Answered step by step

Verified Expert Solution

Question

1 Approved Answer

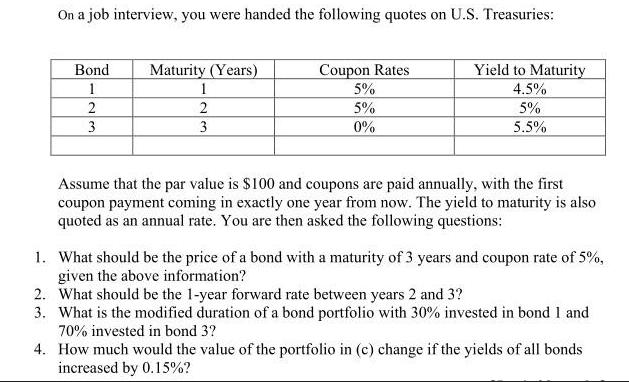

On a job interview, you were handed the following quotes on U.S. Treasuries: Bond 1 2 3 Maturity (Years) 1 2 3 Coupon Rates

On a job interview, you were handed the following quotes on U.S. Treasuries: Bond 1 2 3 Maturity (Years) 1 2 3 Coupon Rates 5% 5% 0% Yield to Maturity 4.5% 5% 5.5% Assume that the par value is $100 and coupons are paid annually, with the first coupon payment coming in exactly one year from now. The yield to maturity is also quoted as an annual rate. You are then asked the following questions: 1. What should be the price of a bond with a maturity of 3 years and coupon rate of 5%, given the above information? 2. What should be the 1-year forward rate between years 2 and 3? 3. What is the modified duration of a bond portfolio with 30% invested in bond 1 and 70% invested in bond 3? 4. How much would the value of the portfolio in (c) change if the yields of all bonds increased by 0.15%?

Step by Step Solution

★★★★★

3.51 Rating (161 Votes )

There are 3 Steps involved in it

Step: 1

Step 11 1 The price of a bond with a maturity of 3 years and coupon rate of 5 would be calc...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516