Answered step by step

Verified Expert Solution

Question

1 Approved Answer

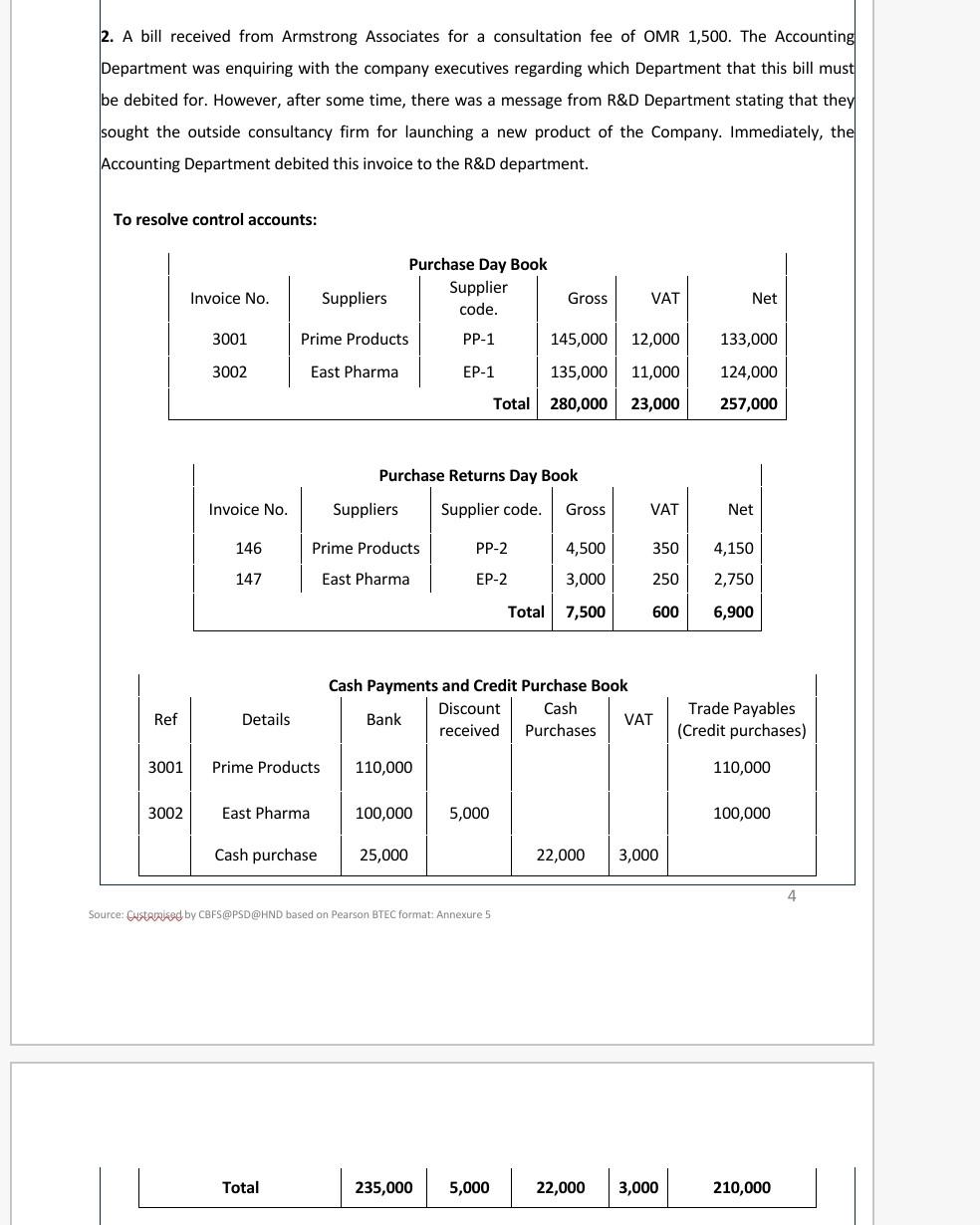

Old MathJax webview Please solve question P6 please solve question P6 P6 Explain the process taken to reconcile control accounts and clear suspense accounts using

Old MathJax webview

Please solve question P6

please solve question P6

P6 Explain the process taken to reconcile control accounts and clear suspense accounts using given account examples.

