Question

On page 2, the document states that this is a Defined Benefit Plan. What information in the plan document can you find that proves this

On page 2, the document states that this is a Defined Benefit Plan. What information in the plan document can you find that proves this is true? Fully explain your answer.

Who contributes to the plan? How, specifically, are each partys contributions determined?

When is the normal retirement date? Explain how early retirement and postponed retirement work for this plan.

Locate the pension benefit formula. Explain, in general and in your own words, how increases or decreases in annual earnings would impact the retirement benefit earned by a member.

According to the plan, what are the tax implications of a plan members contributions, the plan sponsors contributions, and the interest earned on contributions?

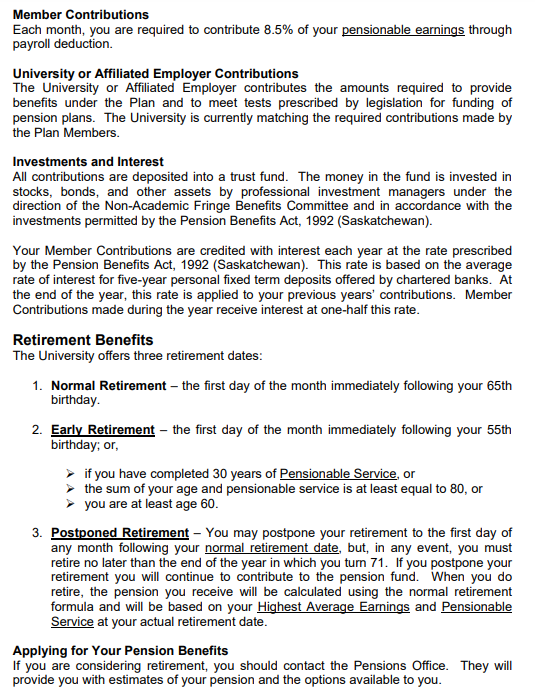

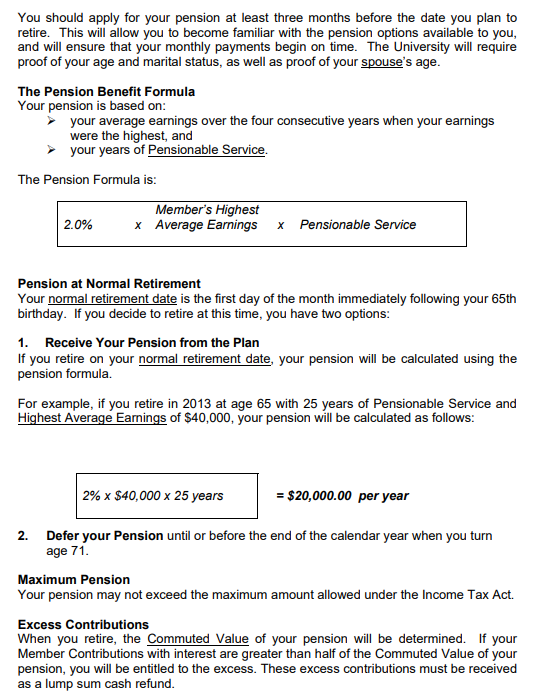

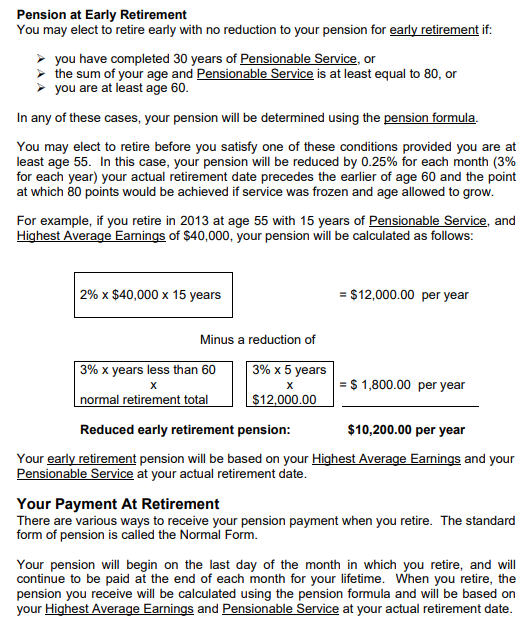

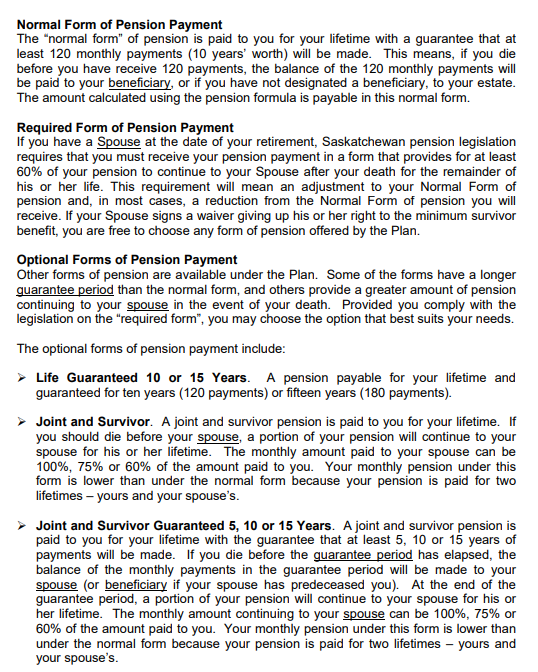

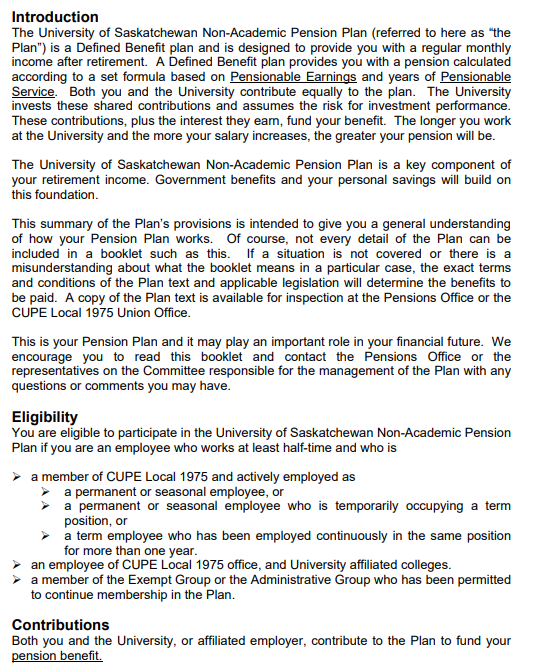

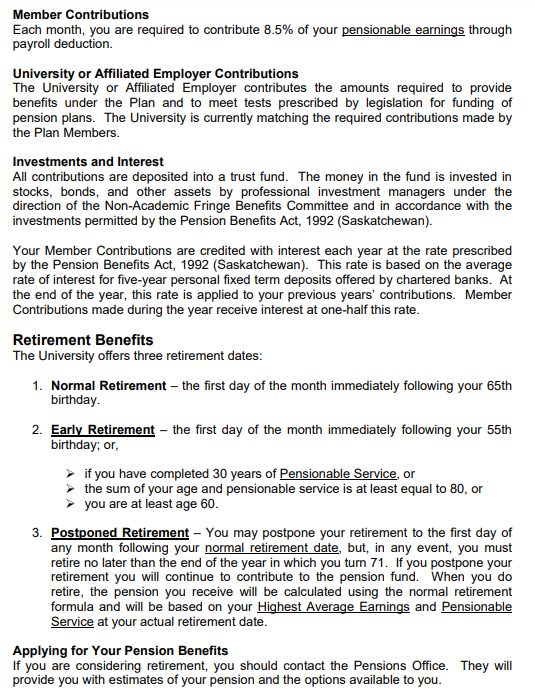

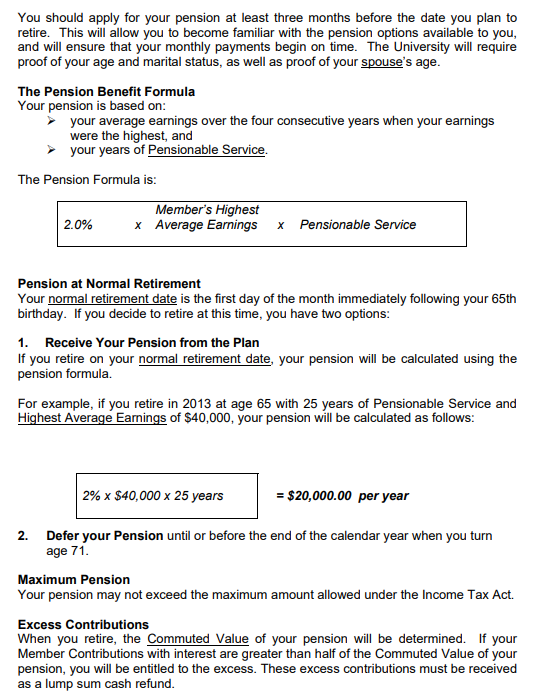

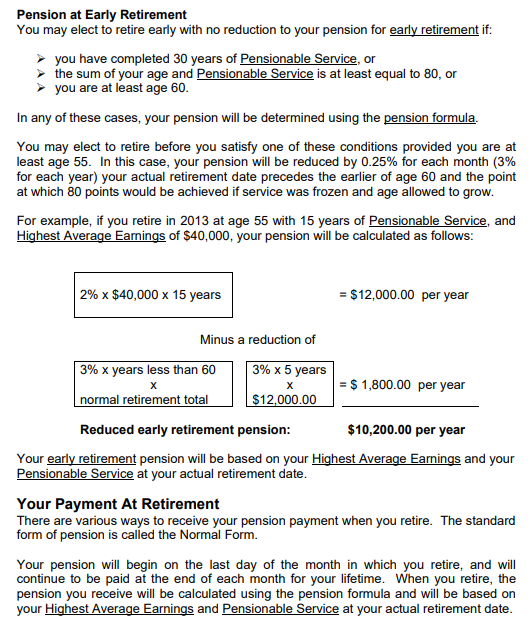

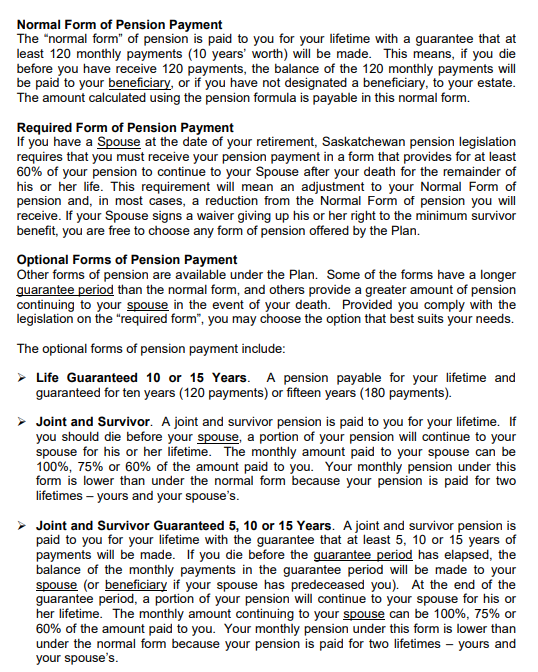

Introduction The University of Saskatchewan Non-Academic Pension Plan (referred to here as "the Plan") is a Defined Benefit plan and is designed to provide you with a regular monthly income after retirement. A Defined Benefit plan provides you with a pension calculated according to a set formula based on Pensionable Earnings and years of Pensionable Service. Both you and the University contribute equally to the plan. The University invests these shared contributions and assumes the risk for investment performance. These contributions, plus the interest they earn, fund your benefit. The longer you work at the University and the more your salary increases, the greater your pension will be. The University of Saskatchewan Non-Academic Pension Plan is a key component of your retirement income. Government benefits and your personal savings will build on this foundation. This summary of the Plan's provisions is intended to give you a general understanding of how your Pension Plan works. Of course, not every detail of the Plan can be included in a booklet such as this. If a situation is not covered or there is a misunderstanding about what the booklet means in a particular case, the exact terms and conditions of the Plan text and applicable legislation will determine the benefits to be paid. A copy of the Plan text is available for inspection at the Pensions Office or the CUPE Local 1975 Union Office. This is your Pension Plan and it may play an important role in your financial future. We encourage you to read this booklet and contact the Pensions Office or the representatives on the Committee responsible for the management of the Plan with any questions or comments you may have. Eligibility You are eligible to participate in the University of Saskatchewan Non-Academic Pension Plan if you are an employee who works at least half-time and who is a member of CUPE Local 1975 and actively employed as - a permanent or seasonal employee, or a permanent or seasonal employee who is temporarily occupying a term position, or a term employee who has been employed continuously in the same position for more than one year. an employee of CUPE Local 1975 office, and University affiliated colleges. a member of the Exempt Group or the Administrative Group who has been permitted to continue membership in the Plan. Contributions Both you and the University, or affiliated employer, contribute to the Plan to fund your pension benefit. Member Contributions Each month, you are required to contribute 8.5% of your pensionable earnings through payroll deduction. University or Affiliated Employer Contributions The University or Affiliated Employer contributes the amounts required to provide benefits under the Plan and to meet tests prescribed by legislation for funding of pension plans. The University is currently matching the required contributions made by the Plan Members. Investments and Interest All contributions are deposited into a trust fund. The money in the fund is invested in stocks, bonds, and other assets by professional investment managers under the direction of the Non-Academic Fringe Benefits Committee and in accordance with the investments permitted by the Pension Benefits Act, 1992 (Saskatchewan). Your Member Contributions are credited with interest each year at the rate prescribed by the Pension Benefits Act, 1992 (Saskatchewan). This rate is based on the average rate of interest for five-year personal fixed term deposits offered by chartered banks. At the end of the year, this rate is applied to your previous years' contributions. Member Contributions made during the year receive interest at one-half this rate. Retirement Benefits The University offers three retirement dates: 1. Normal Retirement - the first day of the month immediately following your 65 th birthday. 2. Early Retirement - the first day of the month immediately following your 55 th birthday; or, if you have completed 30 years of Pensionable Service, or the sum of your age and pensionable service is at least equal to 80 , or you are at least age 60 . 3. Postponed Retirement - You may postpone your retirement to the first day of any month following your normal retirement date, but, in any event, you must retire no later than the end of the year in which you turn 71. If you postpone your retirement you will continue to contribute to the pension fund. When you do retire, the pension you receive will be calculated using the normal retirement formula and will be based on your Highest Average Earnings and Pensionable Service at your actual retirement date. Applying for Your Pension Benefits If you are considering retirement, you should contact the Pensions Office. They will provide you with estimates of your pension and the options available to you. The Pension Benefit Formula Your pension is based on: your average earnings over the four consecutive years when your earnings were the highest, and your years of Pensionable Service. The Pension Formula is: Pension at Normal Retirement Your normal retirement date is the first day of the month immediately