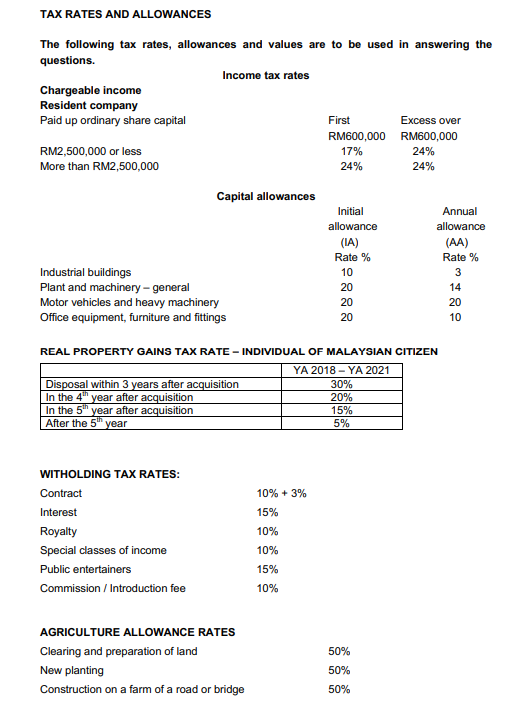

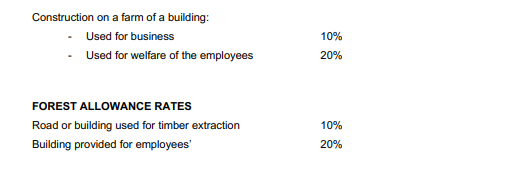

NOTES:

