Answered step by step

Verified Expert Solution

Question

1 Approved Answer

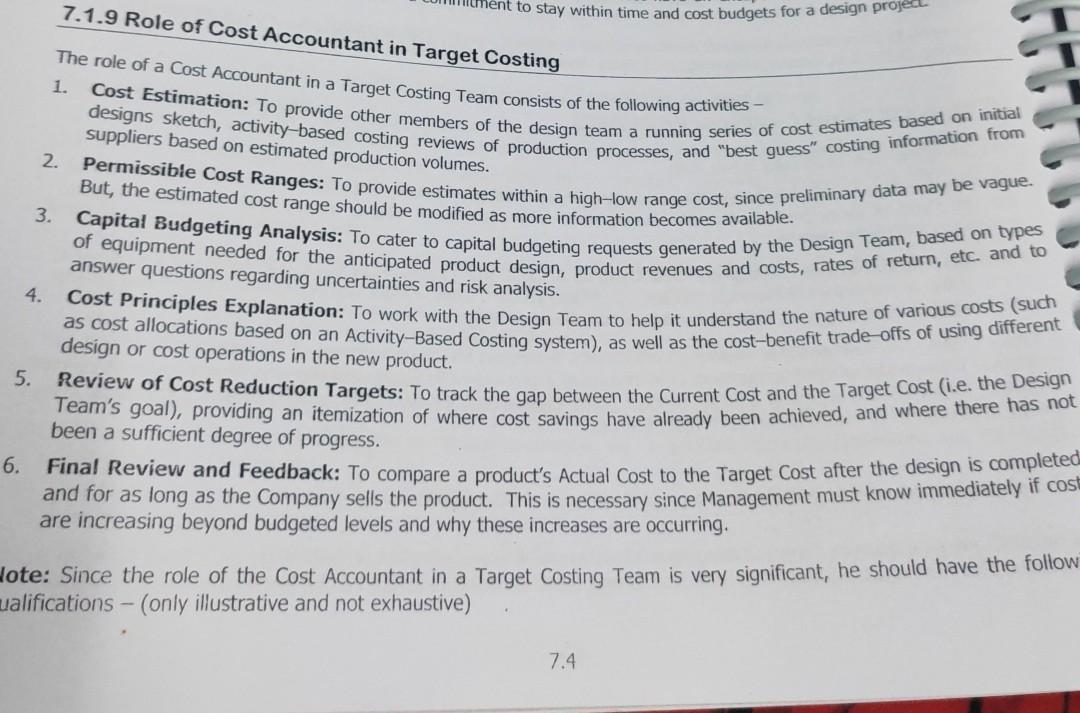

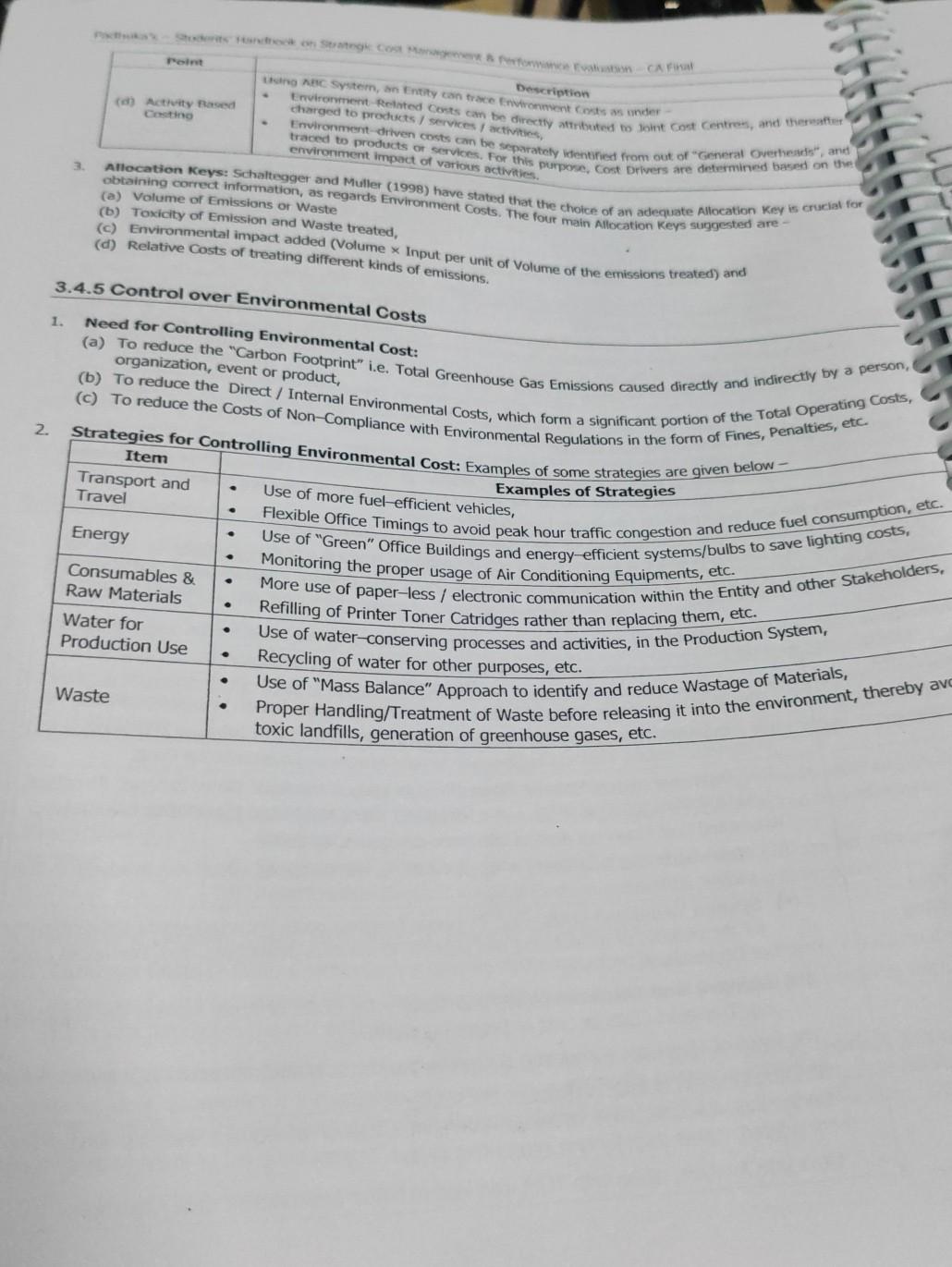

Old MathJax webview if wrong be ready for 5 dislikes full question N 15 in Service Sector 1. Target Costing is applicable for Service Sector

