On excel

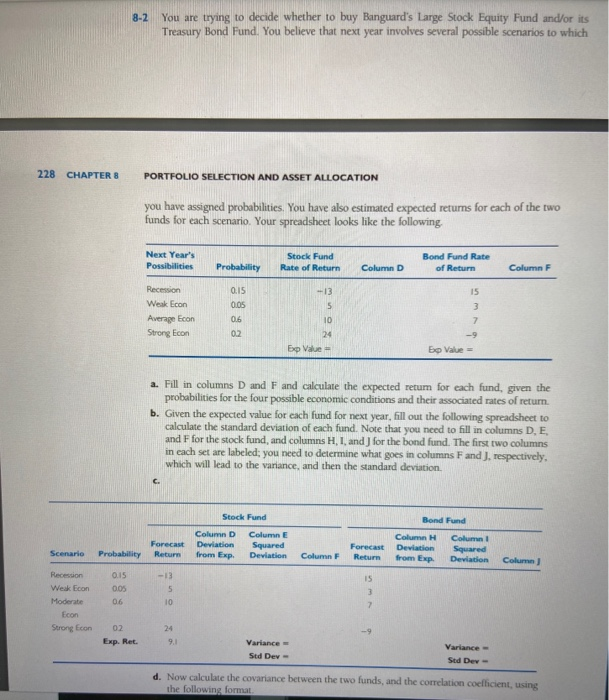

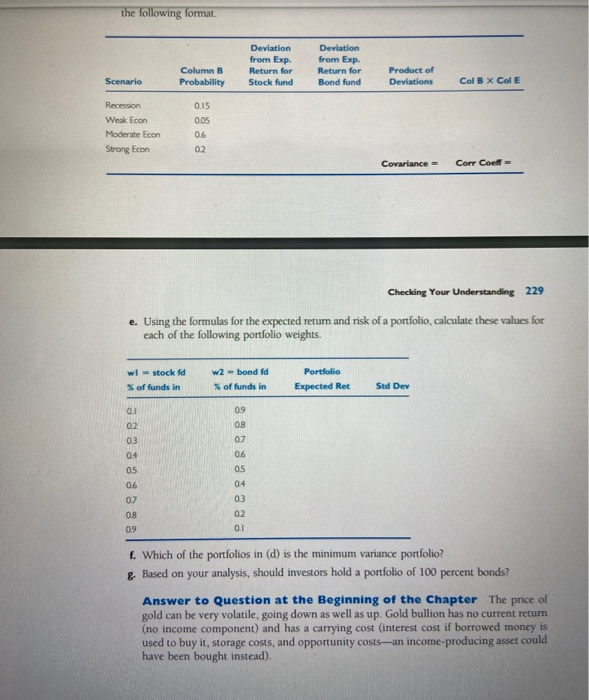

8-2 You are trying to decide whether to buy Banguard's Large Stock Equity Fund and/or its Treasury Bond Fund. You believe that next year involves several possible scenarios to which 228 CHAPTER 8 PORTFOLIO SELECTION AND ASSET ALLOCATION you have assigned probabilities. You have also estimated expected returns for each of the two funds for each scenario. Your spreadsheet looks like the following Next Year's Possibilities Probability Stock Fund Rate of Return Bond Fund Rate of Return Column D Column F -13 Recession Weak Econ Average Econ Strong Econ 0.15 0.05 0.6 0.2 5 10 24 Exp Value 15 3 7 -9 Eo Value = a. Fill in columns D and F and calculate the expected retum for each fund, given the probabilities for the four possible economic conditions and their associated rates of return. b. Given the expected value for each fund for next year, fill out the following spreadsheet to calculate the standard deviation of each fund. Note that you need to fill in columns D, E. and F for the stock fund, and columns H, I, and for the bond fund. The first two columns in each set are labeled; you need to determine what goes in columns F and respectively, which will lead to the variance, and then the standard deviation Stock Fund Bond Fund Column D Deviation Forecast Return Column E Squared Deviation Scenario Column H Deviation from Exp Probability from Exp Column Squared Deviation Forecast Return Column F Column] -13 Recession Weak Econ Moderate Econ Strong con 0.15 005 06 5 10 15 3 7 24 02 Exp. Ret 9.1 Variance Std Dev- Variance Std Dev- d. Now calculate the covariance between the two funds, and the correlation coefficient, using the following format the following format Column B Probability Deviation from Exp. Return for Stock fund Deviation from Exp. Return for Bond fund Product of Deviations Scenario Col B x Col E 0.15 Recession Weak Econ Moderate Econ Strong Econ 0.05 06 0.2 Covariance Corr Coeff- Checking Your Understanding 229 e. Using the formulas for the expected return and risk of a portfolio, calculate these values for each of the following portfolio weights. wl - stock fd w2 - bond id % of funds in Portfolio Expected Ret % of funds in Std Dev 0.1 0.9 0.8 0.2 03 04 05 0.6 0.7 0.7 06 05 04 03 02 0.1 0.8 0.9 f. Which of the portfolios in (d) is the minimum variance portfolio? g. Based on your analysis, should investors hold a portfolio of 100 percent bonds? Answer to Question at the Beginning of the Chapter The price of gold can be very volatile, going down as well as up. Gold bullion has no current retum (no income component) and has a carrying cost interest cost if borrowed money is used to buy it, storage costs, and opportunity costs-an income-producing asset could have been bought instead)