Question

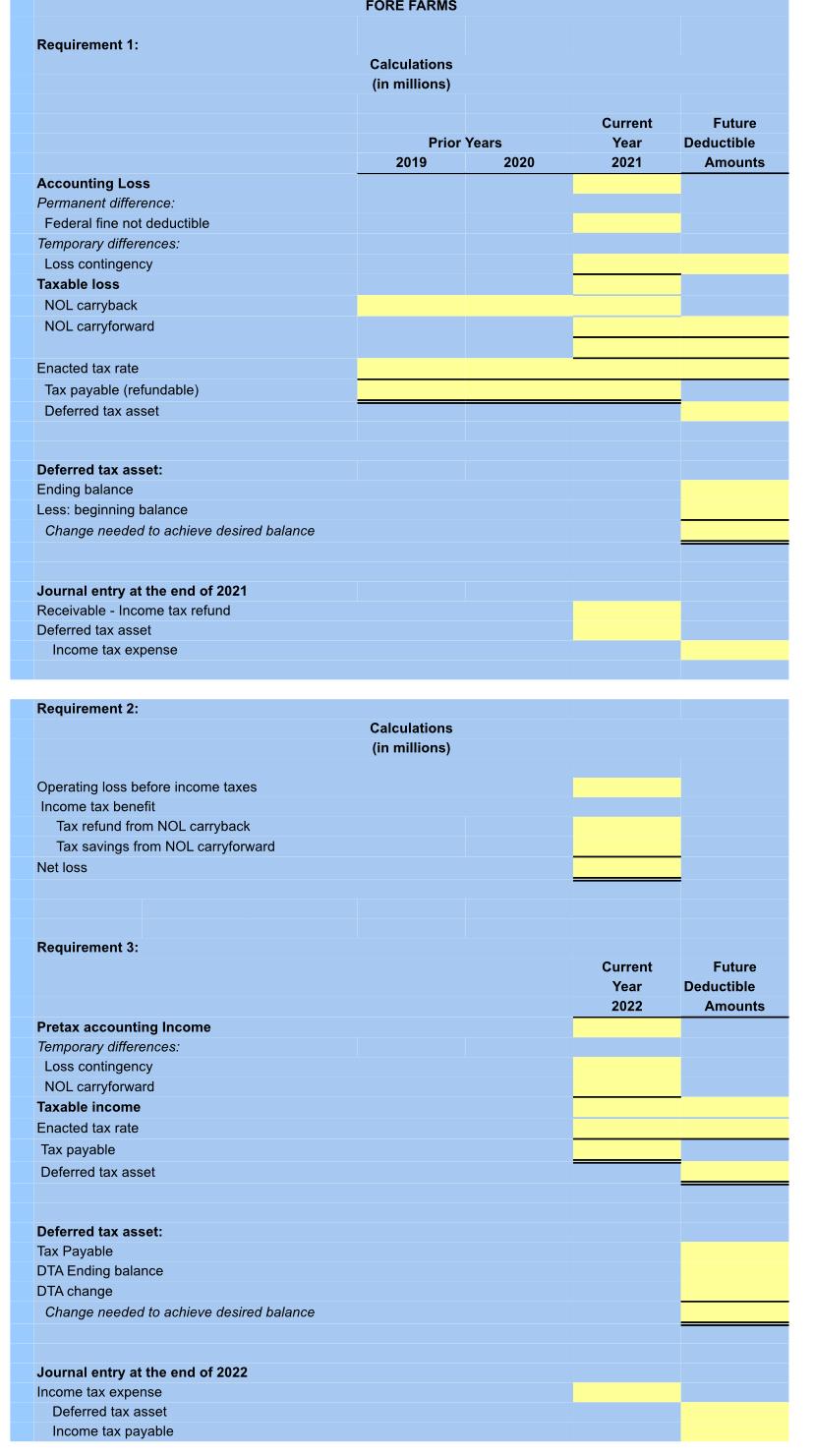

(Note: this problem is a variation of P16-10, modified to allow a net operating loss carryback) Fore Farms reported a pretax operating loss of $137

(Note: this problem is a variation of P16-10, modified to allow a net operating loss carryback) Fore Farms reported a pretax operating loss of $137 million for financial reporting purposes in 2021. Contributing to the loss were (a) a penalty of $5 million assessed by the Environmental Protection Agency for violation of a federal law and paid in 2021 and (b) an estimated loss of $12 million from accruing a loss contingency. The loss will be tax deductible when paid in 2022. The enacted tax rate is 25%. There were no temporary differences at the beginning of the year and none originating in 2021 other than those described above. Taxable income in Foress two previous year of operation was as follows:

2019 $80 million

2020 $32 million.

Prepare the journal entry to recognize the income tax benefit of the net operating loss in 2021. Assume Fore will carry back its NOL to prior years.

Show the lower portion of the 2021 income statement that reports the income tax benefit of the net operating loss

Prepare the journal entry to record income taxes in 2022 assuming pretax accounting income is $160 million. No additional temporary differences originate in 2022.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cost Accounting Foundations and Evolutions

Authors: Michael R. Kinney, Cecily A. Raiborn

9th edition

9781285401072, 1111971722, 1285401077, 978-1111971724