Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Old MathJax webview Old MathJax webview need note on all need all only qurstion is full 000 wi MAR 1000 AN MM -2.000 150.000 100

Old MathJax webview

Old MathJax webview

need note on all

need all only

qurstion is full

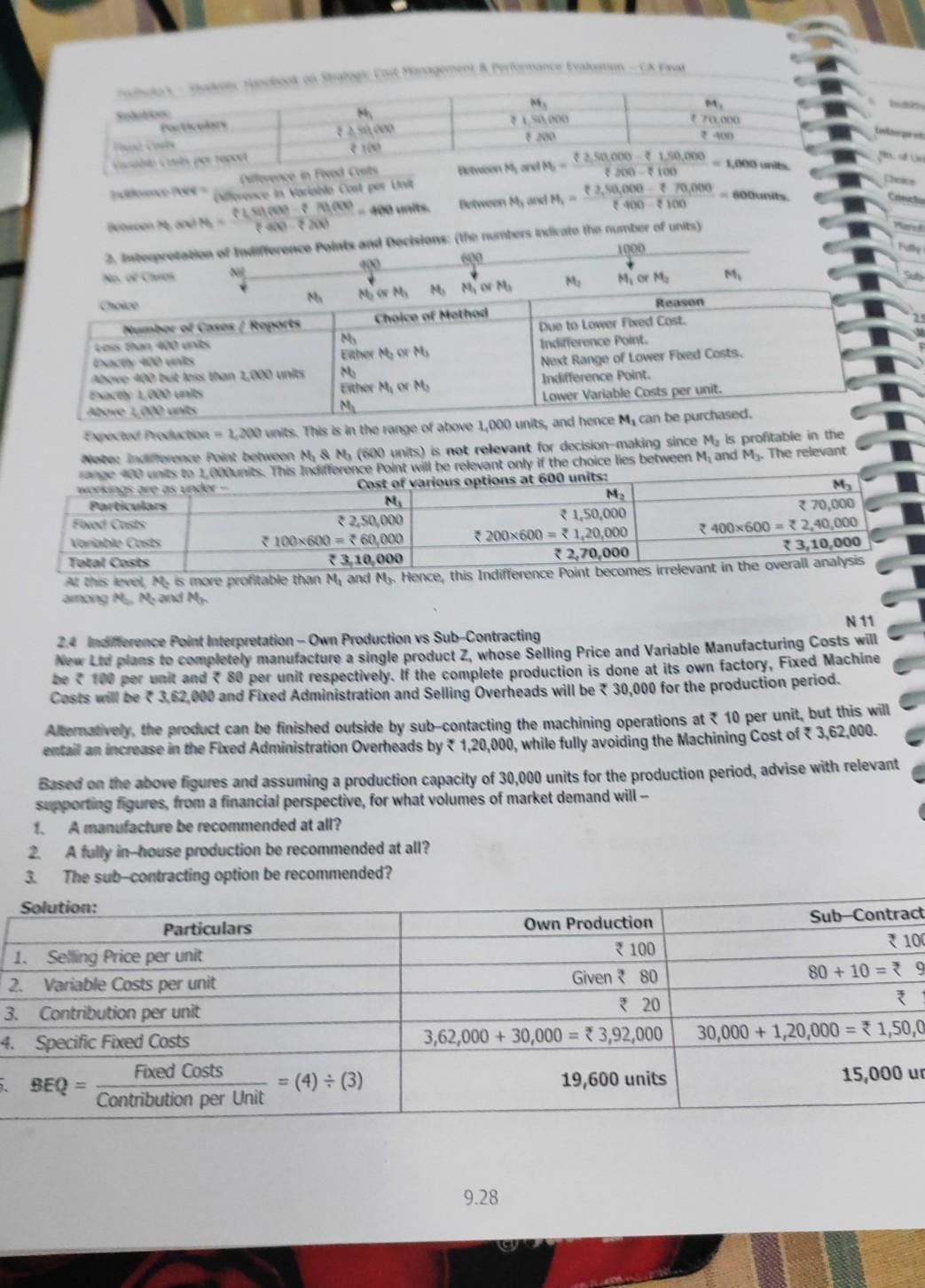

000 wi MAR 1000 AN MM -2.000 150.000 100 100 2.50,000 70.000 ws In MM 100 100 of difference Hits and Decisions the numbers to the number of units) 600 M MOM MMM M M M, OM Reason Choice of Method CarRents NI Due to Lower Fixed Cost Esther MOM Indifference Point M Next Range of Lower Fixed Costs. NO LA Esther MM Indifference Point M Lower Variable Costs per unit. = 2,200 units. This is in the range of above 1,000 units, and hence M, can be purchased. Me behen M & M (800 units) is not relevant for decision-making since Me is profitable in the 2.000 This Indifference point will be relevant only if the choice lies between M, and M. The relevant Was Cast of various options at 600 units: Parcours N M M 22.50,000 31,50,000 370.000 100x600 360,000 200x600 = 1,20,000 400x600 = 2,40,000 3.10.000 32,70,000 13,10,000 svet Me 5 more profitable than M, and M. Hence, this indifference point becomes irrelevant in the overall analysis among Mand N 11 24 horence Point Interpretation - Own Production vs Sub-Contracting New Lid plans to completely manufacture a single product Zwhose Selling Price and Variable Manufacturing Costs will 100 per unit and + 80 per unit respectively. If the complete production is done at its own factory, Fixed Machine Casts will de 3.62,000 and Fixed Administration and Selling Overheads will be * 30,000 for the production period. Alternatively, the product can be finished outside by sub-contacting the machining operations at * 10 per unit, but this will entail an increase in the Fixed Administration Overheads by 1,20,000, while fully avoiding the Machining Cost of 3,62,000. Based on the above figures and assuming a production capacity of 30,000 units for the production period, advise with relevant supporting figures from a financial perspective, for what volumes of market demand will - 1. A manufacture be recommended at all? 2 A fully in-house production be recommended at all? 3 The sub-contracting option be recommended? Solution: Particulars Own Production Sub-Contract 1. Selling Price per unit 3 100 100 2. Variable Costs per unit Given 80 80 + 10 = 9 3. Contribution per unit 20 4. Specific Fixed Costs 3,62,000 + 30,000 = 3,92,000 30,000 + 1,20,000 = 1,50,0 Fixed Costs 5. SEQ (4) = (3) 19,600 units 15,000 uc Contribution per Unit 9.28 Perescons for change in Cost during the product uite che here from the end of maturity stage) to +225 (in dedige) my be due to 0) un forts as a product reads the mury stage count, forts for Stock arance, Required: Case Study: Life Cycle Costing - Basics Meera News Reporter and Feature water ter an economic daily. Her ansignment is to develop a feature article on "Prektora general budget for travel to us to research into the Company's history, operations, and marnet analysis for the Firm she selects for the article Meena has asked you to recommend industries and Firms that would be good candidates for the article. What would you advice? Explain your recommendations. 