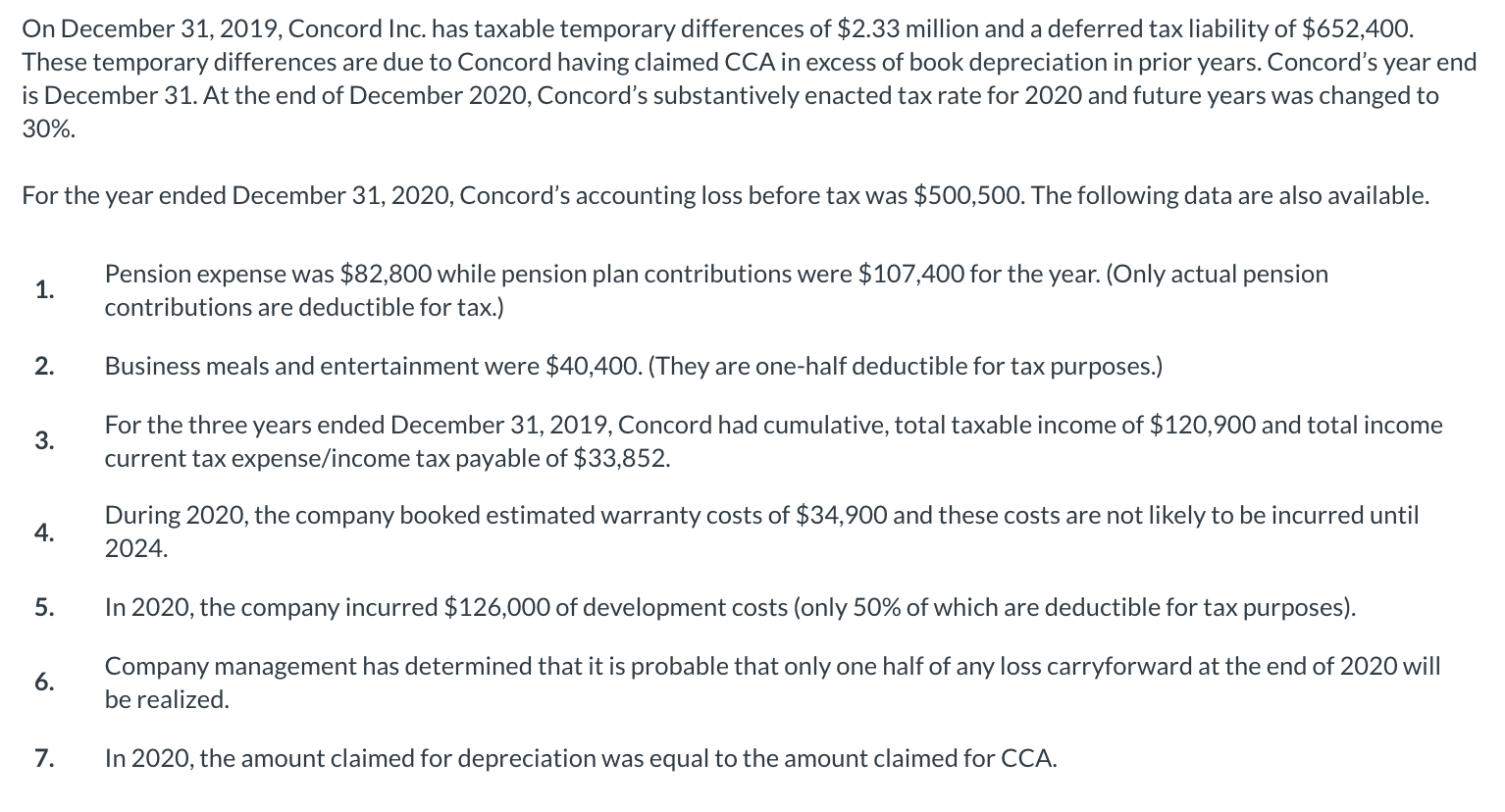

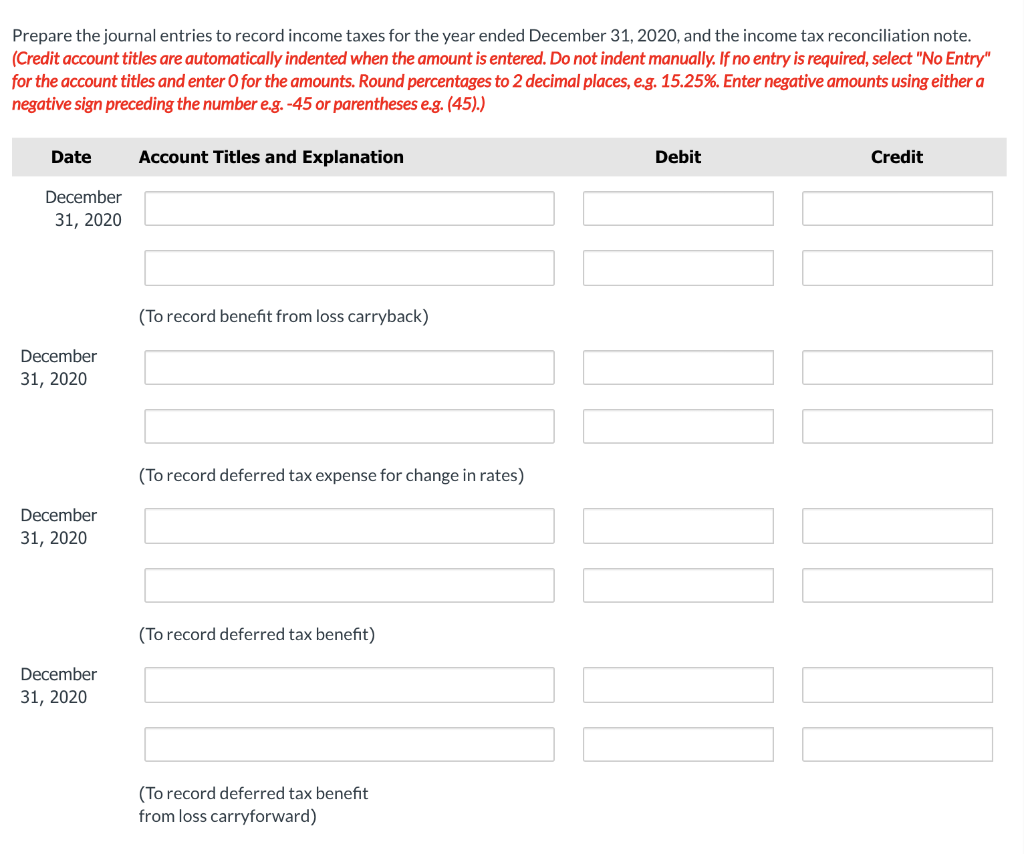

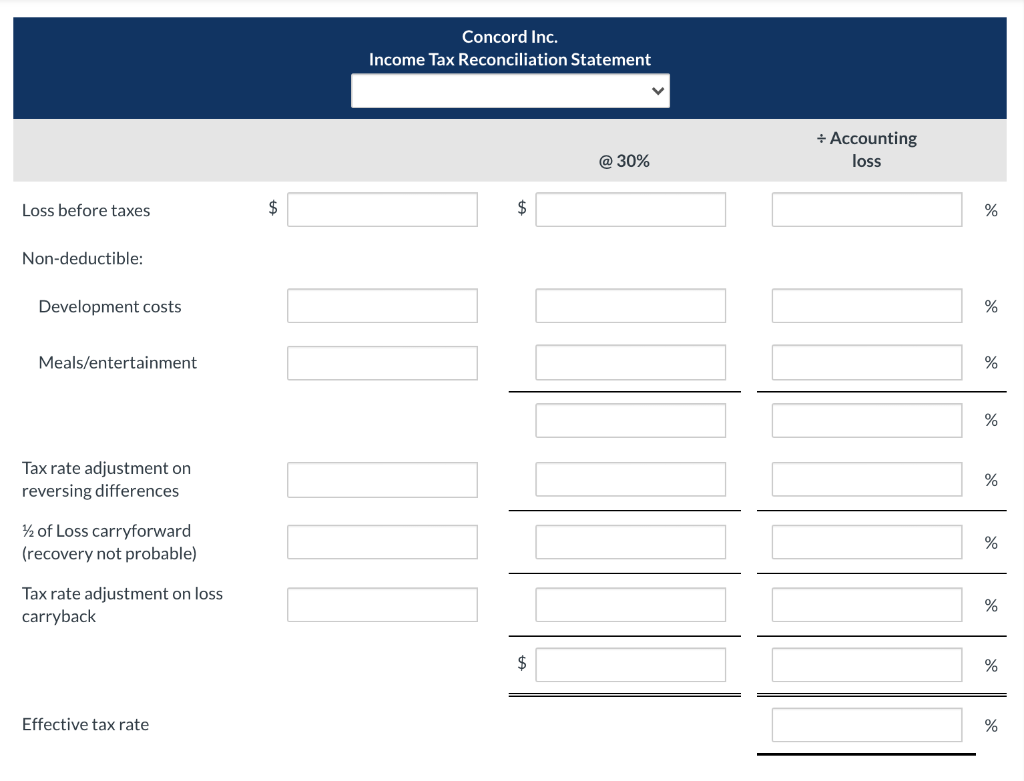

On December 31, 2019, Concord Inc. has taxable temporary differences of $2.33 million and a deferred tax liability of $652,400. These temporary differences are due to Concord having claimed CCA in excess of book depreciation in prior years. Concord's year end is December 31. At the end of December 2020, Concord's substantively enacted tax rate for 2020 and future years was changed to 30%. For the year ended December 31, 2020, Concord's accounting loss before tax was $500,500. The following data are also available. 1. Pension expense was $82,800 while pension plan contributions were $107,400 for the year. (Only actual pension contributions are deductible for tax.) 2. Business meals and entertainment were $40,400. (They are one-half deductible for tax purposes.) 3. For the three years ended December 31, 2019, Concord had cumulative, total taxable income of $120,900 and total income current tax expense/income tax payable of $33,852. 4. During 2020, the company booked estimated warranty costs of $34,900 and these costs are not likely to be incurred until 2024. 5. In 2020, the company incurred $126,000 of development costs (only 50% of which are deductible for tax purposes). 6. Company management has determined that it is probable that only one half of any loss carryforward at the end of 2020 will be realized. 