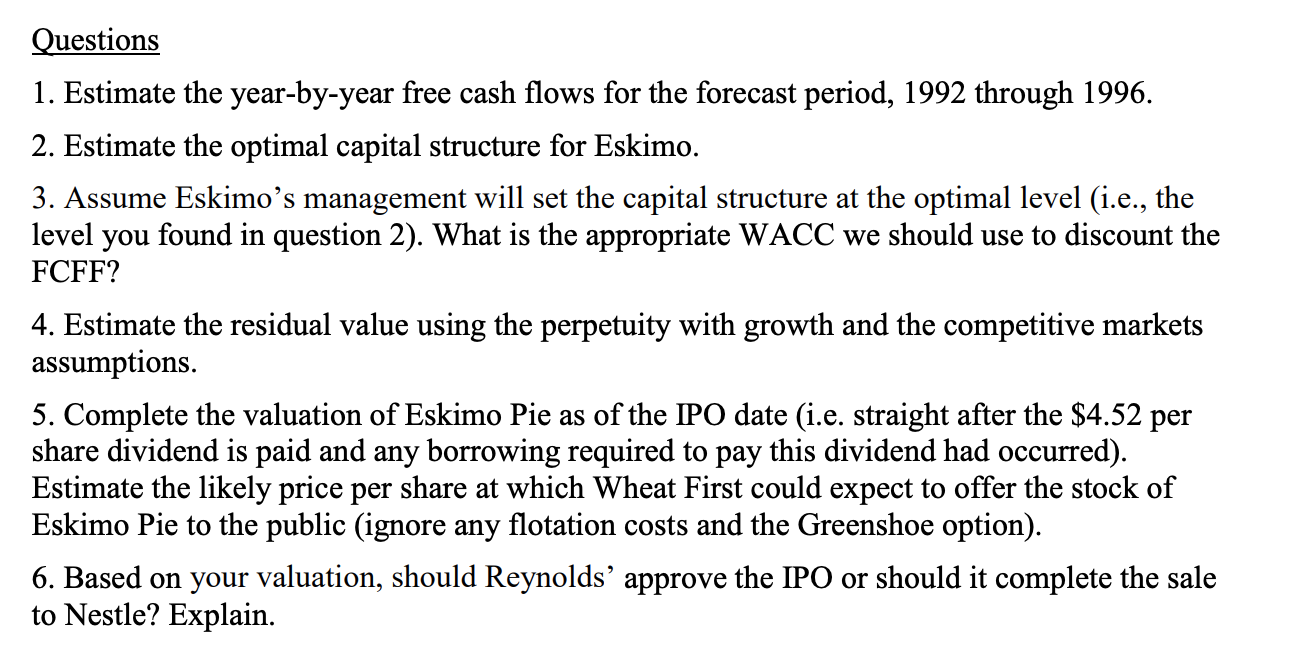

Only need answer to question 3