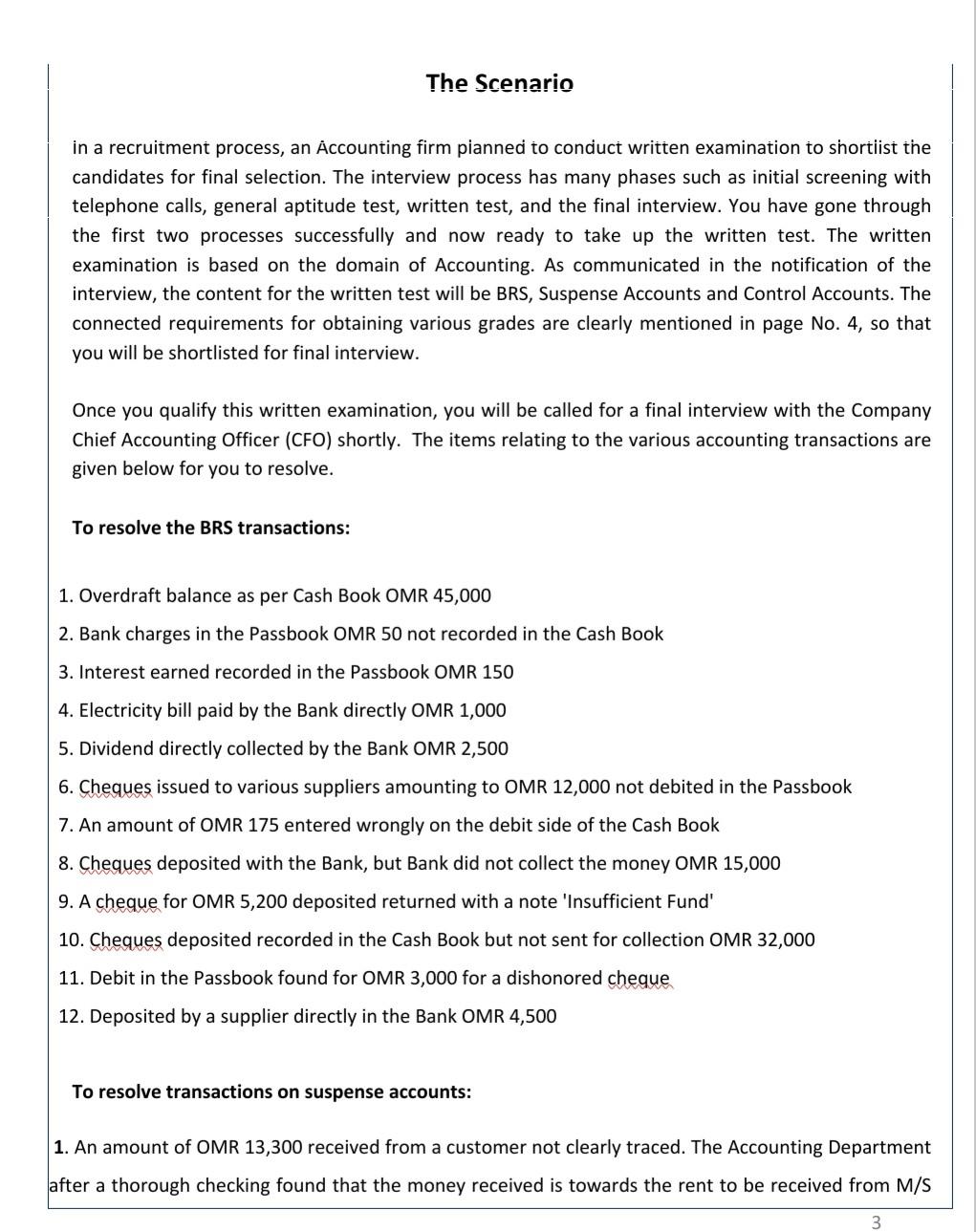

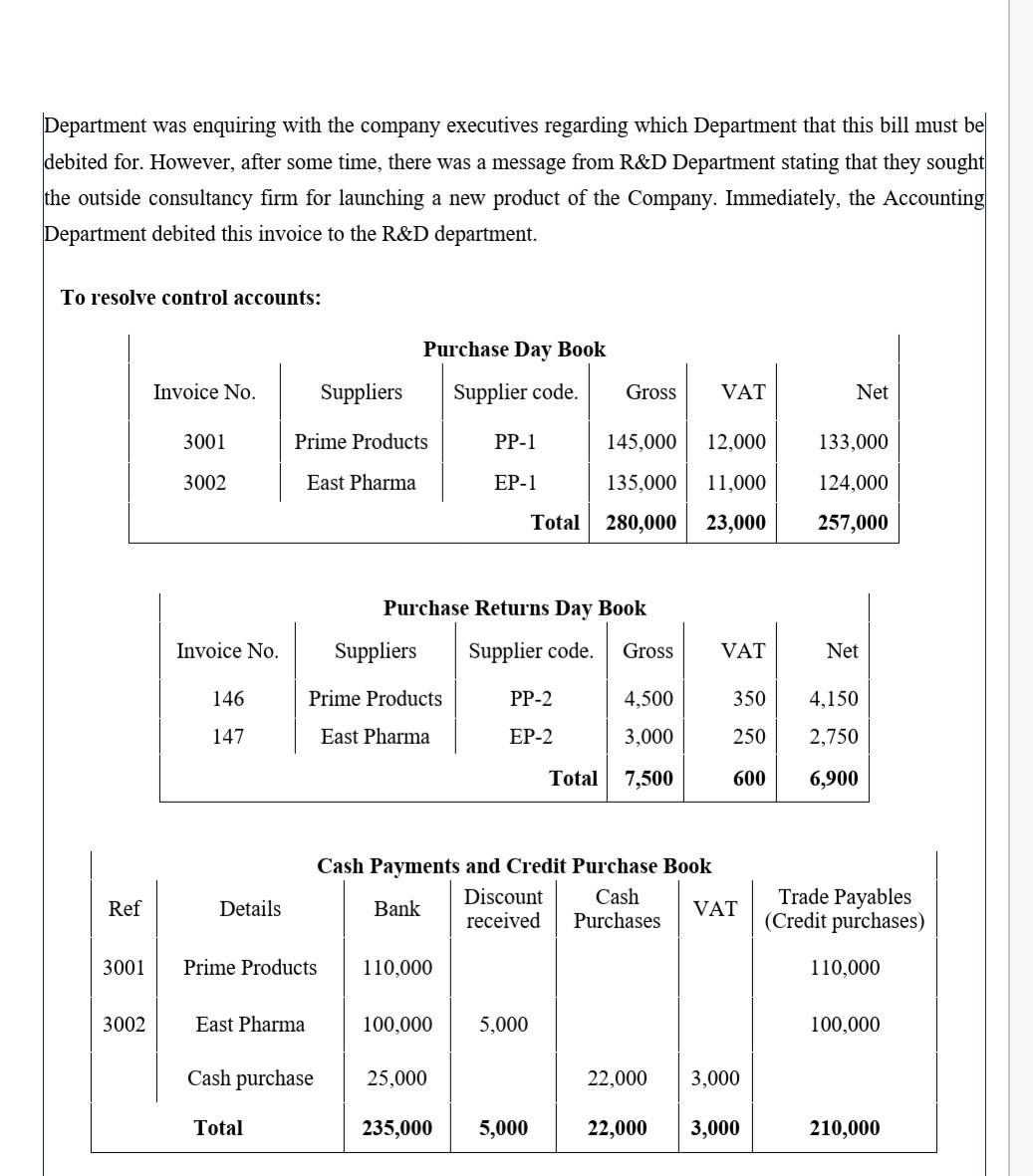

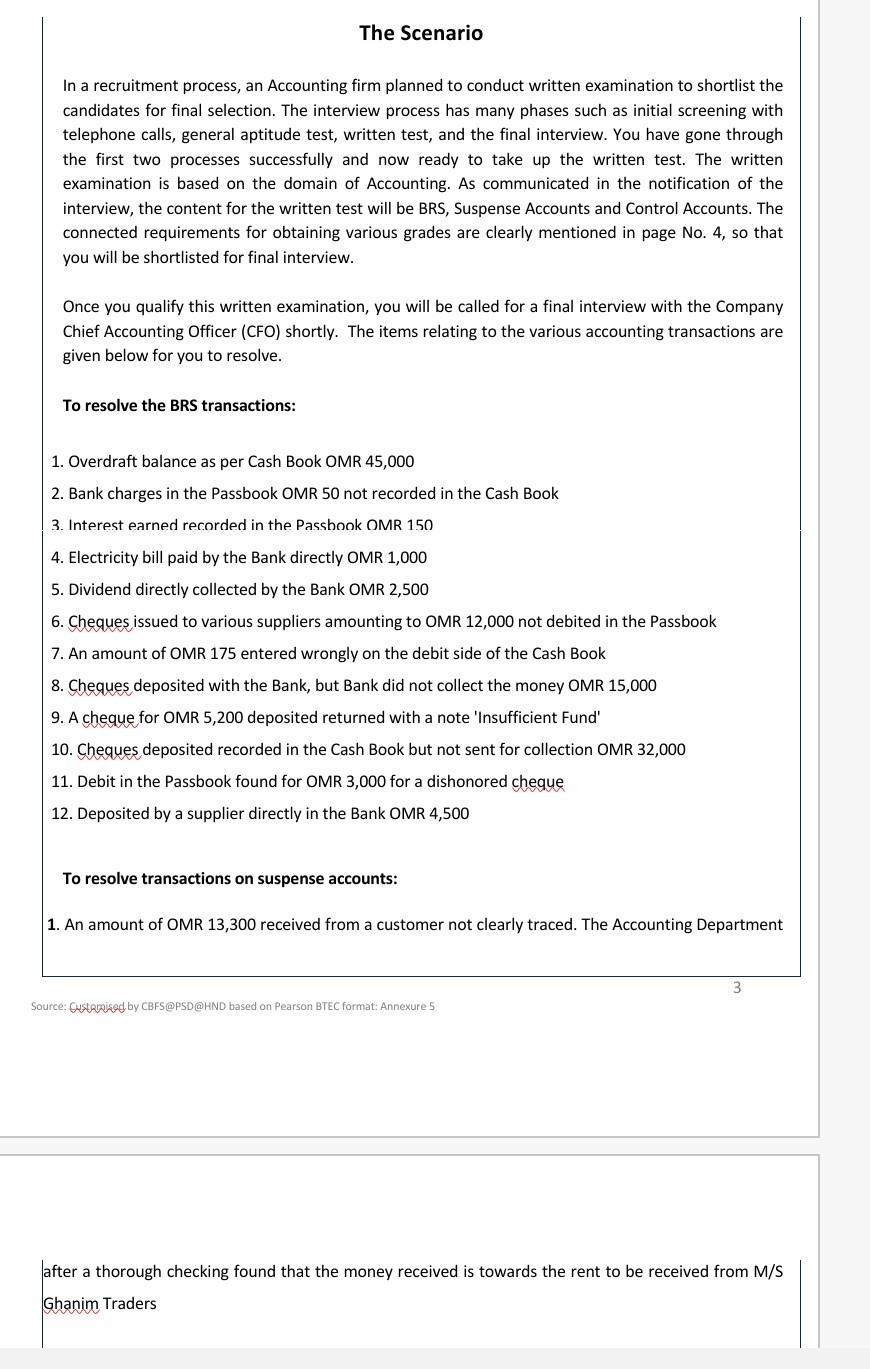

The Scenario in a recruitment process, an Accounting firm pianned to conduct written examination to shortlist the candidates for final selection. The interview process has many phases such as initial screening with telephone calls, general aptitude test, written test, and the final interview. You have gone through the first two processes successfully and now ready to take up the written test. The written examination is based on the domain of Accounting. As communicated in the notification of the interview, the content for the written test will be BRS, Suspense Accounts and Control Accounts. The connected requirements for obtaining various grades are clearly mentioned in page No. 4, so that you will be shortlisted for final interview. Once you qualify this written examination, you will be called for a final interview with the Company Chief Accounting Officer (CFO) shortly. The items relating to the various accounting transactions are given below for you to resolve. To resolve the BRS transactions: 1. Overdraft balance as per Cash Book OMR 45,000 2. Bank charges in the Passbook OMR 50 not recorded in the Cash Book 3. Interest earned recorded in the Passbook OMR 150 4. Electricity bill paid by the Bank directly OMR 1,000 5. Dividend directly collected by the Bank OMR 2,500 6. Cheques issued to various suppliers amounting to OMR 12,000 not debited in the Passbook 7. An amount of OMR 175 entered wrongly on the debit side of the Cash Book 8. Cheques deposited with the Bank, but Bank did not collect the money OMR 15,000 9. A cheque for OMR 5,200 deposited returned with a note 'Insufficient