7. In 2020, the amount claimed for depreciation was equal to the amount claimed for CCA. Prepare the journal entries to record income taxes for the year ended December 31, 2020, and the income tax reconciliation note. (Credit account titles are automatically indented when the amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter for the amounts. Round percentages to 2 decimal places, e.g. 15.25%. Enter negative amounts using either a negative sign preceding the number e.g. -45 or parentheses e.g. (45).) Date Account Titles and Explanation Debit Credit December 31, 2020 (To record benefit from loss carryback) December 31, 2020 (To record deferred tax expense for change in rates) December 31, 2020 (To record deferred tax benefit) December 31, 2020 (To record deferred tax benefit from loss carryforward) Concord Inc. Income Tax Reconciliation Statement V Accounting loss @ 30% Loss before taxes $ $ % Non-deductible: Development costs % Meals/entertainment % % Tax rate adjustment on reversing differences % 1 of Loss carryforward (recovery not probable) % Tax rate adjustment on loss carryback % $ % Effective tax rate % On December 31, 2019, Concord Inc. has taxable temporary differences of $2.33 million and a deferred tax liability of $652,400. These temporary differences are due to Concord having claimed CCA in excess of book depreciation in prior years. Concord's year end is December 31. At the end of December 2020, Concord's substantively enacted tax rate for 2020 and future years was changed to 30%. For the year ended December 31, 2020, Concord's accounting loss before tax was $500,500. The following data are also available. 1. Pension expense was $82,800 while pension plan contributions were $107,400 for the year. (Only actual pension contributions are deductible for tax.) 2. Business meals and entertainment were $40,400. (They are one-half deductible for tax purposes.) 