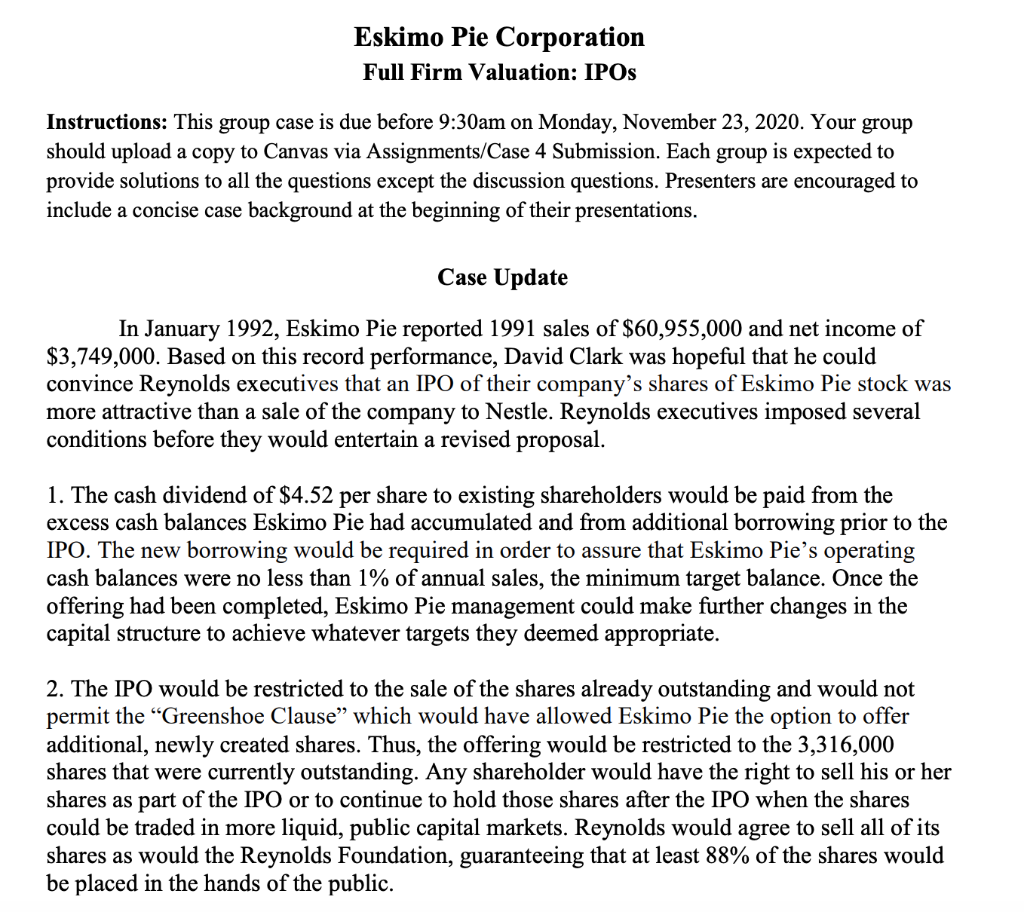

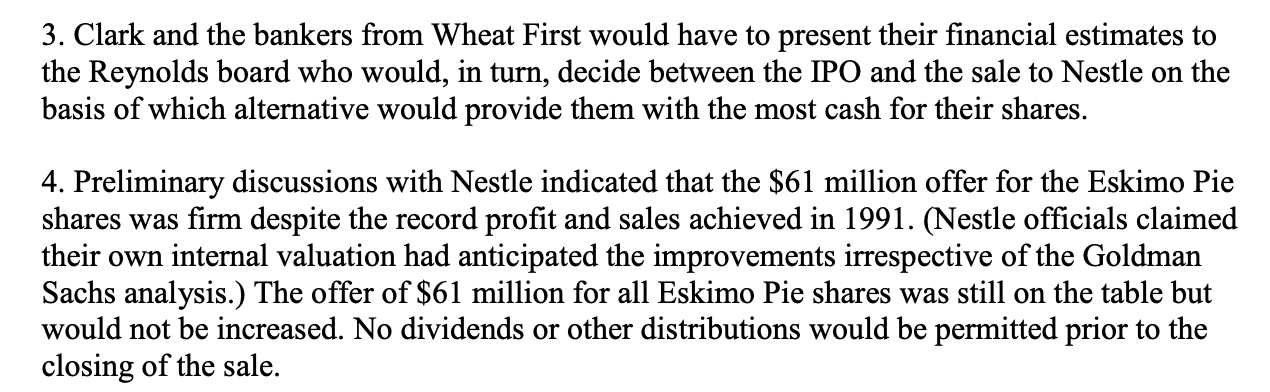