following your 65 th birthday. If you decide to retire at this time, you have two options: 1. Receive Your Pension from the Plan If you retire on your normal retirement date, your pension will be calculated using the pension formula. For example, if you retire in 2013 at age 65 with 25 years of Pensionable Service and Highest Average Earnings of $40,000, your pension will be calculated as follows: =$20,000.00 per year 2. Defer your Pension until or before the end of the calendar year when you turn age 71 . Maximum Pension Your pension may not exceed the maximum amount allowed under the Income Tax Act. Excess Contributions When you retire, the Commuted Value of your pension will be determined. If your Member Contributions with interest are greater than half of the Commuted Value of your pension, you will be entitled to the excess. These excess contributions must be received as a lump sum cash refund. Pension at Early Retirement You may elect to retire early with no reduction to your pension for early retirement if: you have completed 30 years of Pensionable Service, or the sum of your age and Pensionable Service is at least equal to 80 , or > you are at least age 60 . In any of these cases, your pension will be determined using the pension formula. You may elect to retire before you satisfy one of these conditions provided you are at least age 55 . In this case, your pension will be reduced by 0.25% for each month ( 3% for each year) your actual retirement date precedes the earlier of age 60 and the point at which 80 points would be achieved if service was frozen and age allowed to grow. For example, if you retire in 2013 at age 55 with 15 years of Pensionable Service, and Highest Average Earnings of $40,000, your pension will be calculated as follows: =$12,000.00 per year Minus a reduction of Your early retirement pension will be based on your Highest Average Earnings and your Pensionable Service at your actual retirement date. Your Payment At Retirement There are various ways to receive your pension payment when you retire. The standard form of pension is called the Normal Form. Your pension will begin on the last day of the month in which you retire, and will continue to be paid at the end of each month for your lifetime. When you retire, the pension you receive will be calculated using the pension formula and will be based on your HighestAverageEarningsandPensionableServiceatyouractualretirementdate. Normal Form of Pension Payment The "normal form" of pension is paid to you for your lifetime with a guarantee that at least 120 monthly payments (10 years' worth) will be made. This means, if you die before you have receive 120 payments, the balance of the 120 monthly payments will be paid to your beneficiary, or if you have not designated a beneficiary, to your estate. The amount calculated using the pension formula is payable in this normal form. Required Form of Pension Payment If you have a Spouse at the date of your retirement, Saskatchewan pension legislation requires that you must receive your pension payment in a form that provides for at least 60% of your pension to continue to your Spouse after