Question

Now that Gome had a publicly listed shell (China Eagle), Wong Kwongyu needed to make two critical decisions. First of all, should he push through

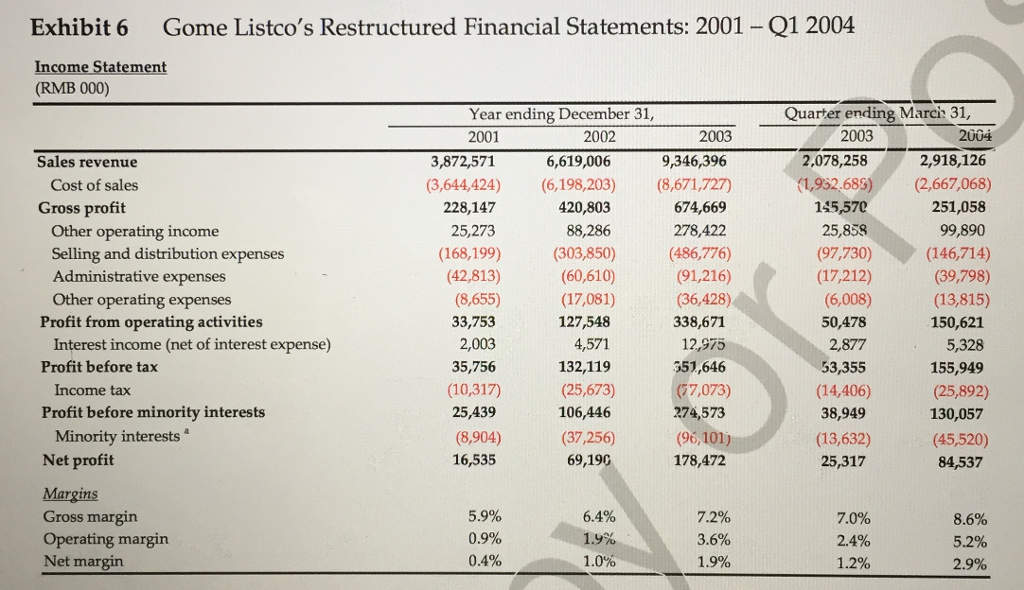

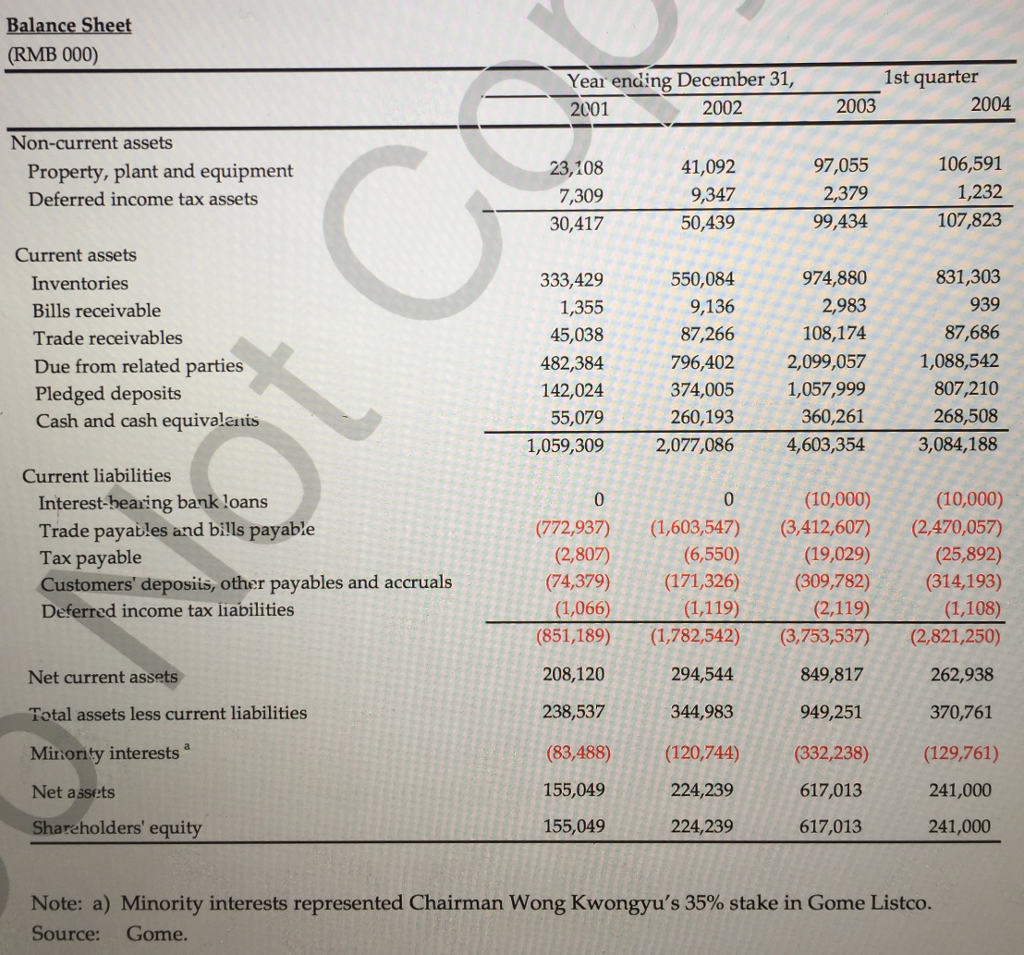

Now that Gome had a publicly listed shell (China Eagle), Wong Kwongyu needed to make two critical decisions. First of all, should he push through with the backdoor listing strategy or shift gears to go public via a traditional IPO? Structuring these elaborate deals had, over the past four years, consumed tremendous amounts of Wongs energy and ingenuity. But he was only half way through. Completing the second half of the process could demand even more attention from Wong and his senior team, all at a time when their undivided focus on key operating issues was imperative. It was a valid question to ask whether this unconventional path was really