Answered step by step

Verified Expert Solution

Question

1 Approved Answer

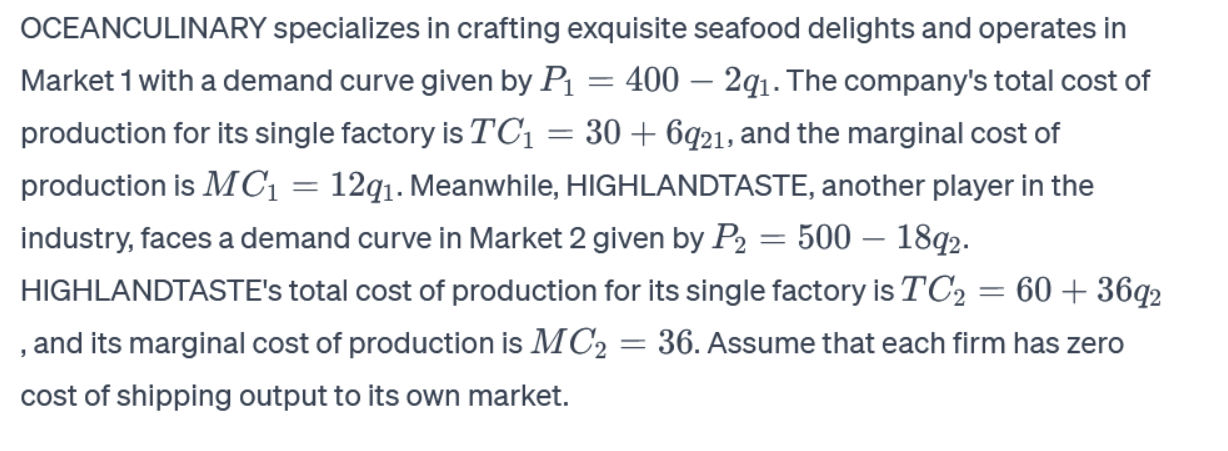

OCEANCULINARY specializes in crafting exquisite seafood delights and operates in Market 1 with a demand curve given by P1 production for its single factory

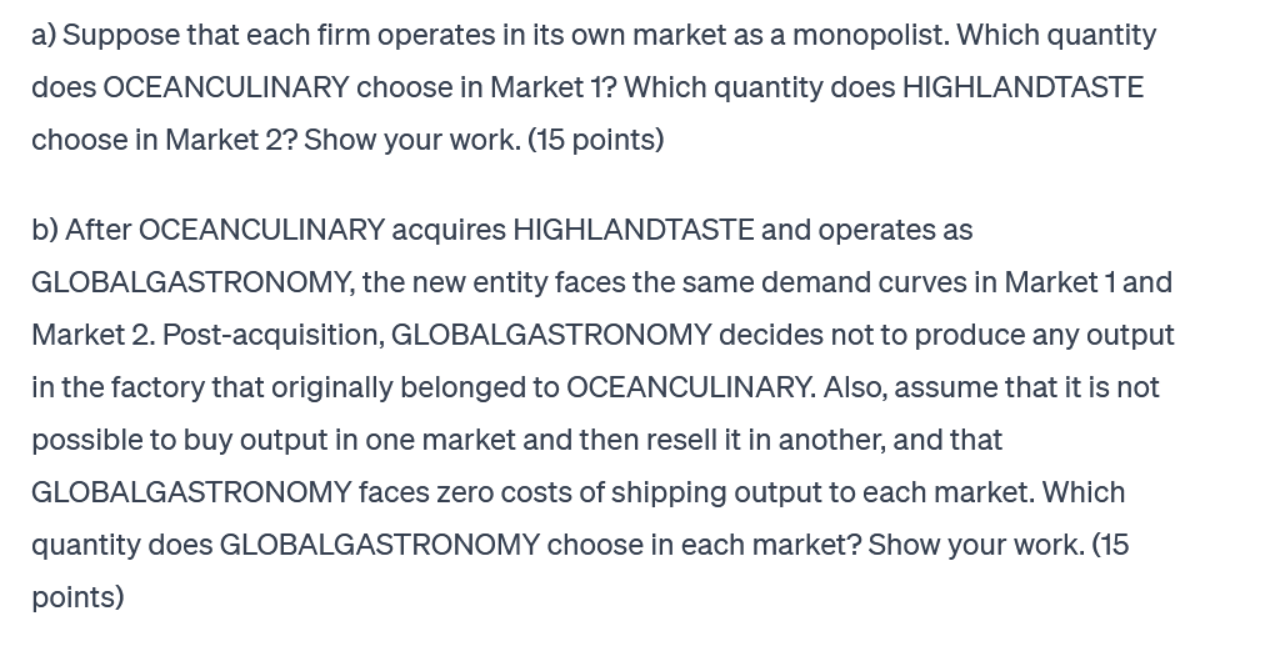

OCEANCULINARY specializes in crafting exquisite seafood delights and operates in Market 1 with a demand curve given by P1 production for its single factory is TC1 = = 400 291. The company's total cost of 30+ 6921, and the marginal cost of production is MC = 12q1. Meanwhile, HIGHLANDTASTE, another player in the industry, faces a demand curve in Market 2 given by P2 = 500 - 18q2. HIGHLANDTASTE's total cost of production for its single factory is TC = 60 + 36q2 = 36. Assume that each firm has zero and its marginal cost of production is MC2 cost of shipping output to its own market. a) Suppose that each firm operates in its own market as a monopolist. Which quantity does OCEANCULINARY choose in Market 1? Which quantity does HIGHLANDTASTE choose in Market 2? Show your work. (15 points) b) After OCEANCULINARY acquires HIGHLANDTASTE and operates as GLOBALGASTRONOMY, the new entity faces the same demand curves in Market 1 and Market 2. Post-acquisition, GLOBALGASTRONOMY decides not to produce any output in the factory that originally belonged to OCEANCULINARY. Also, assume that it is not possible to buy output in one market and then resell it in another, and that GLOBALGASTRONOMY faces zero costs of shipping output to each market. Which quantity does GLOBALGASTRONOMY choose in each market? Show your work. (15 points)

Step by Step Solution

★★★★★

3.41 Rating (148 Votes )

There are 3 Steps involved in it

Step: 1

a Monopolist Quantity Choice For OCEANCULINARY in Market 1 Market 1 Demand P 400 2q MC 12q To determ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Microeconomics

Authors: Hal R. Varian

9th edition

978-0393123975, 393123979, 393123960, 978-0393919677, 393919676, 978-0393123968