Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Old MathJax webview Old MathJax webview A 3-months forward contract is an agreement where: O One side has the right to buy an asset for

Old MathJax webview

Old MathJax webview

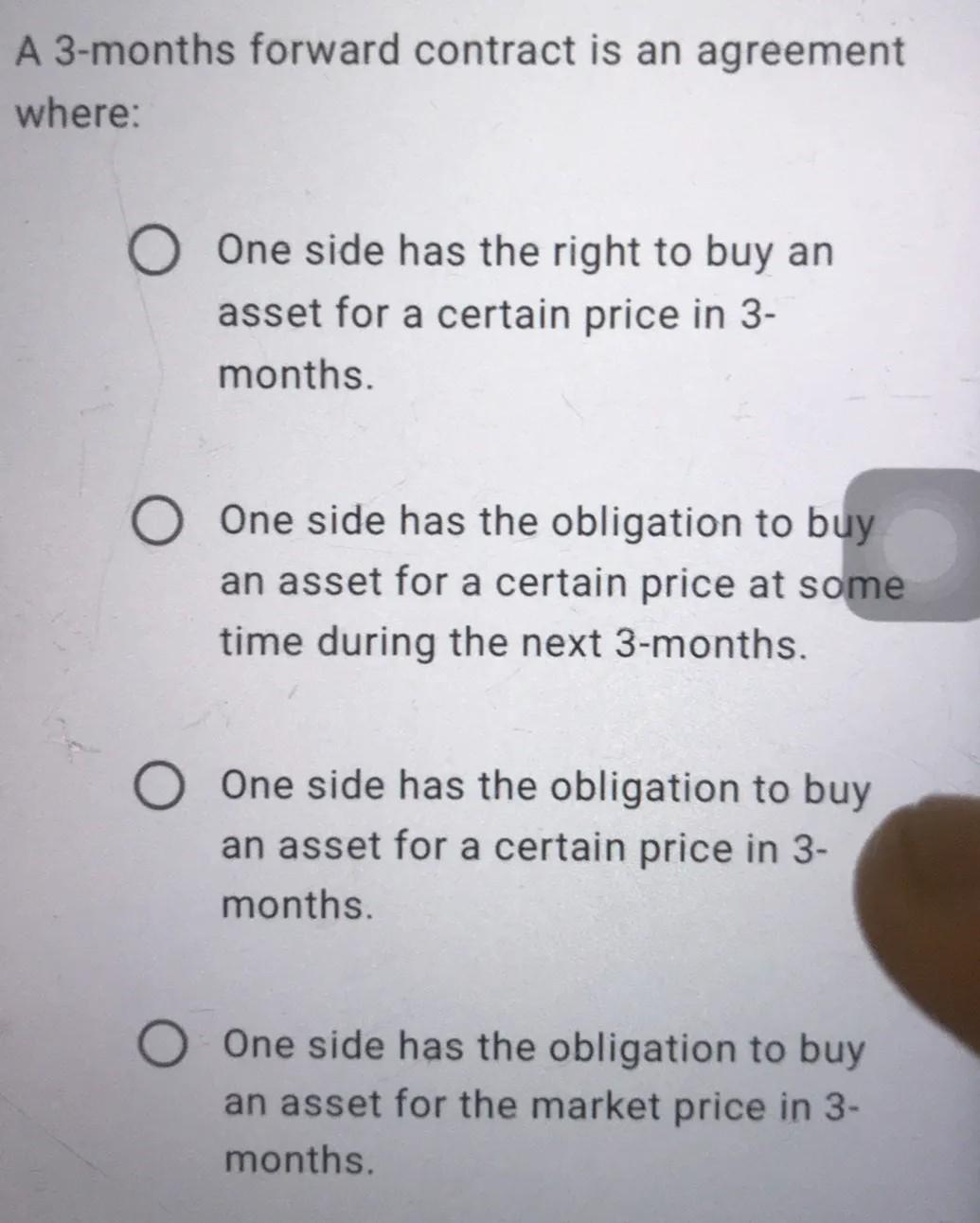

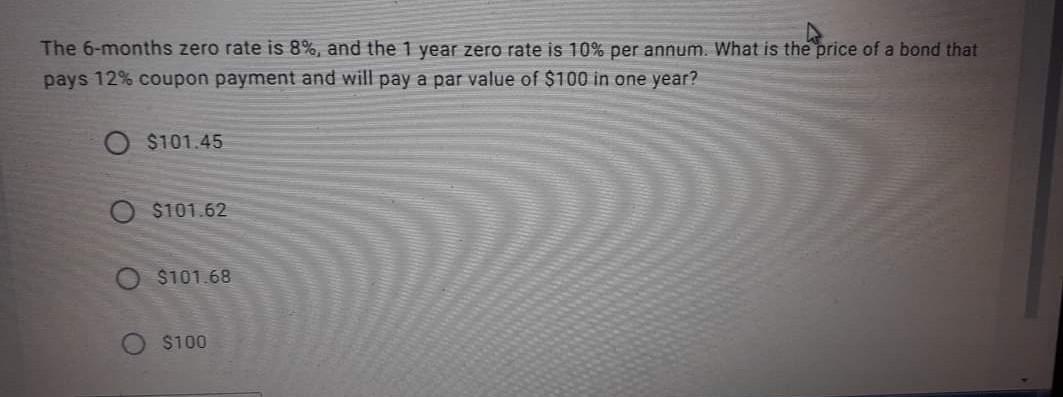

A 3-months forward contract is an agreement where: O One side has the right to buy an asset for a certain price in 3- months. One side has the obligation to buy an asset for a certain price at some time during the next 3-months. O One side has the obligation to buy an asset for a certain price in 3- months. One side has the obligation to buy an asset for the market price in 3- months. The 6-months zero rate is 8%, and the 1 year zero rate is 10% per annum. What is the price of a bond that pays 12% coupon payment and will pay a par value of $100 in one year? O $101.45 $101.62 $101.68 $100 A 3-months forward contract is an agreement where: O One side has the right to buy an asset for a certain price in 3- months. One side has the obligation to buy an asset for a certain price at some time during the next 3-months. O One side has the obligation to buy an asset for a certain price in 3- months. One side has the obligation to buy an asset for the market price in 3- months. The 6-months zero rate is 8%, and the 1 year zero rate is 10% per annum. What is the price of a bond that pays 12% coupon payment and will pay a par value of $100 in one year? O $101.45 $101.62 $101.68 $100

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Inclusive And Sustainable Finance Leadership Ethics And Culture

Authors: Atul K. Shah

1st Edition

0367759403, 978-0367759407