Old MathJax webview

if wrong be ready for 5 dislikes

full question

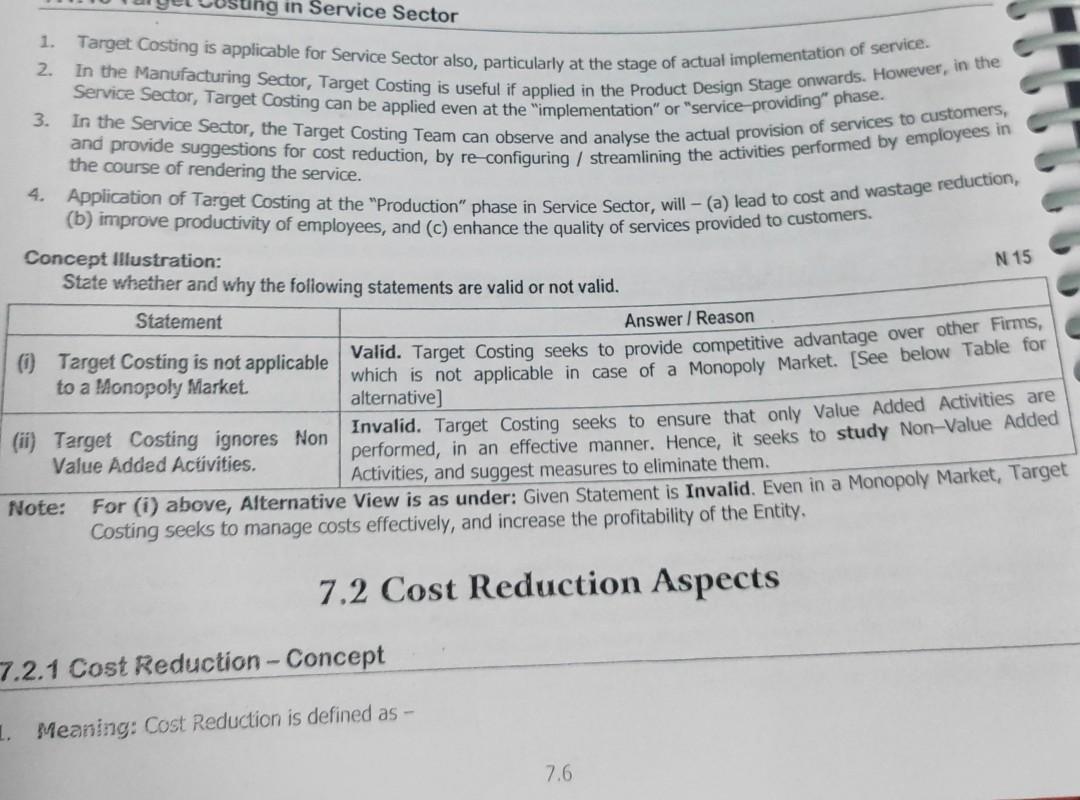

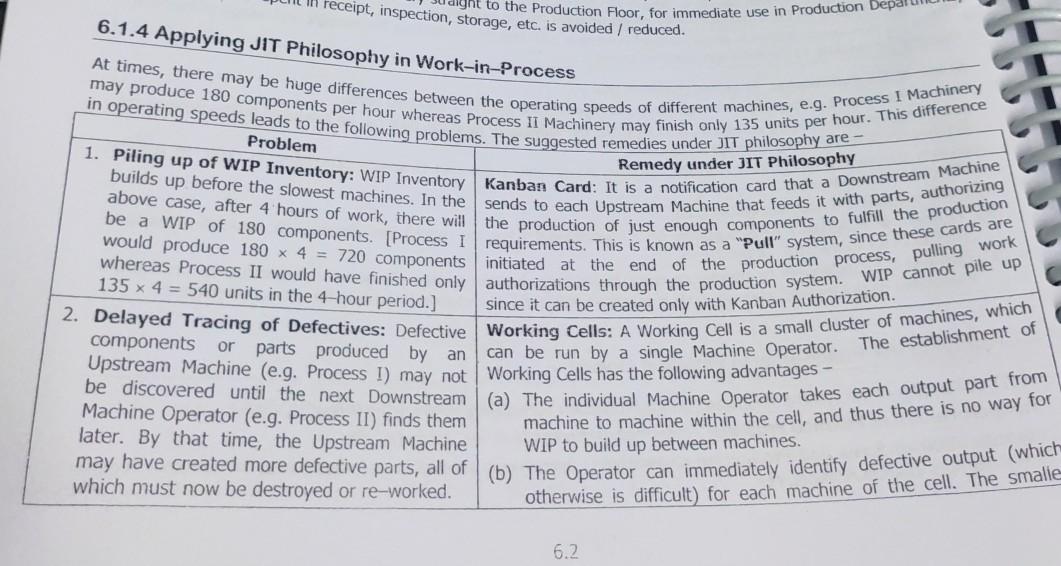

N 15 in Service Sector 1. Target Costing is applicable for Service Sector also, particularly at the stage of actual implementation of service. 2. Service Sector, Target Costing can be applied even at the "implementation" or "service providing phase. In the Manufacturing Sector, Target Costing is useful if applied in the Product Design Stage onwards. However, in the 3. In the Service Sector, the Target Costing Team can observe and analyse the actual provision of services to customers, and provide suggestions for cost reduction, by re-configuring / streamlining the activities performed by employees in the course of rendering the service. 4. Application of Target Costing at the "Production" phase in Service Sector, will - (a) lead to cost and wastage reduction, (b) improve productivity of employees, and (c) enhance the quality of services provided to customers. Concept Illustration: State whether and why the following statements are valid or not valid. Statement Answer / Reason Valid. Target Costing seeks to provide competitive advantage over other Firms, to a Monopoly Market. Target Costing is not applicable which is not applicable in case of a Monopoly Market. (See below Table for alternative] (ii) Target Costing ignores Non Invalid. Target Costing seeks to ensure that only Value Added Activities are Value Added Activities. performed, in an effective manner. Hence, it seeks to study Non-Value Added Activities, and suggest measures to eliminate them. Note: For (i) above, Alternative View is as under: Given Statement is Invalid. Even in a Monopoly Market, Target Costing seeks to manage costs effectively, and increase the profitability of the Entity, 7.2 Cost Reduction Aspects 7.2.1 Cost Reduction - Concept 1. Meaning: Cost Reduction is defined as - 7.6 7.1.9 Role of Cost Accountant in Target Costing went to stay within time and cost budgets for a design projed The role of a Cost Accountant in a Target Costing Team consists of the following activities 1. suppliers based on estimated production volumes. 3. Cost Estimation: To provide other members of the design team a running series of cost estimates based on initial designs sketch, activity-based costing reviews of production processes, and "best guess" costing information from 2. But, the estimated cost range should be modified as more information becomes available. Permissible Cost Ranges: To provide estimates within a high-low range cost, since preliminary data may be vague. of equipment needed for the anticipated product design, product revenues and costs, rates of return, etc. and to answer questions regarding uncertainties and risk analysis. Capital Budgeting Analysis: To cater to capital budgeting requests generated by the Design Team, based on types 4. Cost Principles Explanation: To work with the Design Team to help it understand the nature of various costs (such as cost allocations based on an Activity-Based Costing system), as well as the cost-benefit trade-offs of using different design or cost operations in the new product. 5. Team's goal), providing an itemization of where cost savings have already been achieved, and where there has not been a sufficient degree of progress. 6. Review of Cost Reduction Targets: To track the gap between the Current Cost and the Target Cost (ie the masinet Final Review and Feedback: To compare a product's Actual Cost to the Target Cost after the design is completed and for as long as the Company sells the product. This is necessary since Management must know immediately if cost are increasing beyond budgeted levels and why these increases are occurring. Hote: Since the role of the Cost Accountant in a Target Costing Team is very significant, he should have the follow ualifications - (only illustrative and not exhaustive) 7.4 receipt, inspection, storage, etc. is avoided / reduced. stor to the Production Floor, for immediate use in Production Depan 6.1.4 Applying JIT Philosophy in Work-in-Process Problem At times, there