Question

On January 1, 2014, Prince Corporation acquired 70% of the 100,000 outstanding voting shares of Song Limited for a cash consideration of $1,015,000. On that

On January 1, 2014, Prince Corporation acquired 70% of the 100,000 outstanding voting shares of Song Limited for a cash consideration of $1,015,000. On that date, shares of Song Limited were trading for $14.00 per share on the national stock exchange. The shareholders equity of Song Limited on the acquisition date consisted of common shares with a carrying value of $710,000, contributed surplus of $110,000 and retained earnings of $320,000. All the assets and liabilities of Song were fairly valued on its balance sheet except that capital assets were undervalued by $120,000 and long-term debt with a book value of $210,000 had a fair value of $160,000. The capital assets had a remaining useful life of six years and the long-term debt matured on December 31, 2018.

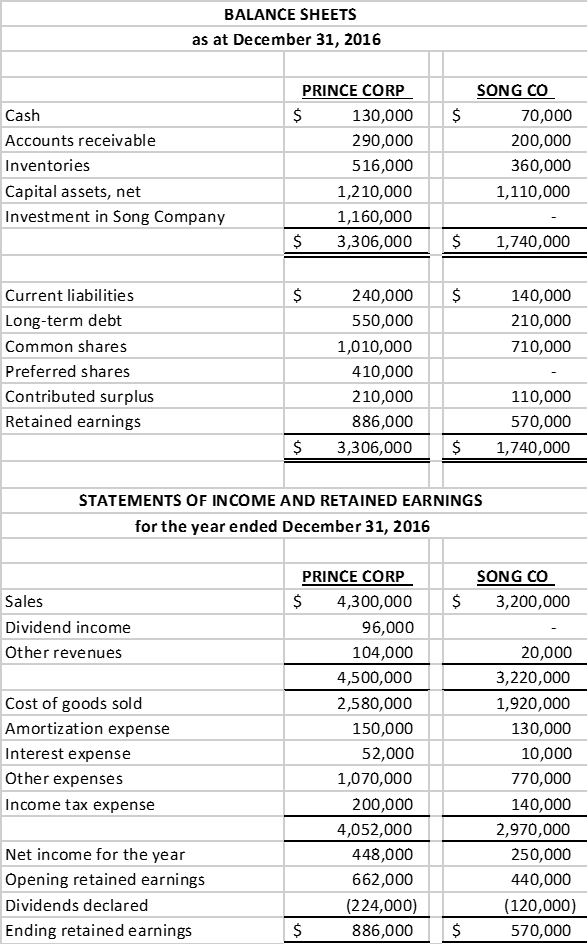

Prince Corporation accounts for its investment in Song Limited using the cost method and values the non-controlling interest in Song Limited at its fair value as determined from the market value of its shares on the acquisition date. The Financial statements of the two companies for the year ended December 31, 2016 appear on the next page.

Additional information:

- Goodwill impairment tests are carried out annually. During 2014, goodwill impairment was determined to be $26,000 on the parents share of goodwill and $5,000 on the NCI share. In 2016, impairment in the amounts of $35,000 and $6,000 respectively was found to have occurred.

- Song Company declared its 2016 dividends on December 15, 2016, with payment to be made on January 15, 2017.

- During 2016, Prince charged rental fees of $30,000 to Song. Prince estimated that its cost to provide the rental services to Song was $20,000 for the year. At December 31, 2016, Song owed Prince $7,500 for the last quarters rental services.

- Ignore income taxes on the allocation and amortization of the acquisition differential.

Required:

Prepare the consolidated financial statements of Prince Corporation and its subsidiary for the year ended December 31, 2016.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Research In Finance Volume 24

Authors: Andrew H. Chen

1st Edition

0762313773, 978-0762313778