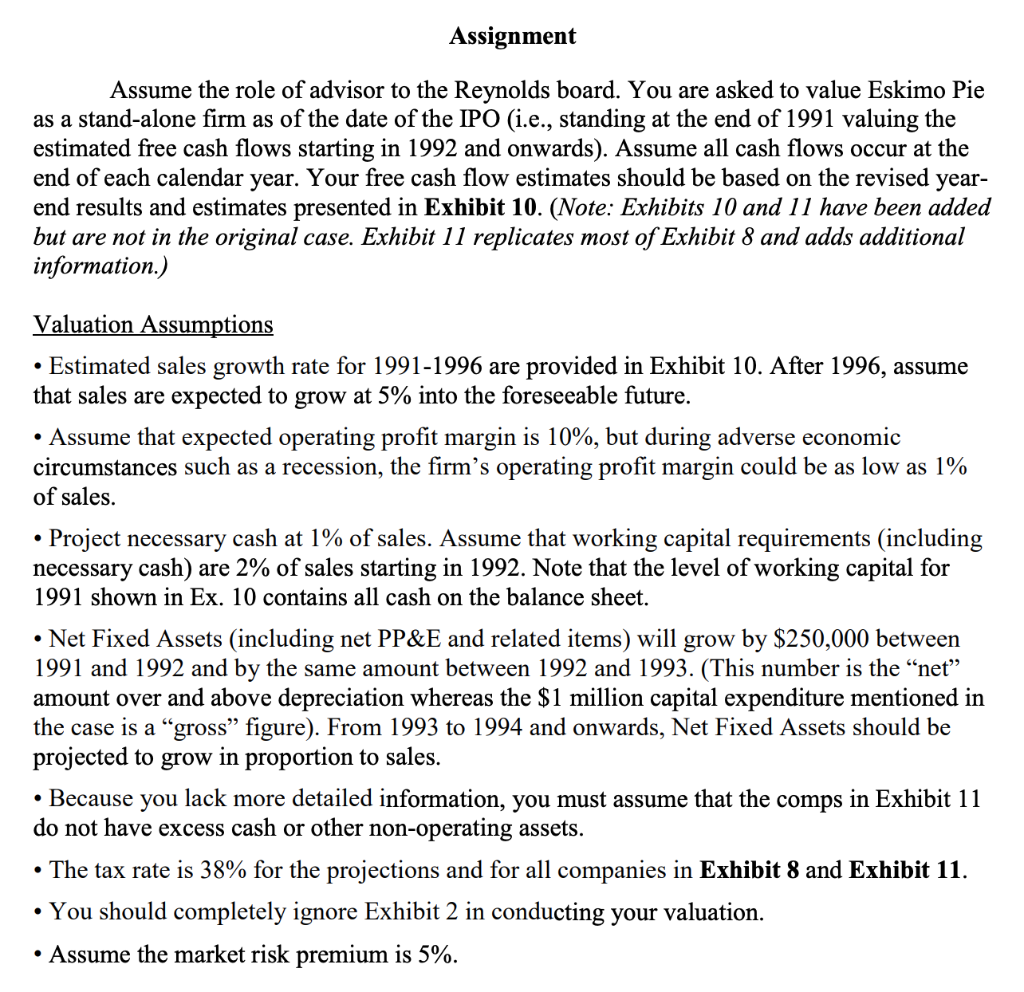

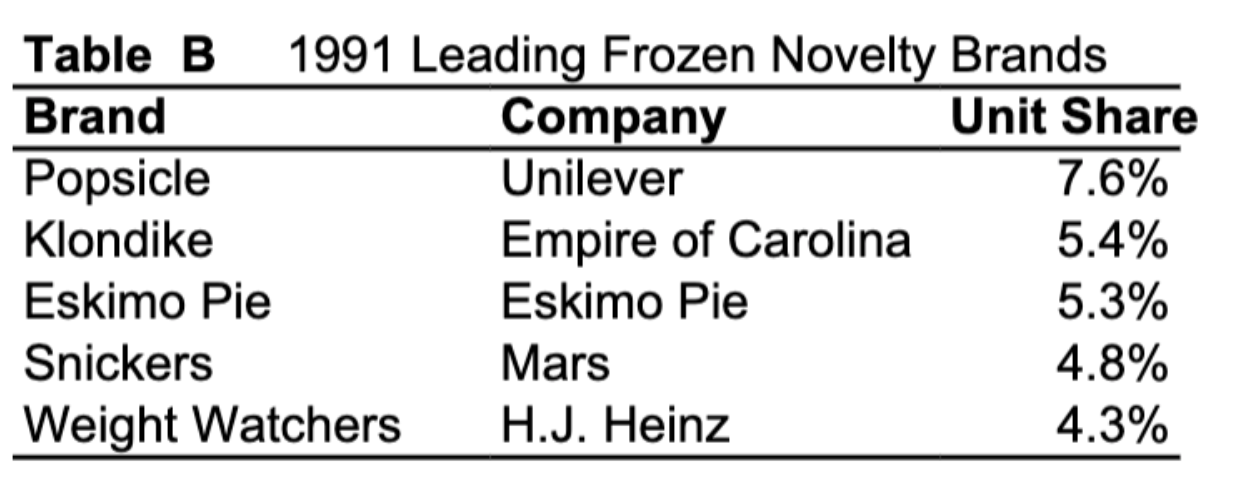

