only answer the question e.

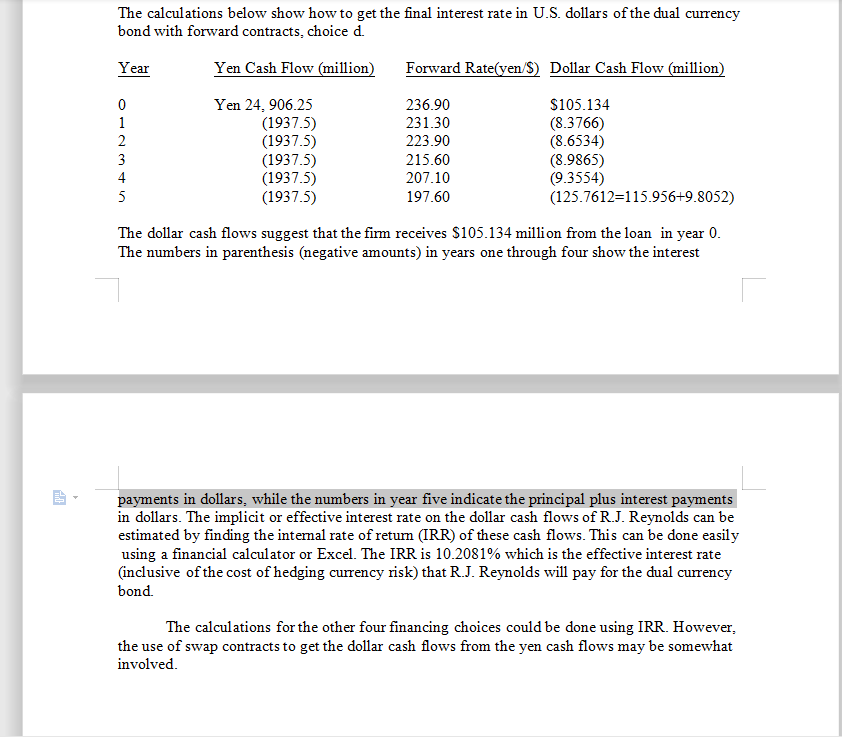

R.J. Reynolds International Financing This case demonstrates that a multinational corporation (MNC) may be able to get financing at a lower cost in foreign capital markets than in its national capital market. The idea is that an MNC can shop around in the world capital markets to get lower interest rates. But the currency that affords the lower interest rate may be subject to substantial currency risk. Thus, the final cost of such foreign borrowing in the local currency (e.g U.S. dollars) is not known with certainty to the MNC. If an MNC does not like the currency risk of its financing, it could use derivative securities, such as forward contracts, futures contracts, or swaps, to fix the currency exchange rate risk (hedge risk) of its foreign financing so that the final interest cost in its local U.S. currency is known with certainty. It is quite possible that the MNC's final cost of foreign borrowing expressed in U.S. dollars is still lower than its financing cost for borrowing the same amount in its domestic (U.S.) market. Although R.J Reynolds (RJR) needs to finance the remaining $1 billion, the best of the five choices presented in the case could finance about 10% (or $100 million) of its financing needs. Obviously, RJR will look to other financing sources in the future for the remaining $900 million. The Morgan team is currently proposing to finance the first 10% of the RJR's needs. The team probably will come up with other possible sources in the future. Our concern in this case is to decide which one of the five options is the best for RJR to finance its $100 million. R. J. Reynolds wants to shop around the world capital markets to find the least-cost source of financing $100 million. The firm has essentially six choices: a. A Eurodollar bond b. A Euroven bond hedged into U.S. dollars using forward contracts on yen c. A Euroven bond hedged into U.S. dollars using a currency swap contract d. A dual currency bond hedged into U.S. dollars using yen forward contracts e. A dual currency bond hedged into U.S. dollars using a currency swap contract f. A dual currency bond; principal repayment hedged into yen and all yen then swapped into dollars. The calculations below show how to get the final interest rate in U.S. dollars of the dual currency bond with forward contracts, choice d. Year Yen Cash Flow (million) Forward Rate(yen/S) Dollar Cash Flow (million) 0 Yen 24, 906.25 236.90 $105.134 (1937.5) 231.30 (8.3766) (1937.5) 223.90 (8.6534) (1937.5) 215.60 (8.9865) (1937.5) 207.10 (9.3554) (1937.5) 197.60 (125.7612-115.956+9.8052) The dollar cash flows suggest that the firm receives $105.134 million from the loan in year 0. The numbers in parenthesis (negative amounts) in years one through four show the interest payments in dollars, while the numbers in year five indicate the principal plus interest payments in dollars. The implicit or effective interest rate on the dollar cash flows of R.J. Reynolds can be estimated by finding the internal rate of retum (IRR) of these cash flows. This can be done easily using a financial calculator or Excel. The IRR is 10.2081% which is the effective interest rate (inclusive of the cost of hedging currency risk) that R.J. Reynolds will pay for the dual currency bond. The calculations for the other four financing choices could be done using IRR. However, the use of swap contracts to get the dollar cash flows from the yen cash flows may be