Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Old MathJax webview how to get these answers for a,b, c Problem #18 (9 points) Below is the regression output of a single index model

Old MathJax webview

how to get these answers for a,b,c

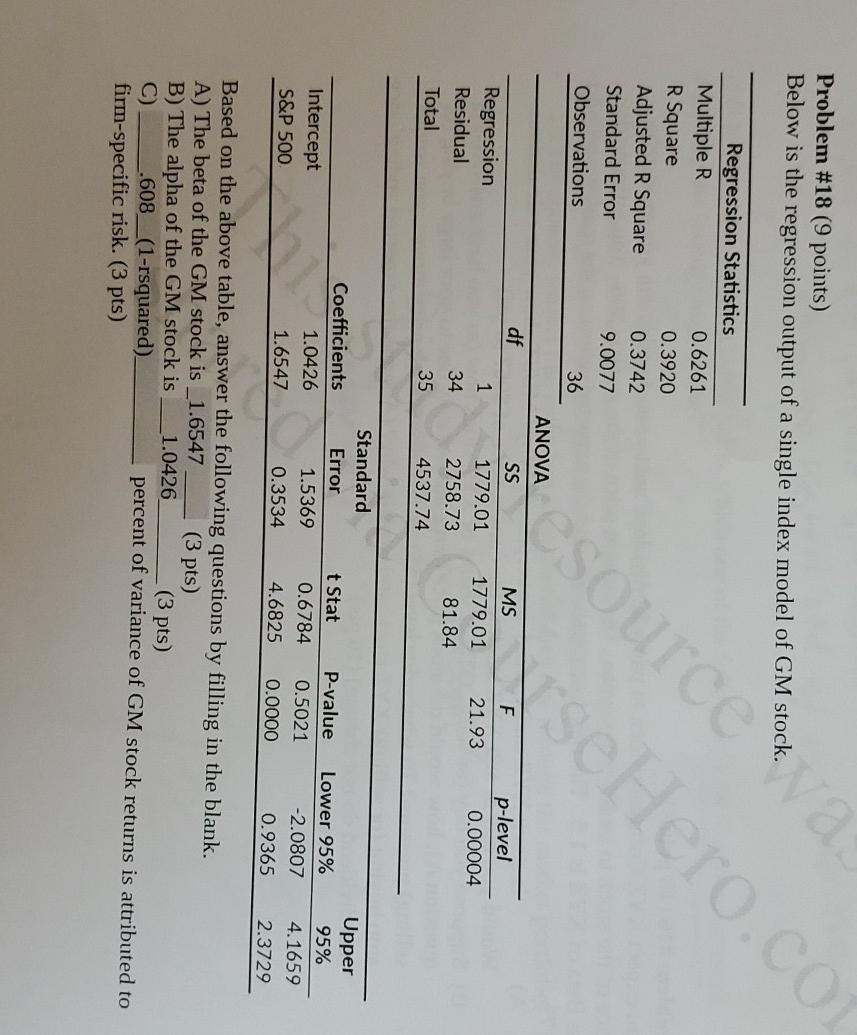

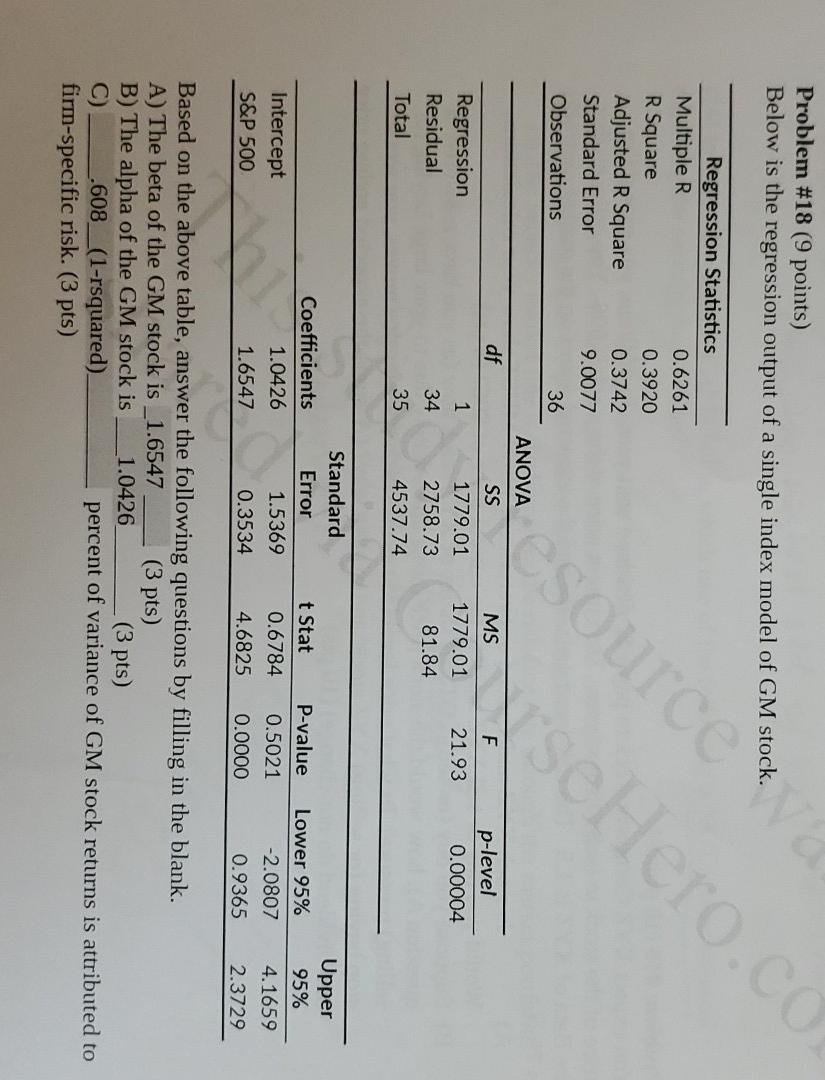

Problem #18 (9 points) Below is the regression output of a single index model of GM stock. Regression Statistics Multiple R 0.6261 R Square 0.3920 Adjusted R Square 0.3742 Standard Error 9.0077 Observations 36 source Hero.co df 1 ANOVA SS 1779.01 2758.73 4537.74 p-level 0.00004 Regression Residual Total MS 1779.01 81.84 21.93 34 35 Intercept S&P 500 Coefficients 1.0426 1.6547 Standard Error 1.5369 0.3534 t Stat 0.6784 4.6825 P-value 0.5021 0.0000 Lower 95% -2.0807 0.9365 Upper 95% 4.1659 2.3729 Based on the above table, answer the following questions by filling in the blank. A) The beta of the GM stock is _1.6547 (3 pts) B) The alpha of the GM stock is 1.0426 (3 pts) C) .608_(1-rsquared) percent of variance of GM stock returns is attributed to firm-specific risk. (3 pts) Problem #18 (9 points) Below is the regression output of a single index model of GM stock. Regression Statistics Multiple R 0.6261 R Square 0.3920 Adjusted R Square 0.3742 Standard Error 9.0077 Observations 36 ANOVA SS df esource Hero.co p-level 0.00004 1 MS 1779.01 81.84 Regression Residual Total 21.93 1779.01 2758.73 4537.74 34 35 Standard Error 1.5369 Upper 95% Coefficients 1.0426 1.6547 t Stat 0.6784 Intercept S&P 500 P-value 0.5021 0.0000 Lower 95% -2.0807 0.9365 4.1659 0.3534 4.6825 2.3729 Based on the above table, answer the following questions by filling in the blank. A) The beta of the GM stock is_1.6547 (3 pts) B) The alpha of the GM stock is 1.0426 (3 pts) C) .608_(1-rsquared). percent of variance of GM stock returns is attributed to firm-specific risk. (3 pts)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance

Authors: Steven G. Medema, Carl Sumner Shoup

1st Edition

0202307859, 978-0202307855