Fund' 10. Cheques deposited recorded in the Cash Book but not sent for collection OMR 32,000 11. Debit in the Passbook found for OMR 3,000 for a dishonored cheque 12. Deposited by a supplier directly in the Bank OMR 4,500 To resolve transactions on suspense accounts: 1. An amount of OMR 13,300 received from a customer not clearly traced. The Accounting Department after a thorough checking found that the money received is towards the rent to be received from M/S 3 Department was enquiring with the company executives regarding which Department that this bill must be debited for. However, after some time, there was a message from R&D Department stating that they sought the outside consultancy firm for launching a new product of the Company. Immediately, Accounting Department debited this invoice to the R&D department. the To resolve control accounts: Purchase Day Book Invoice No. Suppliers Supplier code. Gross VAT Net 3001 Prime Products PP-1 145,000 12,000 133,000 3002 East Pharma EP-1 135,000 11,000 124,000 Total 280,000 23,000 257,000 Purchase Returns Day Book Invoice No. Suppliers Supplier code. Gross VAT Net 146 Prime Products PP-2 4,500 350 4,150 147 East Pharma EP-2 3,000 250 2,750 Total 7,500 600 6,900 Cash Payments and Credit Purchase Book Discount Cash Bank VAT received Purchases Ref Details Trade Payables (Credit purchases) 3001 Prime Products 110,000 110,000 3002 East Pharma 100,000 5,000 100,000 Cash purchase 25,000 22,000 3,000 Total 235,000 5,000 22,000 3,000 210,000 P6 Explain the process taken to reconcile control accounts and clear suspense accounts using given account examples. The Scenario In a recruitment process, an Accounting firm planned to conduct written examination to shortlist the candidates