2 Her Colleague was informally chatting with Meena and observed that lower prices would be charged when a product is out of demand or when a newer product version is launched by a Company, in order to get rid of old stocks. Is this observation correct? Which stage of Product Life Cycle is being dealt with in this case? 3 Outline the importance of Product Life Cycle Costing Issue 1: Bamples of Industries which can be considered for Product Life Cyde (PLC) analysis are - Automobile Companies, eg. Maruti, Honda, Toyota, etc with Car Model PLC of 5-6 years. Mobile / Cell Phone Service Providers, eg. Reliance, Tata, Airtel, etc with Scheme PLC of 1-2 years. Pharmaceutical Companies with Product PLC of 5-6 years. Issue 2: The situation referred to here is the "Decline" stage of Product Life Cycle, wherein lower prices may be charged to reduce the old sacks on hand. There is a Price Cutting Strategy to sell-off existing stocks in this stage. 1. Issue 3: Refer Para 8.6 for importance of Product Life Cycle Costing. N 18 (New) Case Study: Identification of Features, Strategies in Life Cycle JK Lid is following Life Cycle Costing. Its four products PSP3, P2, and P. are in the Market respectively in Introduction, Growth, Maturity and Decline stages (phases). The Management wants to analyse the marketing challenges faced by the products to take strategical measures to stabilize the products in the market. For this purpose, the Board directed the Secretary to get a product-use report from the Marketing Chief of each product. The Chiefs were asked to give one characteristic possessed by the product because of which the product is being classified in the respective stage, and two strategical measures to be taken to overcome the market challenges faced at the stage (phase). The Secretary received the report from all the Chiefs and handed them over to the Computer Operator to get it printed in a tabulated form. But the Operator, without understanding the significance of the products, phases, characteristics and strategies, mixed all the twelve items ((1+2}x4] and got it printed as a list as given below. Over capacity in the Industry. 2 The Company can continue to offer the product to our Loyal Customers at a Reduced Price. Few Competitor Produce basic version of our Product Product features may be improved or enhanced to differentiate our product from that of the competitors. 5. Attracting Customers by raising awareness about our product through promotion activities. 6. High volume of business and increase in competition 7. Use the present product as replacement product for launching another new product successfully in the Market. 3. Value-based Pricing Strategies may be considered. Profits start declining and at times become negative. 10. Maintain Control over product quality to assure Customer Satisfaction. 11. Strengthening or expanding channel and Supply Chain Relationships. 12. Prices may have to be reduced to attract the price-sensitive Customers. 3. 4. 9. 8.12 Setorsk on Store Cont Management, as Performanse metten than simply the lowestros Rear Cou Rection Tanger Cormanent control system to remman and to entity market opportunities that cand interesseret Trinevation! It reforces top to bottom commitment to prwi inwon, disme wenye Market Driven Management Il Pelps to create a company's competitive future with market driven man HA 7.1. . to be resolved for designing and manufacturing products that meet the price rangired for market succes Other Advantages of Target Costing Minimise or inate Non Value Added Activities Enhanced Partnership with suppliers Effective Planning and Usage of Resources Integration of Manufacturing and Sales Strategies Customer (or) Market-driven Approach Wholistic Approach from Design in to Post Sales Service Proactive Approach to Cont Management Top to bottom Organisational Commitment . . 