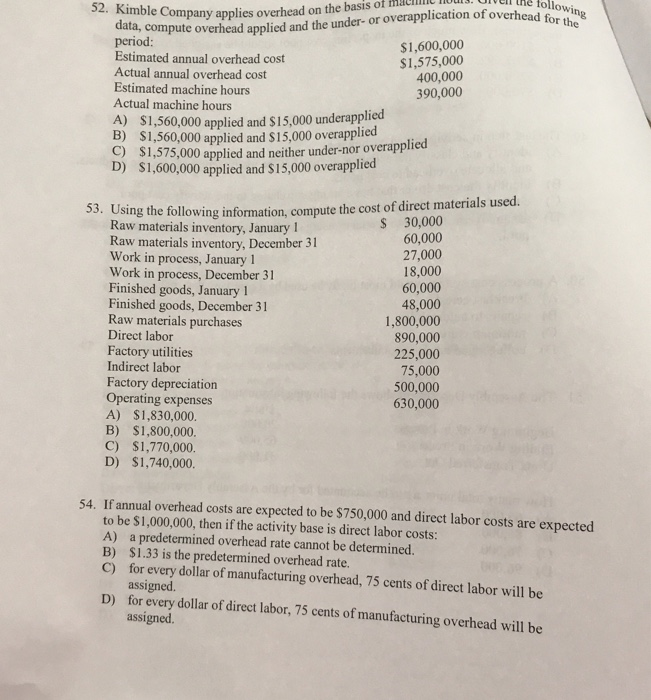

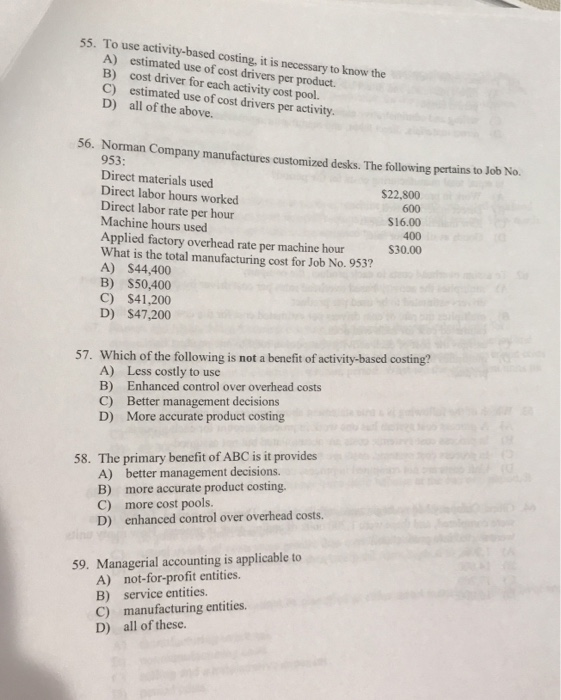

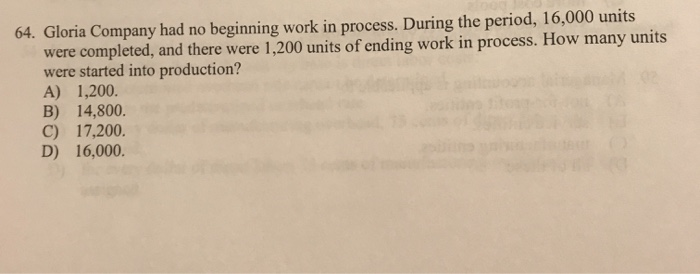

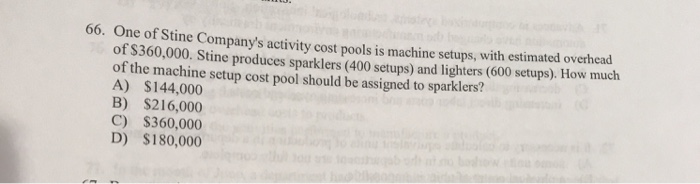

ollowing 52. Kimble Company app data, compute overhead applier erhead for the . Civell the toll Nimble Company applies overhead on the basis of much compute overhead applied and the under- or overapplication of overhead period: Estimated annual overhead cost $1,600,000 Actual annual overhead cost $1,575,000 400,000 Estimated machine hours 390,000 Actual machine hours A) $1,560,000 applied and $15,000 underapplied B) $1,560,000 applied and $15,000 overapplied C) $1,575,000 applied and neither under-nor overapphe D) $1,600,000 applied and $15,000 overapplied Tollowing information, compute the cost of direct materials used. Raw materials inventory, January 1 $ 30,000 Raw materials inventory, December 31 60,000 Work in process, January 1 27,000 Work in process, December 31 18,000 Finished goods, January 1 60,000 Finished goods, December 31 48,000 Raw materials purchases 1,800,000 Direct labor 890,000 Factory utilities 225,000 Indirect labor 75,000 Factory depreciation 500,000 Operating expenses 630,000 A) $1,830,000. B) $1,800,000 C) $1,770,000 D) $1,740,000 54. If annual overhead costs are expected to be $750,000 and direct labor costs are expected to be $1,000,000, then if the activity base is direct labor costs: A) a predetermined overhead rate cannot be determined. B) $1.33 is the predetermined overhead rate. C) for every dollar of manufacturing overhead, 75 cents of direct labor will be assigned D) for every dollar of direct labor, 75 cents of manufacturing overhead will be assigned 55. To use activity-based costing, it is necessary to know the A) estimated use of cost drivers per product. cost driver for each activity cost pool. C) estimated use of cost drivers per activity. D) all of the above. B) 56. Norman Company manufactures customized desks. The following pertains to Job No. 953: Direct materials used Direct labor hours worked $22,800 600 Direct labor rate per hour $16.00 Machine hours used 400 Applied factory overhead rate per machine hour S30.00 What is the total manufacturing cost for Job No. 953? A) S44,400 B) S50,400 C) $41,200 D) $47,200 57. Which of the following is not a benefit of activity-based costing? A) Less costly to use B) Enhanced control over overhead costs C) Better management decisions D) More accurate product costing 58. The primary benefit of ABC is it provides A) better management decisions. B) more accurate product costing. C) more cost pools. D) enhanced control over overhead costs. 