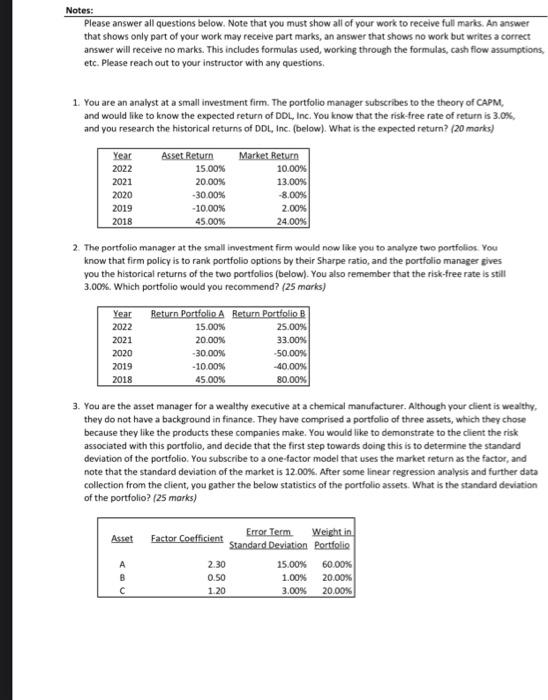

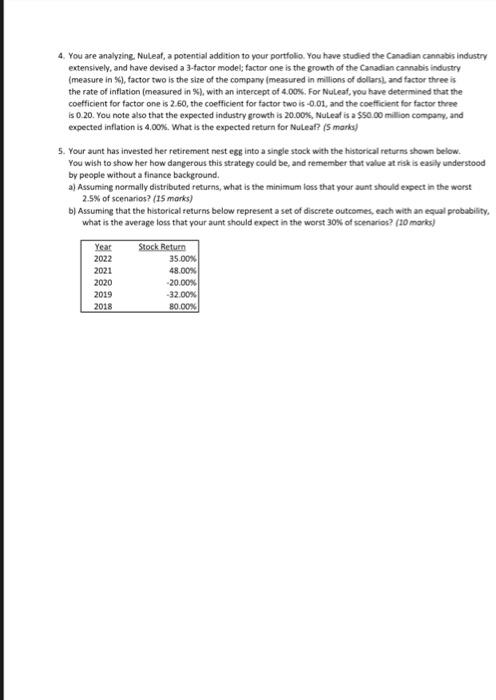

Notes: Please answer all questions below. Note that you must show all of your work to receive full marks. An answer that shows only part of your work may receive part marks, an answer that shows no work but writes a correct answer will receive no marks. This includes formulas used, working through the formulas, cash flow assumptions, etc. Please reach out to your instructor with any questions. 1. You are an analyst at a small investment firm. The portfolio manager subscribes to the theory of CAPM, and would like to know the expected return of DDL, Inc. You know that the risk-free rate of return is 3.0K, and you research the historical returns of DDL, Inc. (below). What is the expected return? (20 marks) 2. The portfolio manager at the small investment firm would now like you to analyre two portfolios. You know that firm policy is to rank portfolio options by their Sharpe ratio, and the portfolio manager gives you the historical returns of the two portfolios (below). You also remember that the risk-free rate is still 3.00%. Which portfolio would you recommend? (25 marks) 3. You are the asset manager for a wealthy executive at a chemical manufacturer. Although your client is wealthy, they do not have a background in finance. They have comprised a portfolio of three assets, which they chose because they like the products these companies make. You would like to demonstrate to the client the risk associated with this portfolio, and decide that the first step towards doing this is to determine the standard deviation of the portfolio. You subscribe to a one-factor model that uses the market return as the factor, and note that the standard deviation of the market is 12.00%. After some linear regression analysis and further data collection from the client, you gather the below statistics of the portfolio assets. What is the standard deviation of the portfolio? (25 marks) 4. You are analyzing. Nuleaf, a potential addition to your portfolia. You have studied the Canadian cannabis industry extensively, and have devised a 3-factor model; factor one is the growth of the Canadian cannabis industry (measure in % ), factor two is the size of the company (measured in millions of dollars), and factor three is the rate of inflation (measured in S ), with an intercept of 4.00K. For Nuleaf, you bave determined that the coefficient for factor one is 2.60 , the coefficient for factor two is -0.01 , and the coefficient for factor three is 0.20 . You note also that the expected industry growth is 20.00%, Nuteaf is a $50.00 million company, and expected inflation is 4,005 . What is the expected return for Nuteaf? (S marks) 5. Your aunt has imvested her retirement nest egg into a single stock with the hiatorical returns shown below. You wish to show her how dangerous this strategy could be, and remember that value at risk is easily understood by people without a finance background. a) Assuming normally distributed returns, what is the minimum loss that your aunt should expect in the worst 2.5% of scenarios? (15 morks) b) Assuming that the historical returns below represent a set of discrete outcomes, each with an equal probability. what is the average loss that your aunt should expect in the worst 30% of scenarios? (10 moris)