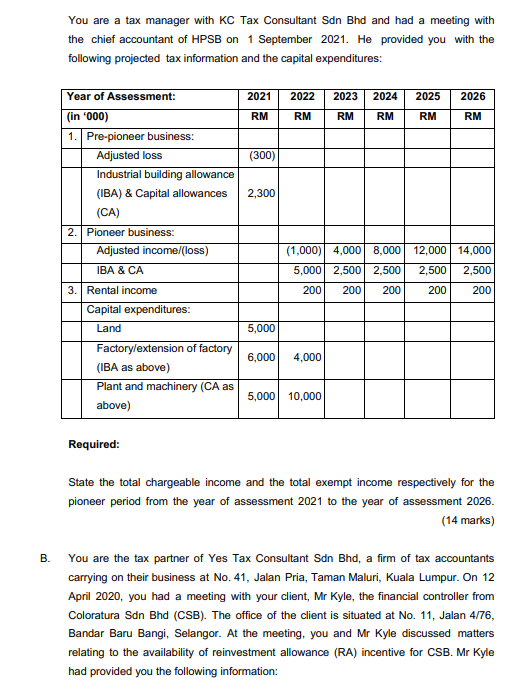

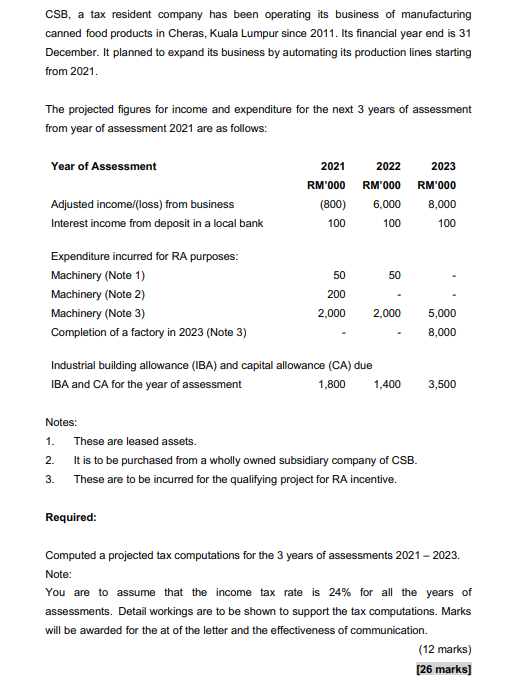

A. Higher Power Sdn Bhd (HPSB) is a new tax resident company in Malaysia with its factory located in Nilai, Negeri Sembilan. It was incorporated on 1 July 2021 with a paid-up capital of RM6 million. It prepares its annual Income Statement to 31 December. Soon after HPSB was incorporated, it made an application to Malaysian Investment Development Authority (MIDA) for pioneer status tax incentive. It commenced manufacturing a promoted product ox on 1 August 2021 upon receiving an initial approval from the MIDA. MIDA issued a pioneer certificate when HPSB achieved the stipulated production target. The production date as stated in the pioneer certificate was 1 January 2022. You are a tax manager with KC Tax Consultant Sdn Bhd and had a meeting with the chief accountant of HPSB on 1 September 2021. He provided you with the following projected tax information and the capital expenditures: 2021 2022 2023 2024 2025 2026 RM RM RM RM RM RM (300)| 2,300 Year of Assessment: (in '000) 1. Pre-pioneer business: Adjusted loss Industrial building allowance (IBA) & Capital allowances (CA) 2. Pioneer business: Adjusted income (loss) IBA & CA 3. Rental income Capital expenditures: Land Factory/extension of factory (IBA as above) Plant and machinery (CA as above) (1,000) 4,000 8,000 12,000 14,000 5,000 2,500 2,500 2,500 2,500 200 200 200 200 200 5,000 6,000 4,000 5,000 10,000 Required: State the total chargeable income and the total exempt income respectively for the pioneer period from the year of assessment 2021 to the year of assessment 2026. (14 marks) B. You are the tax partner of Yes Tax Consultant Sdn Bhd, a firm of tax accountants carrying on their business at No. 41, Jalan Pria, Taman Maluri, Kuala Lumpur. On 12 April 2020, you had a meeting with your client, Mr Kyle, the financial controller from Coloratura Sdn Bhd (CSB). The office of the client is situated at No. 11, Jalan 4/76, Bandar Baru Bangi, Selangor. At the meeting, you and Mr Kyle discussed matters relating to the availability of reinvestment allowance (RA) incentive for CSB. Mr Kyle had provided you the following information: CSB, a tax resident company has been operating its business of manufacturing canned food products in Cheras, Kuala Lumpur since 2011. Its financial year end is 31 December. It planned to expand its business by automating its production lines starting from 2021 The projected figures for income and expenditure for the next 3 years of assessment from year of assessment 2021 are as follows: Year of Assessment 2023 2021 2022 RM'000 RM'000 (800) 6,000 100 100 RM'000 8,000 Adjusted income (loss) from business Interest income from deposit in a local bank 100 50 50 Expenditure incurred for RA purposes: Machinery (Note 1) Machinery (Note 2) Machinery (Note 3) Completion of a factory in 2023 (Note 3) 200 2,000 2.000 5,000 8,000 Industrial building allowance (IBA) and capital allowance (CA) due IBA and CA for the year of assessment 1,800 1,400 3,500 1. Notes: These are leased assets. 2. It is to be purchased from a wholly owned subsidiary company of CSB. 3. These are to be incurred for the qualifying project for RA incentive. Required: Computed a projected tax computations for the 3 years of assessments 2021 - 2023. Note: You are to assume that the income tax rate is 24% for all the years of assessments. Detail workings are to be shown to support the tax computations. Marks will be awarded for the at of the letter and the effectiveness of communication. (12 marks) [26 marks) TAX RATES AND ALLOWANCES The following tax rates, allowances and values are to be used in answering the questions. Income tax rates Chargeable income Resident company Paid up ordinary share capital First Excess over RM600,000 RM600,000 RM2,500,000 or less 17% 24% More than RM2,500,000 24% 24% Capital allowances Initial Annual allowance allowance (IA) (AA) Rate % Rate % Industrial buildings 10 3 Plant and machinery - general 20 14 Motor vehicles and heavy machinery 20 20 Office equipment, furniture and fittings 20 10 REAL PROPERTY GAINS TAX RATE - INDIVIDUAL OF MALAYSIAN CITIZEN YA 2018 - YA 2021 Disposal within 3 years after acquisition 30% In the 4 year after acquisition 20% In the 5th year after acquisition 15% After the year 5% WITHOLDING TAX RATES: Contract Interest Royalty Special classes of income Public entertainers Commission / Introduction fee 10% + 3% 15% 10% 10% 15% 10% 50% AGRICULTURE ALLOWANCE RATES Clearing and preparation of land New planting Construction on a farm of a road or bridge 50% 50% Construction on a farm of a building: Used for business - Used for welfare of the employees 10% 20% FOREST ALLOWANCE RATES Road or building used for timber extraction