worth all the trouble. Second, if Wong decided to move ahead with a backdoor listing, he may have to engineer a restructuring of Gomes current assets. Gomes financial advisors proposed taking the following sequential steps: Select a subset of the 139 retail outlets under Gome at the end of 2003. These outlets should enjoy higher profitability, greater market shares and less competition. They represented Gomes best retail assets and should be packaged into a holding company (Gome Listco) which would go public through a reverse takeover. Exhibit 6 contains the restructured historical financial statements for Gome Listco.

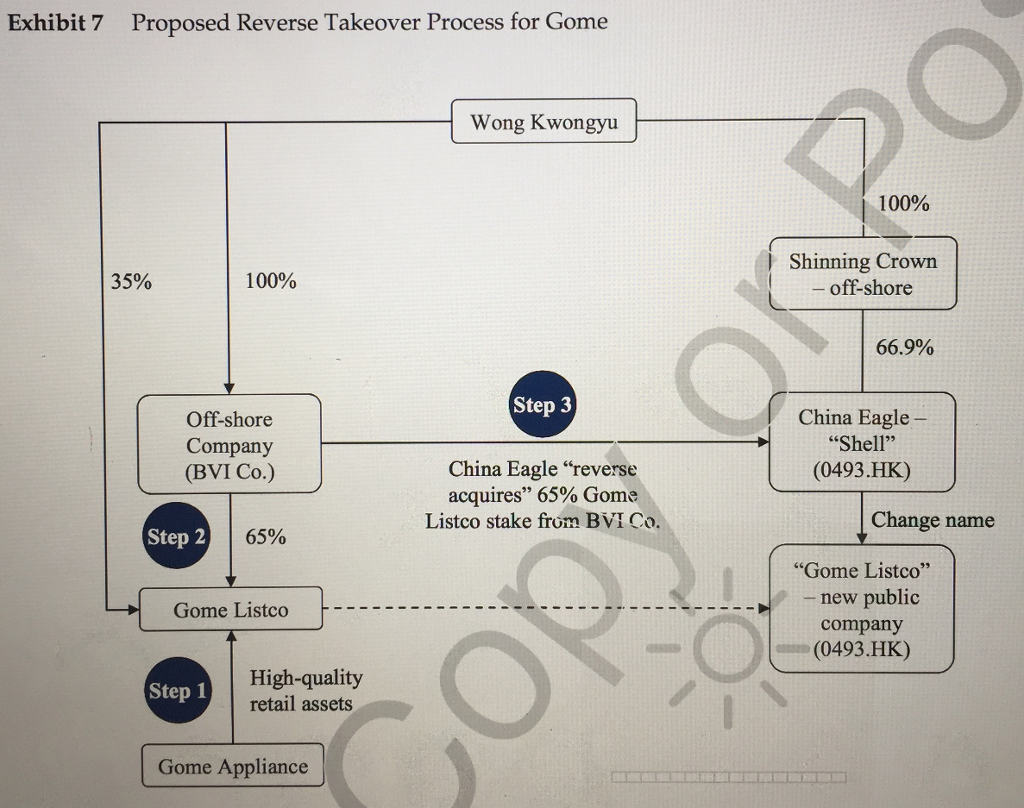

Wong Kwongyu himself should hold 35% of Gome Listco while the remaining 65% could be sold off to an off-shore private company controlled by Wong (BVI Co.), thereby qualifying Gome Listco as a joint-venture retailer in China.18