may be huge differences between the operating speeds of different machines, e.g. Process I Machinery in operating speeds leads to the following problems. The suggested remedies under IT philosophy are - may produce 180 components per hour whereas Process II Machinery may finish only 135 units per hour. This difference 1. Piling up of WIP Inventory: WIP Inventory Kanban Card: It is a notification card that a Downstream Machine Remedy under JIT Philosophy above case, after 4 hours of work, there will the production of just enough components to fulfill the production builds up before the slowest machines. In the sends to each Upstream Machine that feeds it with parts, authorizing would produce 180 x 4 = 720 components initiated at the end of the production process, pulling work be a WIP of 180 components. [Process I requirements. This is known as a "Pull" system, since these cards are 135 x 4 = 540 units in the 4-hour period.] since it can be created only with Kanban Authorization. 2. Delayed Tracing of Defectives: Defective Working Cells: A Working Cell is a small cluster of machines, which components or parts produced by an Upstream Machine (e.g. Process I) may not working Cells has the following advantages - can be run by a single Machine Operator. The establishment of be discovered until the next Downstream (a) The individual Machine Operator takes each output part from Machine Operator (e.g. Process II) finds them . WIP to build up between machines. WIP cannot pile up machine to machine within the cell, and thus there is no way for may have created more defective parts, all of (b) The Operator can immediately identify defective output cwanie which must now be destroyed or re-worked. otherwise is difficult) for each machine of the cell. The smalle 6.2 6.1.4 Applying JIT Philosophy in Work-in-Process age, etc. is avoided / reduced. Problem At times, there may be huge differences between the operating speeds of different machines, e.g. Process I Machinery may produce 180 components per hour whereas Process II Machinery may finish only 135 units per hour. This difference in operating speeds leads to the following problems. The suggested remedies under IT philosophy are - 1. Piling up of WIP Inventory: WIP Inventory Kanban Card: It is a notification card that a Downstream Machine Remedy under JIT Philosophy above case, after 4 hours of work, there will the production of just enough components to fulfill the production builds up before the slowest machines. In the sends to each Upstream Machine that feeds it with parts, authorizing would produce 180 x 4 = 720 components initiated at the end of the production process, pulling work be a WIP of 180 components. [Process I requirements. This is known as a "Pull" system, since these cards are whereas Process II would have finished only authorizations through the production system. WIP cannot pile up since it can be created only with Kanban Authorization 2. Delayed Tracing of Defectives: Defective Working Cells: A Working Cell is a small cluster of machines, which components or parts produced by an Upstream Machine (e.g. Process 1) may not working Cells has the following advantages - can be run by a single Machine Operator. The establishment of be discovered until the next Downstream (a) The individual Machine Operator takes each output part from Machine Operator (e.g. Process II) finds them later. By that time, the Upstream Machine machine to machine within the cell, and thus there is no way for WIP to build up between machines. may have created more defective parts, all of (b) The Operator can immediately identify defective output (which which must now be destroyed or re-worked. otherwise is difficult for each machine of the cell. The smaller 135 x 4 = 540 units in the 4-hour period.] 