for final selection. The interview process has many phases such as initial screening with telephone calls, general aptitude test, written test, and the final interview. You have gone through the first two processes successfully and now ready to take up the written test. The written examination is based on the domain of Accounting. As communicated in the notification of the interview, the content for the written test will be BRS, Suspense Accounts and Control Accounts. The connected requirements for obtaining various grades are clearly mentioned in page No. 4, so that you will be shortlisted for final interview. Once you qualify this written examination, you will be called for a final interview with the Company Chief Accounting Officer (CFO) shortly. The items relating to the various accounting transactions are given below for you to resolve. To resolve the BRS transactions: 1. Overdraft balance per Cash Book OMR 45,000 2. Bank charges in the Passbook OMR 50 not recorded in the Cash Book 3. Interest earned recorded in the Passbook OMR 150 4. Electricity bill paid by the Bank directly OMR 1,000 5. Dividend directly collected by the Bank OMR 2,500 6. Cheques issued to various suppliers amounting to OMR 12,000 not debited in the Passbook 7. An amount of OMR 175 entered wrongly on the debit side of the Cash Book 8. Cheques deposited with the Bank, but Bank did not collect the money OMR 15,000 9. A cheque for OMR 5,200 deposited returned with a note 'Insufficient Fund' 10. Cheques deposited recorded in the Cash Book but not sent for collection OMR 32,000 11. Debit in the Passbook found for OMR 3,000 for a dishonored cheque 12. Deposited by a supplier directly in the Bank OMR 4,500 To resolve transactions on