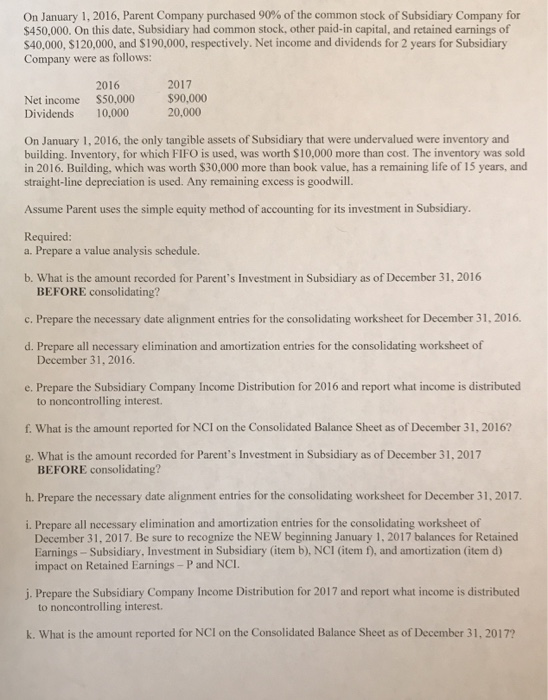

On January 1, 2016, Parent Company purchased 90% of the common stock of Subsidiary Company for $450,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of 40,000, $120,000, and S190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as follows: 2016 2017 Net income $50,000 $90,000 Dividends 10,000 20,000 On January 1, 2016, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $10,000 more than cost. The inventory was sold in 2016. Building, which was worth $30,000 more than book value, has a remaining life of 15 years, and straight-line depreciation is used. Any remaining excess is goodwill. Assume Parent uses the simple equity method of accounting for its investment in Subsidiary. Required a. Prepare a value analysis schedule b. What is the amount recorded for Parent's Investment in Subsidiary as of December 31, 2016 BEFORE consolidating? c. Prepare the necessary date alignment entries for the consolidating worksheet for December 31,2016. d. Prepare all necessary elimination and amortization entries for the consolidating worksheet of December 31, 2016. e. Prepare the Subsidiary Company Income Distribution for 2016 and report what income is distributed f. What is the amount reported for NCI on the Consolidated Balance Sheet as of December 31, 20162 g. What is the amount recorded for Parent's Investment in Subsidiary as of December 31,2017 h. Prepare the necessary date alignment entries for the consolidating worksheet for December 31, 2017 i. Prepare all necessary elimination and amortization entries for the consolidating worksheet of to noncontrolling interest. BEFORE consolidating? December 31, 2017. Be sure to recognize the NEW beginning January 1, 2017 balances for Retained Earnings-Subsidiary, Investment in Subsidiary (item b), NCI (item f), and amortization (item d) impact on Retained Earnings- P and NCI. j. Prepare the Subsidiary Company Income Distribution for 2017 and report what income is distributed to noncontrolling interest. k. What is the amount reported for NCI on the Consolidated Balance Sheet as of December 31, 2017? On January 1, 2016, Parent Company purchased 90% of the common stock of Subsidiary Company for $450,000. On this date, Subsidiary had common stock, other paid-in capital, and retained earnings of 40,000, $120,000, and S190,000, respectively. Net income and dividends for 2 years for Subsidiary Company were as follows: 2016 2017 Net income $50,000 $90,000 Dividends 10,000 20,000 On January 1, 2016, the only tangible assets of Subsidiary that were undervalued were inventory and building. Inventory, for which FIFO is used, was worth $10,000 more than cost. The inventory was sold in 2016. Building, which was worth $30,000 more than book value, has a remaining life of 15 years, and straight-line depreciation is used. Any remaining excess is goodwill. Assume Parent uses the simple equity method of accounting for its investment in Subsidiary. Required a. Prepare a value analysis schedule b. What is the amount recorded for Parent's Investment in Subsidiary as of December 31, 2016 BEFORE consolidating? c. Prepare the necessary date alignment entries for the consolidating worksheet for December 31,2016. d. Prepare all necessary elimination and amortization entries for the consolidating worksheet of December 31, 2016. e. Prepare the Subsidiary Company Income Distribution for 2016 and report what income is distributed f. What is the amount reported for NCI on the Consolidated Balance Sheet as of December 31, 20162 g. What is the amount recorded for Parent's Investment in Subsidiary as of December 31,2017 h. Prepare the necessary date alignment entries for the consolidating worksheet for December 31, 2017 i. Prepare all necessary elimination and amortization entries for the consolidating worksheet of to noncontrolling interest. BEFORE consolidating? December 31, 2017. Be sure to recognize the NEW beginning January 1, 2017 balances for Retained Earnings-Subsidiary, Investment in Subsidiary (item b), NCI (item f), and amortization (item d) impact on Retained Earnings- P and NCI. j. Prepare the Subsidiary Company Income Distribution for 2017 and report what income is distributed to noncontrolling interest. k. What is the amount reported for NCI on the Consolidated Balance Sheet as of December 31, 2017