59. Managerial accounting is applicable to A) not-for-profit entities. B) service entities. C) manufacturing entities. D) all of these. 64. Gloria Company had no beginning work in process. During the period, 16,000 units were completed, and there were 1,200 units of ending work in process. How many units were started into production? A) 1,200. B) 14,800 C) 17,200 D) 16,000 66. One of Stine Company's activity cost pools is machine setups, with estimated overhead of $360,000. Stine produces sparklers (400 setups) and lighters (600 setups). How much of the machine setup cost pool should be assigned to sparklers? A) $144,000 B) $216,000 C) $360,000 D) $180,000 75. A process with 1,600 units of beginning work in process, completed and transferred out 25,000 units during a period. There were 10,000 units in the ending work in process that were 50% complete as to conversion costs. Materials are added 80% at the beginning of the process and 20% when the units are 90% complete. How much is equivalent units of production for the period for material costs? A) 33.000 equivalent units. B) 35,000 equivalent units. C) 27,000 equivalent units. D) 29,000 equivalent units. Produccess and 20te as lo con there were work in proce A) 33.0 for the perihen the units, costs. Materials in the endsted and transfe 35,000 urvalent unit material cost complete. Te added 809 Work in process 76. A well-designed activity-based costing system starts with A) computing the activity-based overhead rate. B) identifying the activity-cost pools. C) assigning overhead costs to products. D) analyzing the activities performed to manufacture a product. 77. In the month of June, a department had 20,000 units in beginning work in process that were 70% complete. During June, 90,000 units were transferred into production from another department. At the end of June there were 10,000 units in ending work in process that were 40% complete. Materials are added at the beginning of the process, while conversion costs are incurred uniformly throughout the process. The equivalent units of production for materials for June were A) 114,000 equivalent units. B) 90,000 equivalent units. C) 110,000 equivalent units. D) 100,000 equivalent units. 78. Cinder Company had the following department information for the month: Total materials costs $ 60,000 Equivalent units of materials 10,000 Total conversion costs $90,000 Equivalent units of conversion costs 20,000 How much is the total manufacturing cost per unit? A) $5.00 B) $10.50 C) $4.50. D) $6.00