suspense accounts: 1. An amount of OMR 13,300 received from a customer not clearly traced. The Accounting Department 3 Source: Customised by CBFS@PSD@HND based on Pearson BTEC format: Annexure 5 after a thorough checking found that the money received is towards the rent to be received from M/S Ghanim Traders 2. A bill received from Armstrong Associates for a consultation fee of OMR 1,500. The Accounting Department was enquiring with the company executives regarding which Department that this bill must be debited for. However, after some time, there was a message from R&D Department stating that they sought the outside consultancy firm for launching a new product of the Company. Immediately, the Accounting Department debited this invoice to the R&D department. To resolve control accounts: Purchase Day Book Supplier code. Invoice No. Suppliers Gross VAT Net 3001 Prime Products PP-1 145,000 12,000 133,000 3002 East Pharma EP-1 135,000 11,000 124,000 Total 280,000 23,000 257,000 Purchase Returns Day Book Invoice No. Suppliers Supplier code. Gross VAT Net 146 Prime Products PP-2 4,500 350 4,150 147 East Pharma EP-2 3,000 250 2,750 Total 7,500 600 6,900 Cash Payments and Credit Purchase Book Discount Cash Bank VAT received Purchases Ref Details Trade Payables (Credit purchases) 3001 Prime Products 110,000 110,000 3002 East Pharma 100,000 5,000 100,000 Cash purchase 25,000 22,000 3,000 4 Source: Customised by CBFS@PSD@HND based on Pearson BTEC format: Annexure 5 Total 235,000 5,000 22,000 3,000 210,000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

I Would Rather Eat A Cactus Than Audit A Project A Beginners Guide To Project Audit And Assurance

Authors: Lesley Elder-Aznar

1st Edition

B0B4HKGN3S, 979-8838344298