Question

On April 4th at 3:00 pm, 2019, Jason Smith, President of Clean Air Inc, called to order a meeting of the financial personnel. The purpose

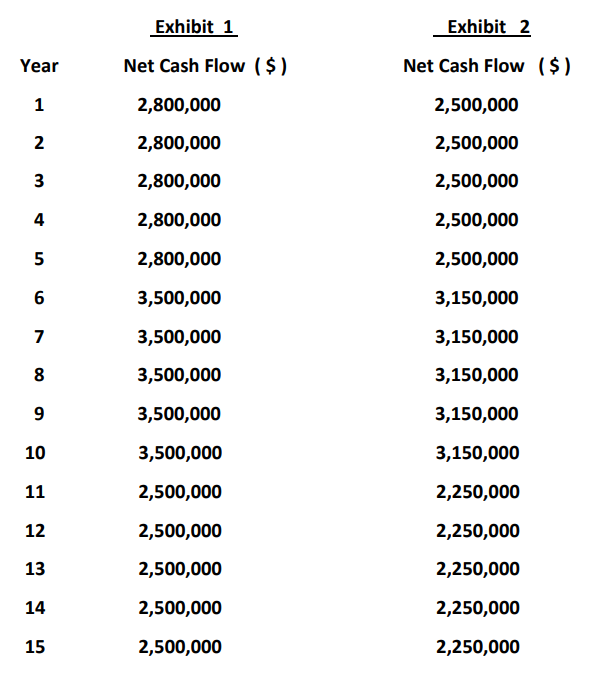

On April 4th at 3:00 pm, 2019, Jason Smith, President of Clean Air Inc, called to order a meeting of the financial personnel. The purpose of the meeting was to make a capital budgeting decision with respect to the potential introduction and production of a new product, a liquid detergent called Blast. In the face of increased competition and technological innovation, Clean Air spent large amounts of time and money over the past 4 years researching and developing new, highly concentrated liquid laundry detergents. Clean Airs new detergent, Blast, would have many obvious advantages over the conventional powdered products as it is highly concentrated, in liquid form and can be packed in light, unbreakable plastic bottles. The meeting was attended by Jason Smith, the president, Jim Anderson, vicepresident of new products, Bob Johnson, the controller and his new assistant Steve Gasper. Smith called the meeting to order, gave a brief statement of its purpose and immediately gave the floor to Bob Johnson. Johnson opened with a presentation of the cost and cash flow analysis for the new product. Anderson proposed that initial cost for the project should include $ 1,000,000 for a test market conducted in the Toronto area. His argument is that; without spending the $ 1MM on test market, Clean Air would never have launched this new product! New specialized machinery/equipment and packing facilities for Blast production is estimated to cost $ 20MM. The whole investment belongs to a CCA class with a rate of 20%. It is expected that this facility will operate for 15 years , at the end of which its salvage value would be 15% of its original value. Anderson cautioned against taking the annual cash flows (as shown in Exhibit 1 ) at face value since portions of these cash flows actually are a result of sales that had been diverted from its existing products. For this reason, Anderson also provided annual cash flows that had been adjusted to include only those cash flows incremental to the company as a whole. ( Exhibit 2 ). 3 At this point, discussions opened up and came to a consensus that the opportunity costs of funds is 10%. Gasper then questioned the fact that no costs were included in the proposed cash budget for plant space which would be needed to produce the new product. Smith then replied that, at the present time, production of existing products would require 55% of total floor space and the additional full production of Blast would need another 10% of the total floor area. Bob Johnson then asked if there had been any consideration of increase working capital needed to operate this project. Anderson answered that there had been and that the Blast project would require $ 500,000 in additional working capital; however, since the money would not leave the firm and always be in liquid form it was not considered as outflow; and therefore not included in the calculation. Smith argued that this project should be charged something for its use of current excess plant space capacity. His reasoning was that if any outside firm tried to rent this space from Clean Air, this outside firm would be charged $ 150,000 as rent per year. Clean Air has a corporate tax rate of 40%. From this point on, discussions continued centering itself on the question as what to do about test market costs, working capacity, available floor space and lost contributions from existing products etc.

Question 1: If you were in Steve Gaspers place, would you argue for the cost of testing marketing to be included as cash outflow and why? If your argument is to be included, what would its PV be? Would you support the idea that the working capital tied up for the Blast project be included in the analysis, why or why what? If you argue that it should be included, what would its PV be?

Exhibit 2 Exhibit 1 Net Cash Flow ($) Year Net Cash Flow ($) 1 2,800,000 2,500,000 2 2 2,800,000 2,500,000 3 2,800,000 2,500,000 4 2,800,000 2,500,000 5 2,800,000 2,500,000 6 3,500,000 3,150,000 7 3,500,000 3,150,000 8 3,500,000 3,150,000 9 3,500,000 3,150,000 10 3,500,000 3,150,000 11 2,500,000 2,250,000 12 2,500,000 2,250,000 13 2,500,000 2,250,000 14 2,500,000 2,250,000 15 2,500,000 2,250,000 Exhibit 2 Exhibit 1 Net Cash Flow ($) Year Net Cash Flow ($) 1 2,800,000 2,500,000 2 2 2,800,000 2,500,000 3 2,800,000 2,500,000 4 2,800,000 2,500,000 5 2,800,000 2,500,000 6 3,500,000 3,150,000 7 3,500,000 3,150,000 8 3,500,000 3,150,000 9 3,500,000 3,150,000 10 3,500,000 3,150,000 11 2,500,000 2,250,000 12 2,500,000 2,250,000 13 2,500,000 2,250,000 14 2,500,000 2,250,000 15 2,500,000 2,250,000Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Top Actuel Fiscalité 2022-2023

Authors: Daniel Freiss,Brigitte Monnet

1st Edition

2017182176,2017879282