Answered step by step

Verified Expert Solution

Question

1 Approved Answer

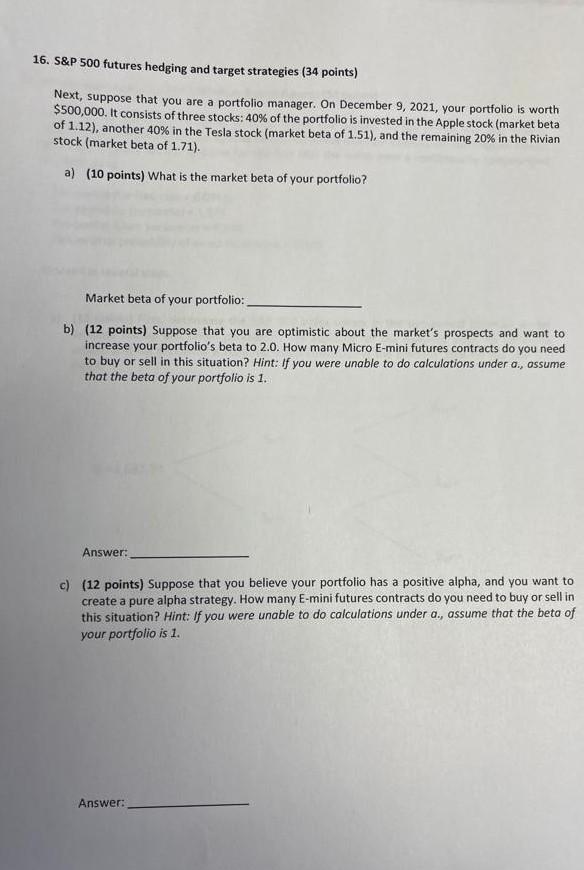

Old MathJax webview please solve it complete Please solve it in one hour please 16. S&P 500 futures hedging and target strategies (34 points) Next,

Old MathJax webview

please solve it complete

Please solve it in one hour please

16. S&P 500 futures hedging and target strategies (34 points) Next, suppose that you are a portfolio manager. On December 9, 2021, your portfolio is worth $500,000. It consists of three stocks: 40% of the portfolio is invested in the Apple stock (market beta of 1.12), another 40% in the Tesla stock (market beta of 1.51), and the remaining 20% in the Rivian stock (market beta of 1.71). a) (10 points) What is the market beta of your portfolio? Market beta of your portfolio: b) (12 points) Suppose that you are optimistic about the market's prospects and want to increase your portfolio's beta to 2.0. How many Micro E-mini futures contracts do you need to buy or sell in this situation? Hint: If you were unable to do calculations under a., assume that the beta of your portfolio is 1. Answer: c) (12 points) Suppose that you believe your portfolio has a positive alpha, and you want to create a pure alpha strategy. How many E-mini futures contracts do you need to buy or sell in this situation? Hint: if you were unable to do calculations under a., assume that the beta of your portfolio is 1Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management Of Health Care Organizations

Authors: William N. Zelman, Michael J. McCue, Noah D. Glick, Marci S. Thomas

5th Edition

1119553849, 9781119553847