your death for the remainder of his or her life. This requirement will mean an adjustment to your Normal Form of pension and, in most cases, a reduction from the Normal Form of pension you will receive. If your Spouse signs a waiver giving up his or her right to the minimum survivor benefit, you are free to choose any form of pension offered by the Plan. Optional Forms of Pension Payment Other forms of pension are available under the Plan. Some of the forms have a longer guarantee period than the normal form, and others provide a greater amount of pension continuing to your spouse in the event of your death. Provided you comply with the legislation on the "required form", you may choose the option that best suits your needs. The optional forms of pension payment include: Life Guaranteed 10 or 15 Years. A pension payable for your lifetime and guaranteed for ten years ( 120 payments) or fifteen years (180 payments). Joint and Survivor. A joint and survivor pension is paid to you for your lifetime. If you should die before your spouse, a portion of your pension will continue to your spouse for his or her lifetime. The monthly amount paid to your spouse can be 100%,75% or 60% of the amount paid to you. Your monthly pension under this form is lower than under the normal form because your pension is paid for two lifetimes - yours and your spouse's. Joint and Survivor Guaranteed 5, 10 or 15 Years. A joint and survivor pension is paid to you for your lifetime with the guarantee that at least 5,10 or 15 years of payments will be made. If you die before the guarantee period has elapsed, the balance of the monthly payments in the guarantee period will be made to your spouse (or beneficiary if your spouse has predeceased you). At the end of the guarantee period, a portion of your pension will continue to your spouse for his or her lifetime. The monthly amount continuing to your spouse can be 100%,75% or 60% of the amount paid to you. Your monthly pension under this form is lower than under the normal form because your pension is paid for two lifetimes - yours and your spouse's. Introduction The University of Saskatchewan Non-Academic Pension Plan (referred to here as "the Plan") is a Defined Benefit plan and is designed to provide you with a regular monthly income after retirement. A Defined Benefit plan provides you with a pension calculated according to a set formula based on Pensionable Earnings and years of Pensionable Service. Both you and the University contribute equally to the plan. The University invests these shared contributions and assumes the risk for investment performance. These contributions, plus the interest they earn, fund your benefit. The longer you work at the University and the more your salary increases, the greater your pension will be. The University of Saskatchewan Non-Academic Pension Plan is a key component of your retirement income. Government benefits and your personal savings will build on this foundation. This summary of the Plan's provisions is intended to give you a general understanding of how your Pension Plan works. Of course, not every detail of the Plan can be included in a booklet