6.2 Point Soon St Corporation CA FI Lang ARC System, an Entity can trace Environment is onder Description (1) Activity Based charged to products / services activities, Environment Rented costs can be directly tributed to Joint Cart Centre, and there Casting Environment-driven costs can be separately identified from out of "General Overheads, and traced to products or services. For this purpose, Cost Drivers are determined based on the environment impact of various activities (a) Volume of Emissions or Waste obtaining correct information, as regards Environment Costs. The four main Allocation Keys suggested are- Allocation keys: Schaltegger and Muller (1998) have stated that the choice of an adequate Allocation Key is crucial for (1) Toxicity of Emission and Waste treated, C) Environmental impact added (Volume * Input per unit of Volume of the emissions treated) and (d) Relative Costs of treating different kinds of emissions. 3 3.4.5 Control over Environmental Costs 1. Need for Controlling Environmental Cost: organization, event or product, 2. Item Travel Use of more fuel-efficient vehicles, Energy (a) To reduce the "Carbon Footprint" i.e. Total Greenhouse Gas Emissions caused directly and indirectly by a person, (c) To reduce the Costs of Non-Compliance with Environmental Regulations in the form of Fines, Penalties, etc. (b) To reduce the Direct / Internal Environmental Costs, which form a significant portion of the Total Operating Costs, Strategies for Controlling Environmental Cost: Examples of some strategies are given below - Transport and Examples of Strategies Use of "Green" Office Buildings and energy-efficient systems/bulbs to save lighting costs, Flexible Office Timings to avoid peak hour traffic congestion and reduce fuel consumption, etc. More use of paper-less / electronic communication within the Entity and other Stakeholders, Use of water-conserving processes and activities, in the Production System, Recycling of water for other purposes, etc. Use of "Mass Balance" Approach to identify and reduce Wastage of Materials, toxic landfills, generation of greenhouse gases, etc. Proper Handling/Treatment of Waste before releasing it into the environment, thereby avc Consumables & Raw Materials Water for Production Use Monitoring the proper usage of Air Conditioning Equipments, etc. Refilling of Printer Toner Catridges rather than replacing them, etc. . Waste . N 15 in Service Sector 1. Target Costing is applicable for Service Sector also, particularly at the stage of actual implementation of service. 2. Service Sector, Target Costing can be applied even at the "implementation" or "service providing phase. In the Manufacturing Sector, Target Costing is useful if applied in the Product Design Stage onwards. However, in the 3. In the Service Sector, the Target Costing Team can observe and analyse the actual provision of services to customers, and provide suggestions for cost reduction, by re-configuring / streamlining the activities performed by employees in the course of rendering the service. 4. Application of Target Costing at the "Production" phase in Service Sector, will - (a) lead to cost and wastage reduction, (b) improve productivity of employees, and (c) enhance the quality of services provided to customers. Concept Illustration: State whether and why the following statements are valid or not valid. Statement Answer / Reason Valid. Target Costing seeks to provide competitive advantage over other Firms, to a Monopoly Market. Target Costing is not applicable which is not applicable in case of a Monopoly Market. (See below Table for alternative] (ii) Target Costing ignores Non Invalid. Target Costing seeks to ensure that only Value Added Activities are Value Added Activities. performed, in an effective manner. Hence, it seeks to study Non-Value Added Activities, and suggest measures to eliminate them. Note: For (i) above, Alternative View is as under: Given Statement is Invalid. Even in a Monopoly Market, Target Costing seeks to manage costs effectively, and increase the profitability of the Entity, 7.2 Cost Reduction Aspects 7.2.1 Cost Reduction - Concept 1. Meaning: Cost Reduction is defined as - 7.6 7.1.9 Role of Cost Accountant in Target Costing went to stay within time and cost budgets for a design projed The role of a Cost Accountant in a Target Costing Team consists of the following activities 1. suppliers based on estimated production volumes. 