Let China Eagle, the shell company, acquire the 65% Gome Listco stake from BVI Co., consummating the reverse takeover. As a result, Gome Listco would formally gain the listing status from China Eagle and become a publicly traded company on the Hong Kong Stock Exchange (see Exhibit 7 for a summary of the proposed reverse takeover process and Exhibit 8 for information on relevant peer companies for Gome Listco).

Mr. Wong liked this plan but he wondered if there were too many moving pieces here. For competitive reasons, he would like to have Gome listed through front door or back door by the end of 2004. Any delay would force him to play catch-up, financially and strategically, with major competitors within and outside China.

Q: What is the percentage of Mr. Wong's holdings of the final new public company "Gome Listco"?

Exhibit 6 Gome Listco's Restructured Financial Statements: 2001 Q1 2004 Income Statement (RMB 000) Quarter ending Marci 31. Year ending December 31, 2004 2002 2003 2003 2001 2,918,126 9,346,396 2,078,258 Sales revenue 3,872,571 6,619,006 1,932,689) (2,667,068) Cost of sales (3,644,424) (6,198,203) (8,671,727) 420,803 674,669 251,058 Gross profit 228,147 135,57C 99,890 88,286 278,422 25,858 Other operating income 25,273 (303,850) (146,714) Selling and distribution expenses (168,199) (486,776) (97,730) (60,610) (39,798) (42,813) (91,216) (17,212) Administrative expenses (8,655) (36,428) Other operating expenses (17,081) (6,008) Profit from operating activities 33,753 127,548 338,671 50,478 150,621 2,003 Interest income (net of interest expense) 4,571 12,975 2,877 5,328 Profit before tax 132,119 35,756 353,646 53,355 155,949 (25,673) Income tax (77,073) (14,406) (25,892) Profit before minority interests 25,439 106,446 274,573 38,949 130,057 Minority interests (96,101) (8,904) (37,256) (13,632) (45,520) Net profit 16,535 69,19C 178,472 25,317 84,537 Margins 5.9% 6.4% 7.2%. Gross margin 7.0% 8.6% Operating margin 0.9% 3.6% 2.4% 5.2% 0.4% Net margin 1.0% 1.9%. 1.2%. 2.9% Exhibit 6 Gome Listco's Restructured Financial Statements: 2001 Q1 2004 Income Statement (RMB 000) Quarter ending Marci 31. Year ending December 31, 2004 2002 2003 2003 2001 2,918,126 9,346,396 2,078,258 Sales revenue 3,872,571 6,619,006 1,932,689) (2,667,068) Cost of sales (3,644,424) (6,198,203) (8,671,727) 420,803 674,669 251,058 Gross profit 228,147 135,57C 99,890 88,286 278,422 25,858 Other operating income 25,273 (303,850) (146,714) Selling and distribution expenses (168,199) (486,776) (97,730) (60,610) (39,798) (42,813) (91,216) (17,212) Administrative expenses (8,655) (36,428) Other operating expenses (17,081) (6,008) Profit from operating activities 33,753 127,548 338,671 50,478 150,621 2,003 Interest income (net of interest expense) 4,571 12,975 2,877 5,328 Profit before tax 132,119 35,756 353,646 53,355 155,949 (25,673) Income tax (77,073) (14,406) (25,892) Profit before minority interests 25,439 106,446 274,573 38,949 130,057 Minority interests (96,101) (8,904) (37,256) (13,632) (45,520) Net profit 16,535 69,19C 178,472 25,317 84,537 Margins 5.9% 6.4% 7.2%. Gross margin 7.0% 8.6% Operating margin 0.9% 3.6% 2.4% 5.2% 0.4% Net margin 1.0% 1.9%. 1.2%. 2.9%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance In Theory And Practice

Authors: Holley Ulbrich

1st Edition

0324016603, 978-0324016604