such as this. If a situation is not covered or there is a misunderstanding about what the booklet means in a particular case, the exact terms and conditions of the Plan text and applicable legislation will determine the benefits to be paid. A copy of the Plan text is available for inspection at the Pensions Office or the CUPE Local 1975 Union Office. This is your Pension Plan and it may play an important role in your financial future. We encourage you to read this booklet and contact the Pensions Office or the representatives on the Committee responsible for the management of the Plan with any questions or comments you may have. Eligibility You are eligible to participate in the University of Saskatchewan Non-Academic Pension Plan if you are an employee who works at least half-time and who is a member of CUPE Local 1975 and actively employed as - a permanent or seasonal employee, or a permanent or seasonal employee who is temporarily occupying a term position, or a term employee who has been employed continuously in the same position for more than one year. an employee of CUPE Local 1975 office, and University affiliated colleges. a member of the Exempt Group or the Administrative Group who has been permitted to continue membership in the Plan. Contributions Both you and the University, or affiliated employer, contribute to the Plan to fund your pension benefit. Member Contributions Each month, you are required to contribute 8.5% of your pensionable earnings through payroll deduction. University or Affiliated Employer Contributions The University or Affiliated Employer contributes the amounts required to provide benefits under the Plan and to meet tests prescribed by legislation for funding of pension plans. The University is currently matching the required contributions made by the Plan Members. Investments and Interest All contributions are deposited into a trust fund. The money in the fund is invested in stocks, bonds, and other assets by professional investment managers under the direction of the Non-Academic Fringe Benefits Committee and in accordance with the investments permitted by the Pension Benefits Act, 1992 (Saskatchewan). Your Member Contributions are credited with interest each year at the rate prescribed by the Pension Benefits Act, 1992 (Saskatchewan). This rate is based on the average rate of interest for five-year personal fixed term deposits offered by chartered banks. At the end of the year, this rate is applied to your previous years' contributions. Member Contributions made during the year receive interest at one-half this rate. Retirement Benefits The University offers three retirement dates: 1. Normal Retirement - the first day of the month immediately following your 65 th birthday. 2. Early Retirement - the first day of the month immediately following your 55 th birthday; or, if you have completed 30 years of Pensionable Service, or the sum of your age and pensionable service is at least equal to 80 , or you are at least age 60 . 