Answered step by step

Verified Expert Solution

Question

1 Approved Answer

On January 1, Year 1, a company purchased major pieces of manufacturing equipment for a total of $60 million. The company uses straight-line depreciation

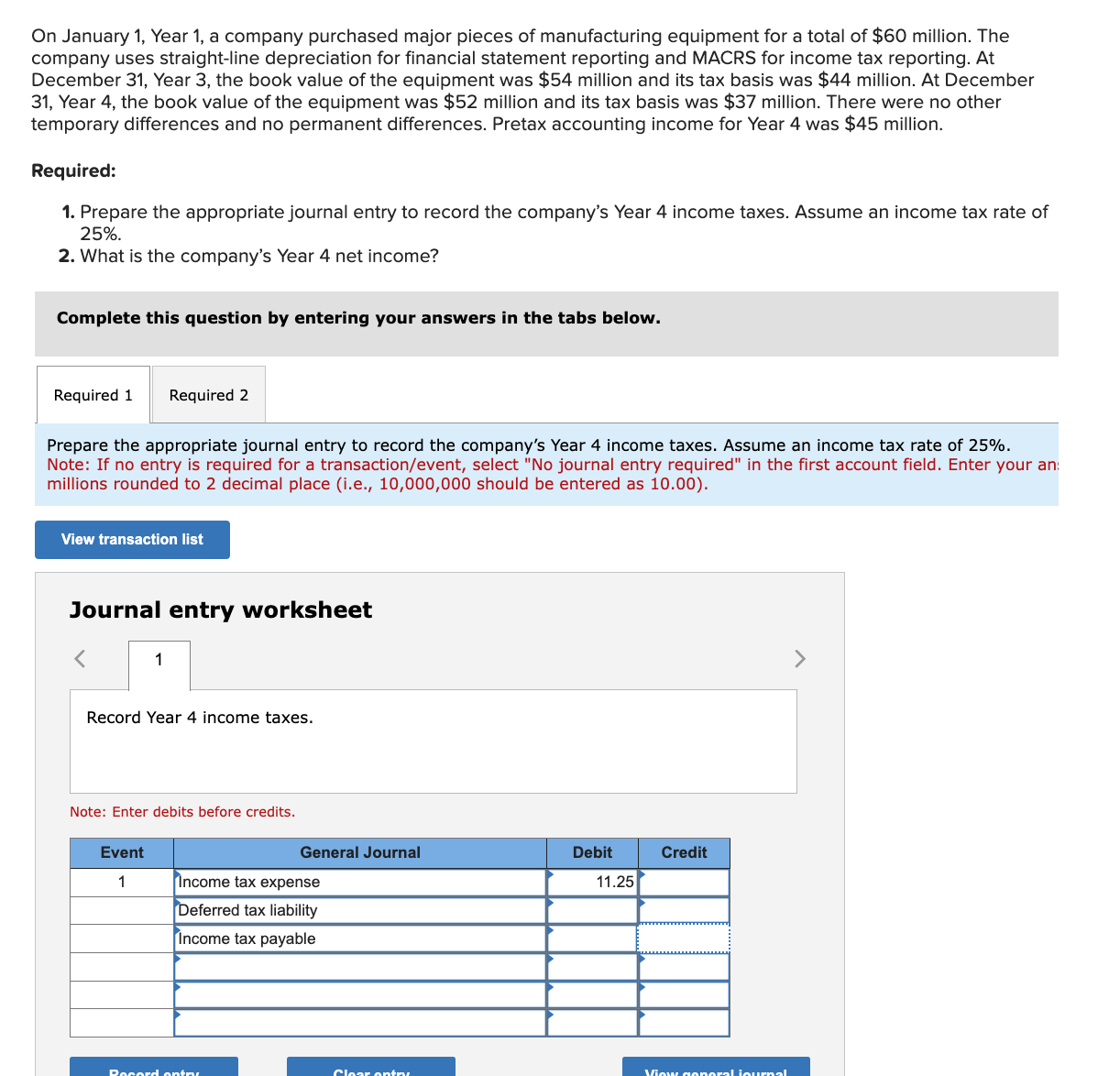

On January 1, Year 1, a company purchased major pieces of manufacturing equipment for a total of $60 million. The company uses straight-line depreciation for financial statement reporting and MACRS for income tax reporting. At December 31, Year 3, the book value of the equipment was $54 million and its tax basis was $44 million. At December 31, Year 4, the book value of the equipment was $52 million and its tax basis was $37 million. There were no other temporary differences and no permanent differences. Pretax accounting income for Year 4 was $45 million. Required: 1. Prepare the appropriate journal entry to record the company's Year 4 income taxes. Assume an income tax rate of 25%. 2. What is the company's Year 4 net income? Complete this question by entering your answers in the tabs below. Required 1 Required 2 Prepare the appropriate journal entry to record the company's Year 4 income taxes. Assume an income tax rate of 25%. Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field. Enter your an: millions rounded to 2 decimal place (i.e., 10,000,000 should be entered as 10.00). View transaction list Journal entry worksheet 1 Record Year 4 income taxes. Note: Enter debits before credits. Event General Journal Debit Credit 1 Income tax expense 11.25 Deferred tax liability Income tax payable Record antes Clear antnu. View general inurnal

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting

Authors: J. David Spiceland, James Sepe, Mark Nelson, Wayne Thomas

10th edition

1260481956, 1260310175, 978-1260481952