Answered step by step

Verified Expert Solution

Question

1 Approved Answer

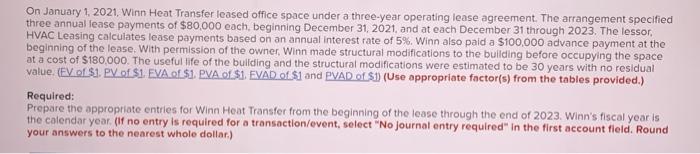

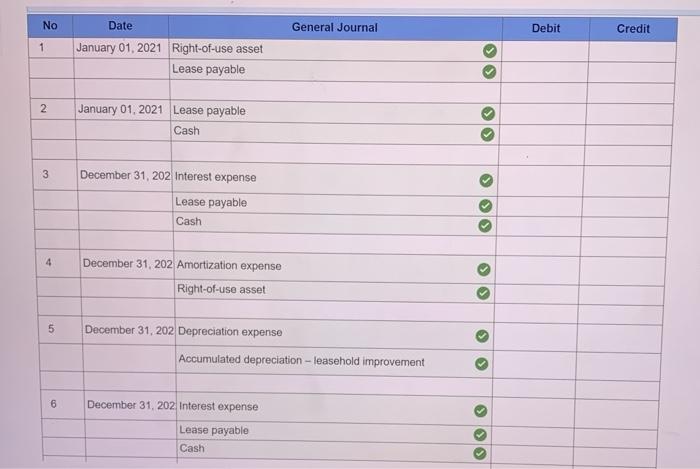

On January 1, 2021. Winn Heat Transfer leased office space under a three-year operating lease agreement. The arrangement specified three annual lease payments of $80,000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Care And Counsel For Combat Trauma Training Program Workbook For Audit Only

Authors: Cru Military, American Association Of Christian Counselors, Light University, Karen D Watkins

1st Edition

0986363081, 978-0986363085