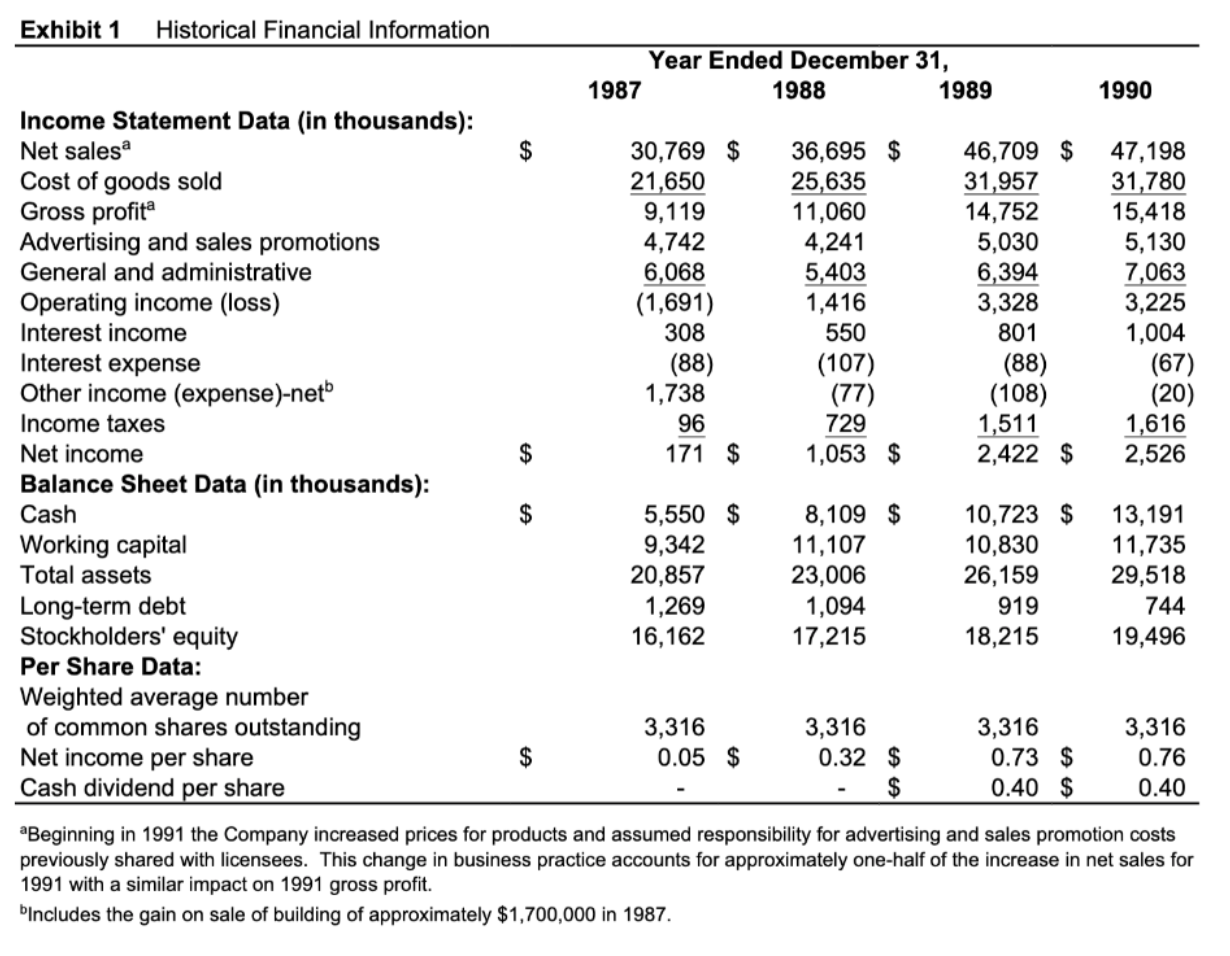