somewhat involved. SAWNIO 1 2 3 4 5 R.J. Reynolds International Financing This case demonstrates that a multinational corporation (MNC) may be able to get financing at a lower cost in foreign capital markets than in its national capital market. The idea is that an MNC can shop around in the world capital markets to get lower interest rates. But the currency that affords the lower interest rate may be subject to substantial currency risk. Thus, the final cost of such foreign borrowing in the local currency (e.g U.S. dollars) is not known with certainty to the MNC. If an MNC does not like the currency risk of its financing, it could use derivative securities, such as forward contracts, futures contracts, or swaps, to fix the currency exchange rate risk (hedge risk) of its foreign financing so that the final interest cost in its local U.S. currency is known with certainty. It is quite possible that the MNC's final cost of foreign borrowing expressed in U.S. dollars is still lower than its financing cost for borrowing the same amount in its domestic (U.S.) market. Although R.J Reynolds (RJR) needs to finance the remaining $1 billion, the best of the five choices presented in the case could finance about 10% (or $100 million) of its financing needs. Obviously, RJR will look to other financing sources in the future for the remaining $900 million. The Morgan team is currently proposing to finance the first 10% of the RJR's needs. The team probably will come up with other possible sources in the future. Our concern in this case is to decide which one of the five options is the best for RJR to finance its $100 million. R. J. Reynolds wants to shop around the world capital markets to find the least-cost source of financing $100 million. The firm has essentially six choices: a. A Eurodollar bond b. A Euroven bond hedged into U.S. dollars using forward contracts on yen c. A Euroven bond hedged into U.S. dollars using a currency swap contract d. A dual currency bond hedged into U.S. dollars using yen forward contracts e. A dual currency bond hedged into U.S. dollars using a currency swap contract f. A dual currency bond; principal repayment hedged into yen and all yen then swapped into dollars. The calculations below show how to get the final interest rate in U.S. dollars of the dual currency bond with forward contracts, choice d. Year Yen Cash Flow (million) Forward Rate(yen/S) Dollar Cash Flow (million) 0 Yen 24, 906.25 236.90 $105.134 (1937.5) 231.30 (8.3766) (1937.5) 223.90 (8.6534) (1937.5) 215.60 (8.9865) (1937.5) 207.10 (9.3554) (1937.5) 197.60 (125.7612-115.956+9.8052) The dollar cash flows suggest that the firm receives $105.134 million from the loan in year 0. The numbers in parenthesis (negative amounts) in years one through four show the interest payments in dollars, while the numbers in year five indicate the principal plus interest payments in dollars. The implicit or effective interest rate on the dollar cash flows of R.J. Reynolds can be estimated by finding the internal rate of retum (IRR) of these cash flows. This can be done easily using a financial calculator or Excel. The IRR is 10.2081% which is the effective interest rate (inclusive of the cost of hedging currency risk) that R.J. Reynolds will pay for the dual currency bond. The calculations for the other four financing choices could be done using IRR. However, the use of swap contracts to get the dollar cash flows from the yen cash flows may be somewhat involved. SAWNIO 1 2 3 4 5