3. For the three years ended December 31, 2019, Concord had cumulative, total taxable income of $120,900 and total income current tax expense/income tax payable of $33,852. 4. During 2020, the company booked estimated warranty costs of $34,900 and these costs are not likely to be incurred until 2024. 5. In 2020, the company incurred $126,000 of development costs (only 50% of which are deductible for tax purposes). 6. Company management has determined that it is probable that only one half of any loss carryforward at the end of 2020 will be realized. 7. In 2020, the amount claimed for depreciation was equal to the amount claimed for CCA. Prepare the journal entries to record income taxes for the year ended December 31, 2020, and the income tax reconciliation note. (Credit account titles are automatically indented when the amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter for the amounts. Round percentages to 2 decimal places, e.g. 15.25%. Enter negative amounts using either a negative sign preceding the number e.g. -45 or parentheses e.g. (45).) Date Account Titles and Explanation Debit Credit December 31, 2020 (To record benefit from loss carryback) December 31, 2020 (To record deferred tax expense for change in rates) December 31, 2020 (To record deferred tax benefit) December 31, 2020 (To record deferred tax benefit from loss carryforward) Concord Inc. Income Tax Reconciliation Statement V Accounting loss @ 30% Loss before taxes $ $ % Non-deductible: Development costs % Meals/entertainment % % Tax rate adjustment on reversing differences % 1 of Loss carryforward (recovery not probable) % Tax rate adjustment on loss carryback % $ % Effective tax rate %