3. Cost Estimation: To provide other members of the design team a running series of cost estimates based on initial designs sketch, activity-based costing reviews of production processes, and "best guess" costing information from 2. But, the estimated cost range should be modified as more information becomes available. Permissible Cost Ranges: To provide estimates within a high-low range cost, since preliminary data may be vague. of equipment needed for the anticipated product design, product revenues and costs, rates of return, etc. and to answer questions regarding uncertainties and risk analysis. Capital Budgeting Analysis: To cater to capital budgeting requests generated by the Design Team, based on types 4. Cost Principles Explanation: To work with the Design Team to help it understand the nature of various costs (such as cost allocations based on an Activity-Based Costing system), as well as the cost-benefit trade-offs of using different design or cost operations in the new product. 5. Team's goal), providing an itemization of where cost savings have already been achieved, and where there has not been a sufficient degree of progress. 6. Review of Cost Reduction Targets: To track the gap between the Current Cost and the Target Cost (ie the masinet Final Review and Feedback: To compare a product's Actual Cost to the Target Cost after the design is completed and for as long as the Company sells the product. This is necessary since Management must know immediately if cost are increasing beyond budgeted levels and why these increases are occurring. Hote: Since the role of the Cost Accountant in a Target Costing Team is very significant, he should have the follow ualifications - (only illustrative and not exhaustive) 7.4 receipt, inspection, storage, etc. is avoided / reduced. stor to the Production Floor, for immediate use in Production Depan 6.1.4 Applying JIT Philosophy in Work-in-Process Problem At times, there may be huge differences between the operating speeds of different machines, e.g. Process I Machinery in operating speeds leads to the following problems. The suggested remedies under IT philosophy are - may produce 180 components per hour whereas Process II Machinery may finish only 135 units per hour. This difference 1. Piling up of WIP Inventory: WIP Inventory Kanban Card: It is a notification card that a Downstream Machine Remedy under JIT Philosophy above case, after 4 hours of work, there will the production of just enough components to fulfill the production builds up before the slowest machines. In the sends to each Upstream Machine that feeds it with parts, authorizing would produce 180 x 4 = 720 components initiated at the end of the production process, pulling work be a WIP of 180 components. [Process I requirements. This is known as a "Pull" system, since these cards are 135 x 4 = 540 units in the 4-hour period.] since it can be created only with Kanban Authorization. 2. Delayed Tracing of Defectives: Defective Working Cells: A Working Cell is a small cluster of machines, which components or parts produced by an Upstream Machine (e.g. Process I) may not working Cells has the following advantages - can be run by a single Machine Operator. The establishment of be discovered until the next Downstream (a) The individual Machine Operator takes each output part from Machine Operator (e.g. Process II) finds them . WIP to build up between machines. WIP cannot pile up machine to machine within the cell, and thus there is no way for may have created more defective parts, all of (b) The Operator can immediately identify defective output cwanie which must now be destroyed or re-worked. otherwise is difficult) for each machine of the cell. The smalle 6.2 6.1.4 Applying JIT Philosophy in Work-in-Process age, etc. is avoided / reduced. Problem At times, there may be huge differences between the operating speeds of different machines, e.g. Process I Machinery may produce 180 components per hour whereas Process II Machinery may finish only 135 units per hour. This difference in operating speeds leads to the following problems. The suggested remedies under IT philosophy are - 1. Piling