only answer 2 3 &4 and please explain

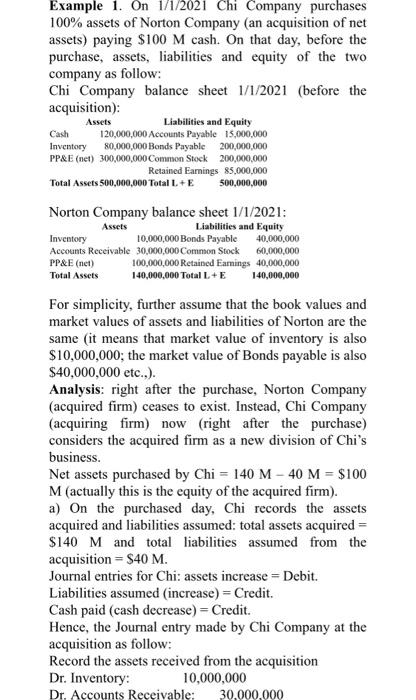

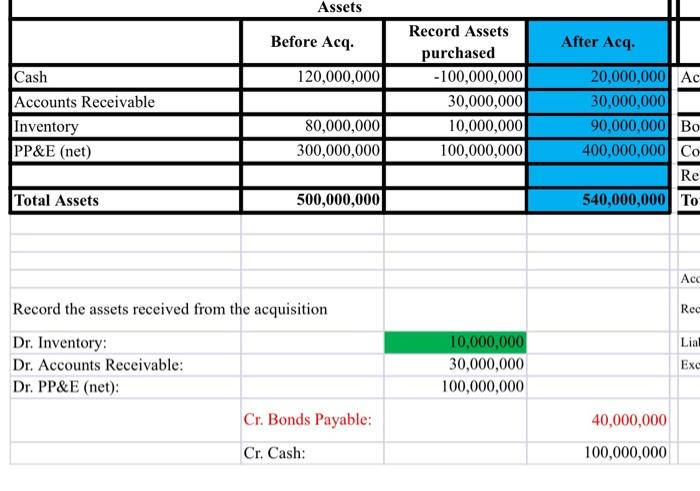

Question 1) In the video/transcript example: Chi Company purchased 100% of Norton Company. Right after the acquisition: - Total assets of Chi increased by $40,000,000 - Total liabilities of Chi increased by $40,000,000 - Total equity of Chi stays the same. Why equity stays the same? Questions 2,3,4,5. For questions 2, 3, 4, and 5 only: we modify example 1 in the transcript/video: instead of paying $100 Mcash, if Chi Company issues stock $100 M to acquire Norton Company, all the other information stays the same, then (please use the NEW FACT that Chi Company issues stocks for the acquisition): 2) What is the journal entry Chi Company uses to record the transaction of the acquisition? 3) What is total asset of Chi Company after the acquisition (show your calculation)? 4) What is total equity of Chi Company after the acquisition (show your calculation)? Example 1. On 1/1/2021 Chi Company purchases 100% assets of Norton Company (an acquisition of net assets) paying $100 M cash. On that day, before the purchase, assets, liabilities and equity of the two company as follow: Chi Company balance sheet 1/1/2021 (before the acquisition): Assets Liabilities and Equity Cash 120,000,000 Accounts Payable 15.000.000 Inventory 80,000,000 Bonds Payable 200,000,000 PP&E (net) 300,000,000 Common Stock 200,000,000 Retained Earnings 85,000,000 Total Assets 500,000,000 Total L+E 500,000,000 Norton Company balance sheet 1/1/2021: Assets Liabilities and Equity Inventory 10,000,000 Bonds Payable 40,000,000 Accounts Receivable 30,000,000 Common Stock 60,000,000 PP&E (net) 100,000,000 Retained Eamings 40,000,000 Total Assets 140,000,000 Total L+E 140,000,000 For simplicity, further assume that the book values and market values of assets and liabilities of Norton are the same (it means that market value of inventory is also $10,000,000; the market value of Bonds payable is also $40,000,000 etc..). Analysis: right after the purchase, Norton Company (acquired firm) ceases to exist. Instead, Chi Company (acquiring firm) now (right after the purchase) considers the acquired firm as a new division of Chi's business. Net assets purchased by Chi = 140 M - 40 M = $100 M (actually this is the equity of the acquired firm). a) On the purchased day, Chi records the assets acquired and liabilities assumed: total assets acquired = $140 M and total liabilities assumed from the acquisition = $40 M. Journal entries for Chi: assets increase = Debit. Liabilities assumed increase) = Credit. Cash paid (cash decrease) = Credit. Hence, the Journal entry made by Chi Company at the acquisition as follow: Record the assets received from the acquisition Dr. Inventory: 10,000,000 Dr. Accounts Receivable: 30,000,000 Assets Before Acq. After Acq. 120,000,000 Cash Accounts Receivable Inventory PP&E (net) Record Assets purchased -100,000,000 30,000,000 10,000,000 100,000,000 80,000,000 300,000,000 20,000,000 AC 30,000,000 90,000,000 Bo 400,000,000 Co Re 540,000,000 TO Total Assets 500,000,000 Acc Rec Lial Record the assets received from the acquisition Dr. Inventory: Dr. Accounts Receivable: Dr. PP&E (net): Cr. Bonds Payable: 10,000,000 30,000,000 100,000,000 Exc 40,000,000 Cr. Cash: 100,000,000