3. Postponed Retirement - You may postpone your retirement to the first day of any month following your normal retirement date, but, in any event, you must retire no later than the end of the year in which you turn 71. If you postpone your retirement you will continue to contribute to the pension fund. When you do retire, the pension you receive will be calculated using the normal retirement formula and will be based on your Highest Average Earnings and Pensionable Service at your actual retirement date. Applying for Your Pension Benefits If you are considering retirement, you should contact the Pensions Office. They will provide you with estimates of your pension and the options available to you. The Pension Benefit Formula Your pension is based on: your average earnings over the four consecutive years when your earnings were the highest, and your years of Pensionable Service. The Pension Formula is: Pension at Normal Retirement Your normal retirement date is the first day of the month immediately following your 65 th birthday. If you decide to retire at this time, you have two options: 1. Receive Your Pension from the Plan If you retire on your normal retirement date, your pension will be calculated using the pension formula. For example, if you retire in 2013 at age 65 with 25 years of Pensionable Service and Highest Average Earnings of $40,000, your pension will be calculated as follows: =$20,000.00 per year 2. Defer your Pension until or before the end of the calendar year when you turn age 71 . Maximum Pension Your pension may not exceed the maximum amount allowed under the Income Tax Act. Excess Contributions When you retire, the Commuted Value of your pension will be determined. If your Member Contributions with interest are greater than half of the Commuted Value of your pension, you will be entitled to the excess. These excess contributions must be received as a lump sum cash refund. Pension at Early Retirement You may elect to retire early with no reduction to your pension for early retirement if: you have completed 30 years of Pensionable Service, or the sum of your age and Pensionable Service is at least equal to 80 , or > you are at least age 60 . In any of these cases, your pension will be determined using the pension formula. You may elect to retire before you satisfy one of these conditions provided you are at least age 55 . In this case, your pension will be reduced by 0.25% for each month ( 3% for each year) your actual retirement date precedes the earlier of age 60 and the point at which 80 points would be achieved if service was frozen and age allowed to grow. For example, if you retire in 2013 at age 55 with 15 years of Pensionable Service, and Highest Average Earnings of $40,000, your pension will be calculated as follows: =$12,000.00 per year Minus a reduction of Your early retirement pension will be based on your Highest Average Earnings and your Pensionable Service at your actual retirement date. Your Payment At Retirement There are various ways to receive your pension payment when you retire. The standard form of pension is called the Normal Form. Your pension will begin on the last day of the month in which you retire, and will continue to be paid at the end of each month for your lifetime. When you retire, the pension you receive