up of WIP Inventory: WIP Inventory Kanban Card: It is a notification card that a Downstream Machine Remedy under JIT Philosophy above case, after 4 hours of work, there will the production of just enough components to fulfill the production builds up before the slowest machines. In the sends to each Upstream Machine that feeds it with parts, authorizing would produce 180 x 4 = 720 components initiated at the end of the production process, pulling work be a WIP of 180 components. [Process I requirements. This is known as a "Pull" system, since these cards are whereas Process II would have finished only authorizations through the production system. WIP cannot pile up since it can be created only with Kanban Authorization 2. Delayed Tracing of Defectives: Defective Working Cells: A Working Cell is a small cluster of machines, which components or parts produced by an Upstream Machine (e.g. Process 1) may not working Cells has the following advantages - can be run by a single Machine Operator. The establishment of be discovered until the next Downstream (a) The individual Machine Operator takes each output part from Machine Operator (e.g. Process II) finds them later. By that time, the Upstream Machine machine to machine within the cell, and thus there is no way for WIP to build up between machines. may have created more defective parts, all of (b) The Operator can immediately identify defective output (which which must now be destroyed or re-worked. otherwise is difficult for each machine of the cell. The smaller 135 x 4 = 540 units in the 4-hour period.] 6.2 Point Soon St Corporation CA FI Lang ARC System, an Entity can trace Environment is onder Description (1) Activity Based charged to products / services activities, Environment Rented costs can be directly tributed to Joint Cart Centre, and there Casting Environment-driven costs can be separately identified from out of "General Overheads, and traced to products or services. For this purpose, Cost Drivers are determined based on the environment impact of various activities (a) Volume of Emissions or Waste obtaining correct information, as regards Environment Costs. The four main Allocation Keys suggested are- Allocation keys: Schaltegger and Muller (1998) have stated that the choice of an adequate Allocation Key is crucial for (1) Toxicity of Emission and Waste treated, C) Environmental impact added (Volume * Input per unit of Volume of the emissions treated) and (d) Relative Costs of treating different kinds of emissions. 3 3.4.5 Control over Environmental Costs 1. Need for Controlling Environmental Cost: organization, event or product, 2. Item Travel Use of more fuel-efficient vehicles, Energy (a) To reduce the "Carbon Footprint" i.e. Total Greenhouse Gas Emissions caused directly and indirectly by a person, (c) To reduce the Costs of Non-Compliance with Environmental Regulations in the form of Fines, Penalties, etc. (b) To reduce the Direct / Internal Environmental Costs, which form a significant portion of the Total Operating Costs, Strategies for Controlling Environmental Cost: Examples of some strategies are given below - Transport and Examples of Strategies Use of "Green" Office Buildings and energy-efficient systems/bulbs to save lighting costs, Flexible Office Timings to avoid peak hour traffic congestion and reduce fuel consumption, etc. More use of paper-less / electronic communication within the Entity and other Stakeholders, Use of water-conserving processes and activities, in the Production System, Recycling of water for other purposes, etc. Use of "Mass Balance" Approach to identify and reduce Wastage of Materials, toxic landfills, generation of greenhouse gases, etc. Proper Handling/Treatment of Waste before releasing it into the environment, thereby avc Consumables & Raw Materials Water for Production Use Monitoring the proper usage of Air Conditioning Equipments, etc. Refilling of Printer Toner Catridges rather than replacing them, etc. . WasteStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting for Non-Accounting Students

Authors: John R. Dyson

8th Edition

273722972, 978-0273722977