7.1.8 Disadvantages of Target Costing 1. Time: The development process has to be lengthened for a long time, since the Design Team may require a number of design iterations, before it can devise a sufficiently low cost product that meets the Target Cost and Margin criteria. 2. Responsibility: Strong interpersonal and negotiation skills are required on the part of the Project Manager, to avoid behavioural problems if cost reduction targets are not equitable shared. For example, the industrial Engineering Staff will not be happy if they are required to completely after the production layout in order to generate cost savings, while the Purchase Staff are not required to make any cost reductions through Supplier negotiations, 3. Co-ordination: Having representatives from a number of departments on the Design Team makes the process of decision making difficult. Quality Issues: Excessive focus on Cost Reduction, leading to use of cheaper components and materials, may lead to reduction in quality of the product. 5. Cost Data: Il proper Cost Data is not used for Target Costing, then the Cost-Benefit Analysis made based on such data may not be converted into actual performance. These problems can be set right by a good Team Leader, who must have an exceptional knowledge of the design process, good interpersonal skills, and a commitment to stay within time and cost budgets for a design project. 4. 7.1.9 Role of Cost Accountant in Target Costing The role of a Cost Accountant in a Target Costing Team consists of the following activities - 1. Cost Estimation: To provide other members of the design team a running series of cost estimates based on initial designs sketch, activity-based costing reviews of production processes, and "best guess" costing information from suppliers based on estimated production volumes. 2. Permissible Cost Ranges: To provide estimates within a high-low range cost, since preliminary data may be vague. But, the estimated cost range should be modified as more information becomes available. 3. Capital Budgeting Analysis: To cater to capital budgeting requests generated by the Design Team, based on types of equipment needed for the anticipated product design, product revenues and costs, rates of return, etc. and to answer questions regarding uncertainties and risk analysis. 4. Cost Principles Explanation: To work with the Design Team to help it understand the nature of various costs (such as cost allocations based on an Activity-Based Costing system), as well as the cost-benefit trade-offs of using different design or cost operations in the new product. 5. Review of Cost Reduction Targets: To track the gap between the Current Cost and the Target Cost (i.e. the Desig Team's goal), providing an itemization of where cost savings have already been achieved, and where there has been a sufficient degree of progress. 6. Final Review and Feedback: To compare a product's Actual Cost to the Target Cost after the design is complex and for as long as the Company sells the product. This is necessary since Management must know immediately if are increasing beyond budgeted levels and why these increases are occurring. Note: Since the role of the Cost Accountant in a Target Costing Team is very significant, he should have the foll- qualifications - (only illustrative and not exhaustive) 7.4 la suhe - Steve Maddeck on Strategie Cost Management & Performance Evaluation cam Principle Description Es distingush those who do the work from those who monitor and make de about the work based on the assumption that there who do the world not the (a) Decision Point where the work is herformed, but bull controls time, inchination, knowledge, or responsibility for monitoring and controlling what they However, Information Technology Tools can be used to capture and store ders, and Expert Systems to supply knowledge, to enable people to make their own decinson Thus, BPR seeks to changes the role of a Manager from Controller and Supervisor to Supporter and Facilitator. This also eliminates the Middle Managers who had been summarizing and reporting Information to Top Mariagement, . 5.4.3 Process Innovation vs BPR BPR Process Innovation (PI) BPR focusses on amending existing processes. Pl seeks to implement new processes into an Entity. BPR is streamlining processes that are already in place, PI is more radical than BPR, since it seeks to change the overall structure of an Entity. Questions for Revision 1 Outline the meaning of "Lean System. List its features. 2 What are the seven types of "Waste" in the context of a "Lean System"? 3 List a few principles objectives of "Lean System". 4. What are the techniques through which "Lean System" is implemented? 5. Wnite short notes on the numerical concept of Six Sigma 6 Explain how Six Sigma Concept is applied in Lean System. 7 What are the features of Six Sigma? 8 List a few advantages of Six Sigma Concept. 9. Explain the methodologies for implementing Six Sigma Concept. 10. Differentiate between DMAIC and DMADV in the context of Six Sigma implementation. 11. Explain how DMAIC philosophy can be implemented in the Banking Sector. 12. Briefly explain some Quality Management Tools used in Six Sigma Concept. 13. What are the central themes of Six Sigma Philosophy? 14. Six Sigma has its limitations. Explain a few of these. 15. What do you mean by Kaizen Costing? 16. What is 5S Methodology in Lean System Implementation? 17. Write short notes on Total Productive Maintenance (TPM) Methodology. 18. Explain the concept of 8-Pillars of TPM Methodology. 19. Explain the concept of OEE in TPM Methodology 20. Write short notes on Cellular Manufacturing/One Piece Flow Production System. 21. Explain the concept of Process Innovation. 22. Write short notes on the concept of Business Process Re-Engineering (BPR). 23. In what ways Process Innovation is different from BPR? Case Study: Kaizen Costing M India Ltd (MIL) is an Automobile Manufacturer in India and a Subsidiary of Japanese Automobile and Motorcy manufacturer Leon. MIL manufactures and sells a complete range of cars from the entry level to the hatchback to sedans a has a present market share of 22% of the Indian Passenger Car markets. MIL uses a Standard Costing System to set budgets, Budgets are semi-annually by the Finance Department after the approval of MIL's Board of Directors. The Fina Department prepares Variance Reports each month for review in the Board Meeting, where actual performance is comp with budgets. The Group CEO of Leon is of the opinion that Kaizen Costing method should be implemented as a syste planning and control in MIL. You are required to recommend key changes vital to MIL's Planning and Control Syster support the adoption of Kaizen Costing Concepts. 5.12Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Ressourceneffizientes Wirtschaften

Authors: Heinz Karl Prammer

2nd Edition

3658046082, 9783658046088