will be calculated using the pension formula and will be based on your HighestAverageEarningsandPensionableServiceatyouractualretirementdate. Normal Form of Pension Payment The "normal form" of pension is paid to you for your lifetime with a guarantee that at least 120 monthly payments (10 years' worth) will be made. This means, if you die before you have receive 120 payments, the balance of the 120 monthly payments will be paid to your beneficiary, or if you have not designated a beneficiary, to your estate. The amount calculated using the pension formula is payable in this normal form. Required Form of Pension Payment If you have a Spouse at the date of your retirement, Saskatchewan pension legislation requires that you must receive your pension payment in a form that provides for at least 60% of your pension to continue to your Spouse after your death for the remainder of his or her life. This requirement will mean an adjustment to your Normal Form of pension and, in most cases, a reduction from the Normal Form of pension you will receive. If your Spouse signs a waiver giving up his or her right to the minimum survivor benefit, you are free to choose any form of pension offered by the Plan. Optional Forms of Pension Payment Other forms of pension are available under the Plan. Some of the forms have a longer guarantee period than the normal form, and others provide a greater amount of pension continuing to your spouse in the event of your death. Provided you comply with the legislation on the "required form", you may choose the option that best suits your needs. The optional forms of pension payment include: Life Guaranteed 10 or 15 Years. A pension payable for your lifetime and guaranteed for ten years ( 120 payments) or fifteen years (180 payments). Joint and Survivor. A joint and survivor pension is paid to you for your lifetime. If you should die before your spouse, a portion of your pension will continue to your spouse for his or her lifetime. The monthly amount paid to your spouse can be 100%,75% or 60% of the amount paid to you. Your monthly pension under this form is lower than under the normal form because your pension is paid for two lifetimes - yours and your spouse's. Joint and Survivor Guaranteed 5, 10 or 15 Years. A joint and survivor pension is paid to you for your lifetime with the guarantee that at least 5,10 or 15 years of payments will be made. If you die before the guarantee period has elapsed, the balance of the monthly payments in the guarantee period will be made to your spouse (or beneficiary if your spouse has predeceased you). At the end of the guarantee period, a portion of your pension will continue to your spouse for his or her lifetime. The monthly amount continuing to your spouse can be 100%,75% or 60% of the amount paid to you. Your monthly pension under this form is lower than under the normal form because your pension is paid for two lifetimes - yours and your spouse'sStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Management and Cost Accounting

Authors: Alnoor Bhimani, Charles T. Horngren, Srikant M. Datar, Madhav V. Rajan

6th edition

1292063467, 978-1292063461