Building provided for employees' 10% 20% A. Higher Power Sdn Bhd (HPSB) is a new tax resident company in Malaysia with its factory located in Nilai, Negeri Sembilan. It was incorporated on 1 July 2021 with a paid-up capital of RM6 million. It prepares its annual Income Statement to 31 December. Soon after HPSB was incorporated, it made an application to Malaysian Investment Development Authority (MIDA) for pioneer status tax incentive. It commenced manufacturing a promoted product ox on 1 August 2021 upon receiving an initial approval from the MIDA. MIDA issued a pioneer certificate when HPSB achieved the stipulated production target. The production date as stated in the pioneer certificate was 1 January 2022. You are a tax manager with KC Tax Consultant Sdn Bhd and had a meeting with the chief accountant of HPSB on 1 September 2021. He provided you with the following projected tax information and the capital expenditures: 2021 2022 2023 2024 2025 2026 RM RM RM RM RM RM (300)| 2,300 Year of Assessment: (in '000) 1. Pre-pioneer business: Adjusted loss Industrial building allowance (IBA) & Capital allowances (CA) 2. Pioneer business: Adjusted income (loss) IBA & CA 3. Rental income Capital expenditures: Land Factory/extension of factory (IBA as above) Plant and machinery (CA as above) (1,000) 4,000 8,000 12,000 14,000 5,000 2,500 2,500 2,500 2,500 200 200 200 200 200 5,000 6,000 4,000 5,000 10,000 Required: State the total chargeable income and the total exempt income respectively for the pioneer period from the year of assessment 2021 to the year of assessment 2026. (14 marks) B. You are the tax partner of Yes Tax Consultant Sdn Bhd, a firm of tax accountants carrying on their business at No. 41, Jalan Pria, Taman Maluri, Kuala Lumpur. On 12 April 2020, you had a meeting with your client, Mr Kyle, the financial controller from Coloratura Sdn Bhd (CSB). The office of the client is situated at No. 11, Jalan 4/76, Bandar Baru Bangi, Selangor. At the meeting, you and Mr Kyle discussed matters relating to the availability of reinvestment allowance (RA) incentive for CSB. Mr Kyle had provided you the following information: CSB, a tax resident company has been operating its business of manufacturing canned food products in Cheras, Kuala Lumpur since 2011. Its financial year end is 31 December. It planned to expand its business by automating its production lines starting from 2021 The projected figures for income and expenditure for the next 3 years of assessment from year of assessment 2021 are as follows: Year of Assessment 2023 2021 2022 RM'000 RM'000 (800) 6,000 100 100 RM'000 8,000 Adjusted income (loss) from business Interest income from deposit in a local bank 100 50 50 Expenditure incurred for RA purposes: Machinery (Note 1) Machinery (Note 2) Machinery (Note 3) Completion of a factory in 2023 (Note 3) 200 2,000 2.000 5,000 8,000 Industrial building allowance (IBA) and capital allowance (CA) due IBA and CA for the year of assessment 1,800 1,400 3,500 1. Notes: These are leased assets. 2. It is to be purchased from a wholly owned subsidiary company of CSB. 3. These are to be incurred for the qualifying project for RA incentive. Required: Computed a projected tax computations for the 3 years of assessments 2021 - 2023. Note: You are to assume that the income tax rate is 24% for all the years of assessments. Detail workings are to be shown to support the tax computations. Marks will be awarded for the at of the letter and the effectiveness of communication. (12 marks) [26 marks) TAX RATES AND ALLOWANCES The following tax rates, allowances and values are to be used in answering the questions. Income tax rates Chargeable income Resident company Paid up ordinary share capital First Excess over RM600,000 RM600,000 RM2,500,000 or less 17% 24% More than RM2,500,000 24% 24% Capital allowances Initial Annual allowance allowance (IA) (AA) Rate % Rate % Industrial buildings 10 3 Plant and machinery - general 20 14 Motor vehicles and heavy machinery 20 20 Office equipment, furniture and fittings 20 10 REAL PROPERTY GAINS TAX RATE - INDIVIDUAL OF MALAYSIAN CITIZEN YA 2018 - YA 2021 Disposal within 3 years after acquisition 30% In the 4 year after acquisition 20% In the 5th year after acquisition 15% After the year 5% WITHOLDING TAX RATES: Contract Interest Royalty Special classes of income Public entertainers Commission / Introduction fee 10% + 3% 15% 10% 10% 15% 10% 50% AGRICULTURE ALLOWANCE RATES Clearing and preparation of land New planting Construction on a farm of a road or bridge 50% 50% Construction on a farm of a building: Used for business - Used for welfare of the employees 10% 20% FOREST ALLOWANCE RATES Road or building used for timber extraction Building provided for employees' 10% 20%