital. APPENDIX III (continued) OTHER INFORMATION Setup costs at the new site would be as follows: $ Relocation of existing camp office and snack bar Relocation and upgrade of recreation building Construction of new washrooms Landscaping of new site Construction of campsites and roads Digging of a well 4,500 19,400 27,500 24,000 35,000 29,000 $ 139,400 The average lifespan of these improvements will be 20 years. The efficiency of the new washroom facilities means that propane consumption will decrease by 20%. There will be no scrap value to the remaining items at the old property. Maintenance costs at the new site will be $5,000 lower than historic levels. Year-round employees are paid, on average, $700 per week. Seasonal and part-time employees are paid $15 per hour, or approximately $16 per hour including benefits. Except for the potential addition of a motorboat rental attendant, staff levels would be the same at the new location. One-time advertising to announce the move would cost $12,000. Beginning in taxation year 2022, the company's tax rate will be 13% on active business income and 52% on investment income. Possible expansion in new location It would cost $15,000 to build a dock, and eight motorboats will cost $3,000 each. The motorboat rental would be open eight weeks per year, for eight hours each day, and one attendant would need to be present for all the opening hours. Total annual overhead of the motorboat operations is estimated at $5,000, and 18 one-hour rentals are expected per day, at $20 per motorboat per hour. Fuel for the motorboats is estimated to cost $4 per hour of usage

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Markets And Institutions

Authors: Jeff Madura

10th Edition

1285531507, 9781285531502