Answered step by step

Verified Expert Solution

Question

1 Approved Answer

note: using SOFR and not LIBOR. Swap example from powerpoint provided at the bottom of the photo. thank you in advance for your help! :)

note: using SOFR and not LIBOR. Swap example from powerpoint provided at the bottom of the photo. thank you in advance for your help! :)

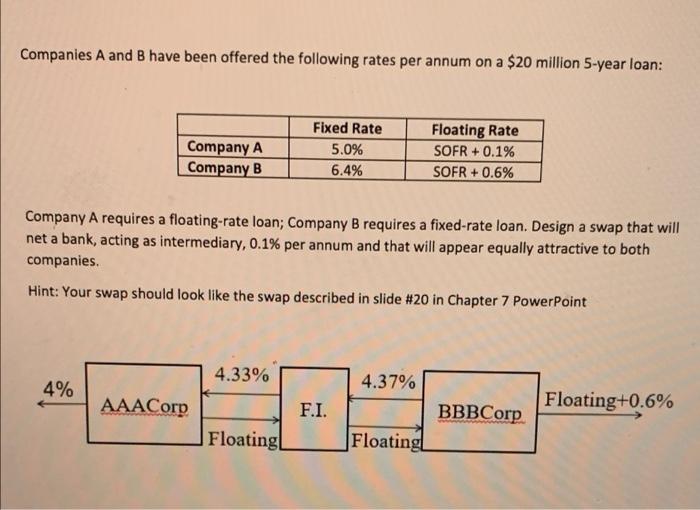

Companies A and B have been offered the following rates per annum on a $20 million 5-year loan: Company A Company B Fixed Rate 5.0% 6.4% Floating Rate SOFR + 0.1% SOFR + 0.6% Company A requires a floating-rate loan; Company B requires a fixed-rate loan. Design a swap that will net a bank, acting as intermediary, 0.1% per annum and that will appear equally attractive to both companies. Hint: Your swap should look like the swap described in slide #20 in Chapter 7 PowerPoint 4.33% 4% AAACorp F.I. 4.37% BBBCorp Floating! Floating+0.6% Floating Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Market Takers Edge Insider Strategies From The Options Trading Floor

Authors: Dan Passarelli

1st Edition

007175492X,0071754946