Answered step by step

Verified Expert Solution

Question

1 Approved Answer

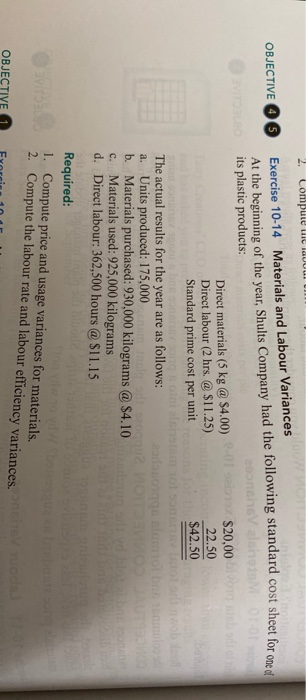

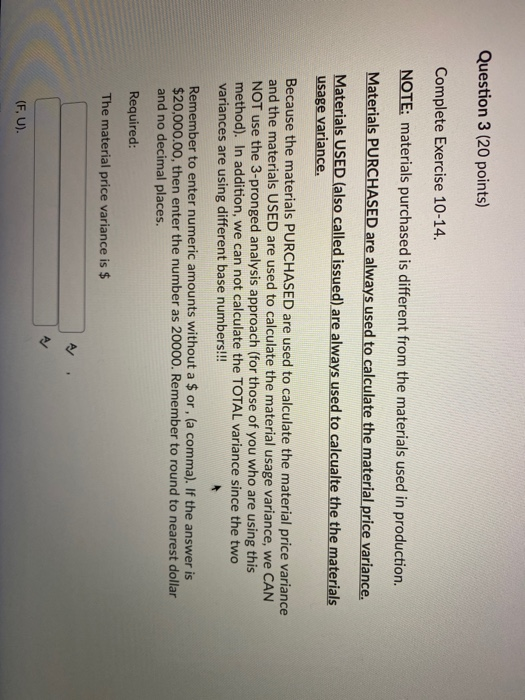

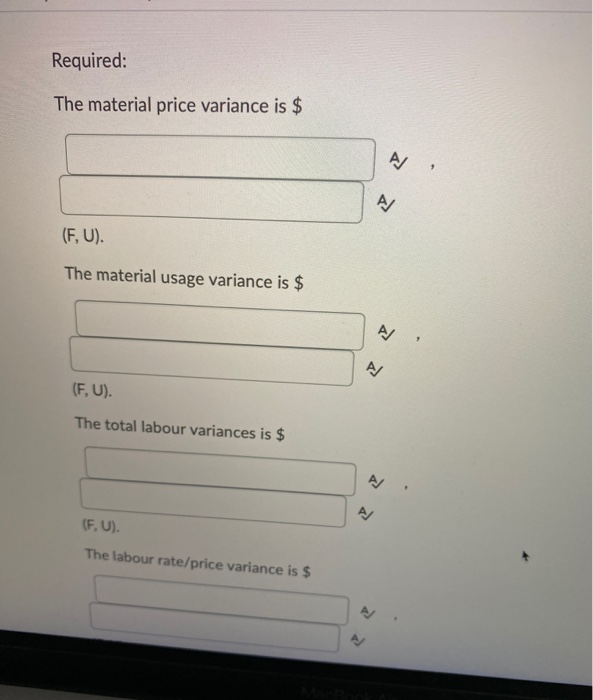

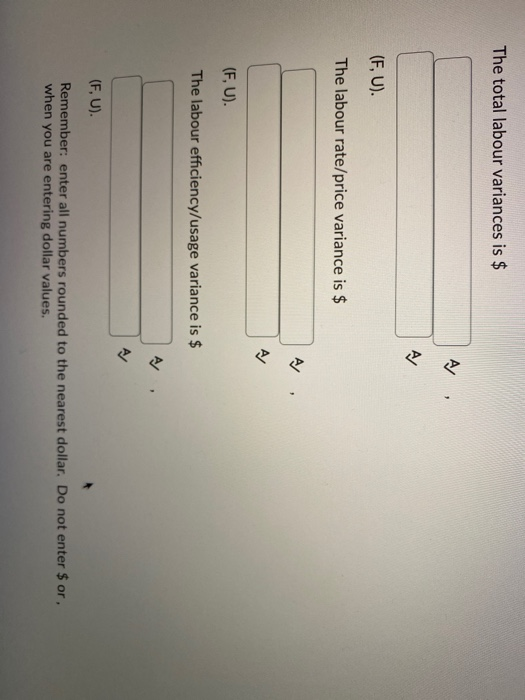

OBJECTIVE 2. Compute uit laul Exercise 10-14 Materials and Labour Variances At the beginning of the year, Shults Company had the following standard cost sheet

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Medical Record Auditor A Guide To Improving Clinical Documentation In A Changing Health Environment

Authors: Deborah J. Grider

4th Edition

1622021010, 978-1622021017