Answered step by step

Verified Expert Solution

Question

1 Approved Answer

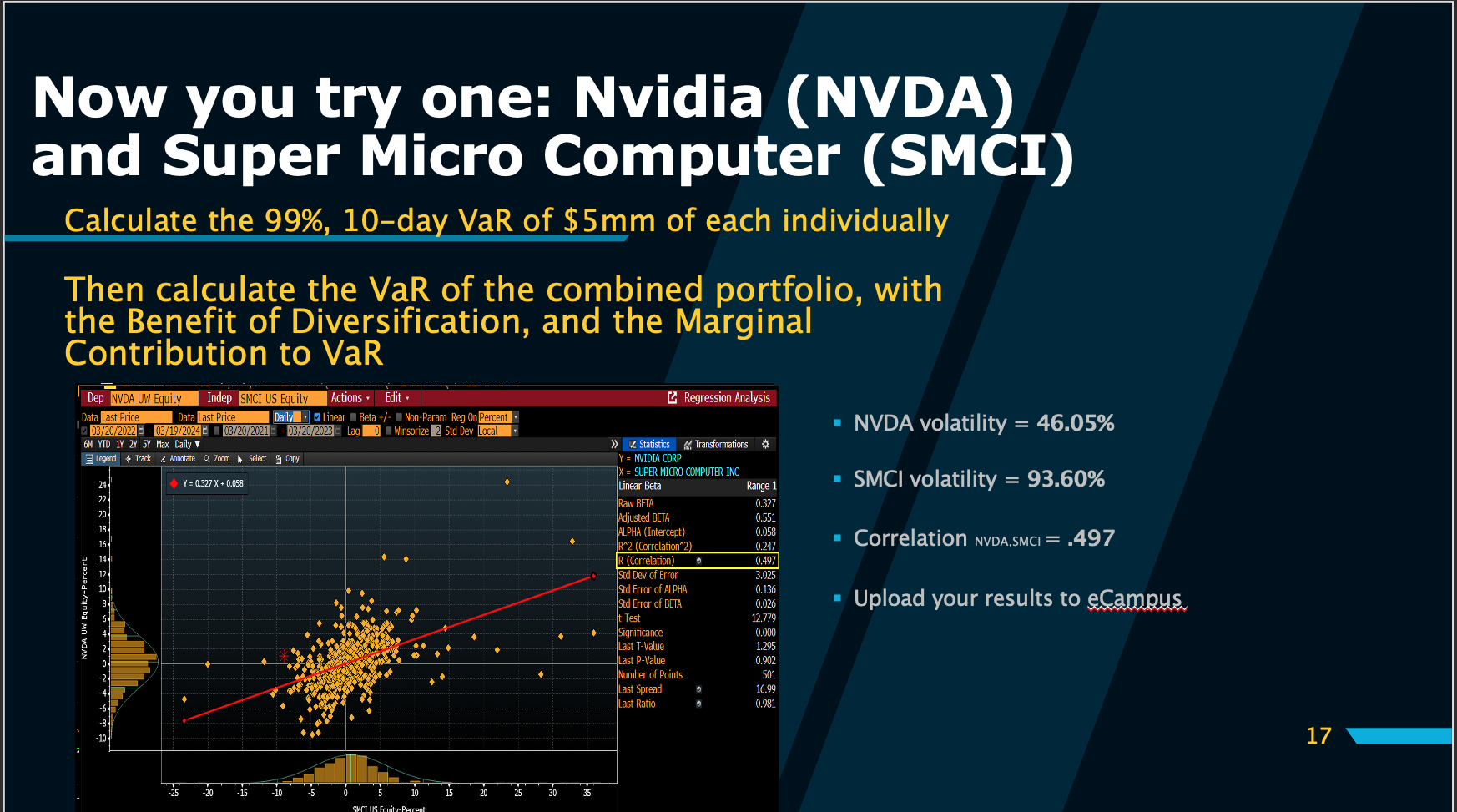

Now you try one: Nvidia ( NVDA ) and Super Micro Computer ( SMCI ) Calculate the 9 9 % , 1 0 - day

Now you try one: Nvidia NVDA and Super Micro Computer SMCI

Calculate the day VaR of $ of each individually

Then calculate the VaR of the combined portfolio, with the Benefit of Diversification, and the Marginal Contribution to VaR

NVDA volatility

SMCI volatility

Correlation NVDA,SMCI

Steps done in excel!!!!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Budget Building Book For Nonprofits

Authors: Murray Dropkin, Jim Halpin, Bill La Touche

2nd Edition

0787996033, 978-0787996031