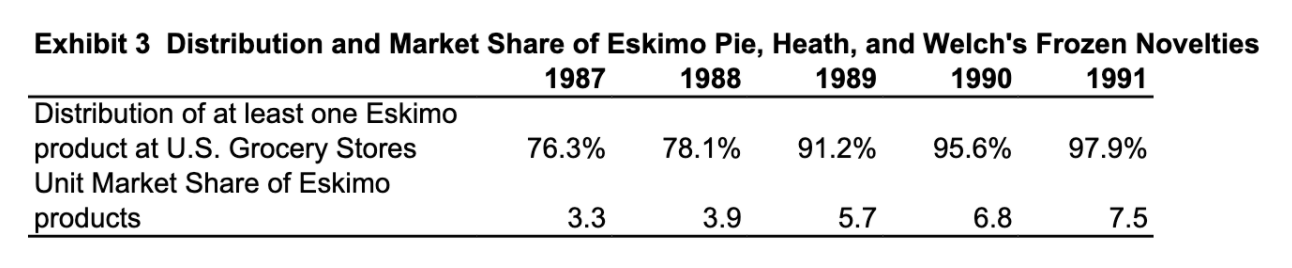

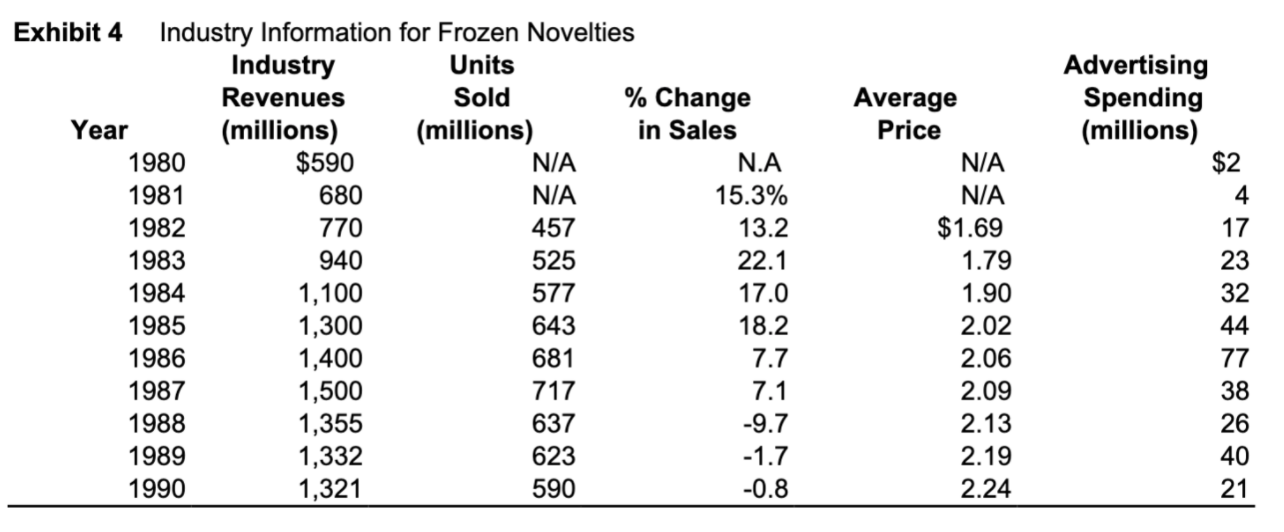

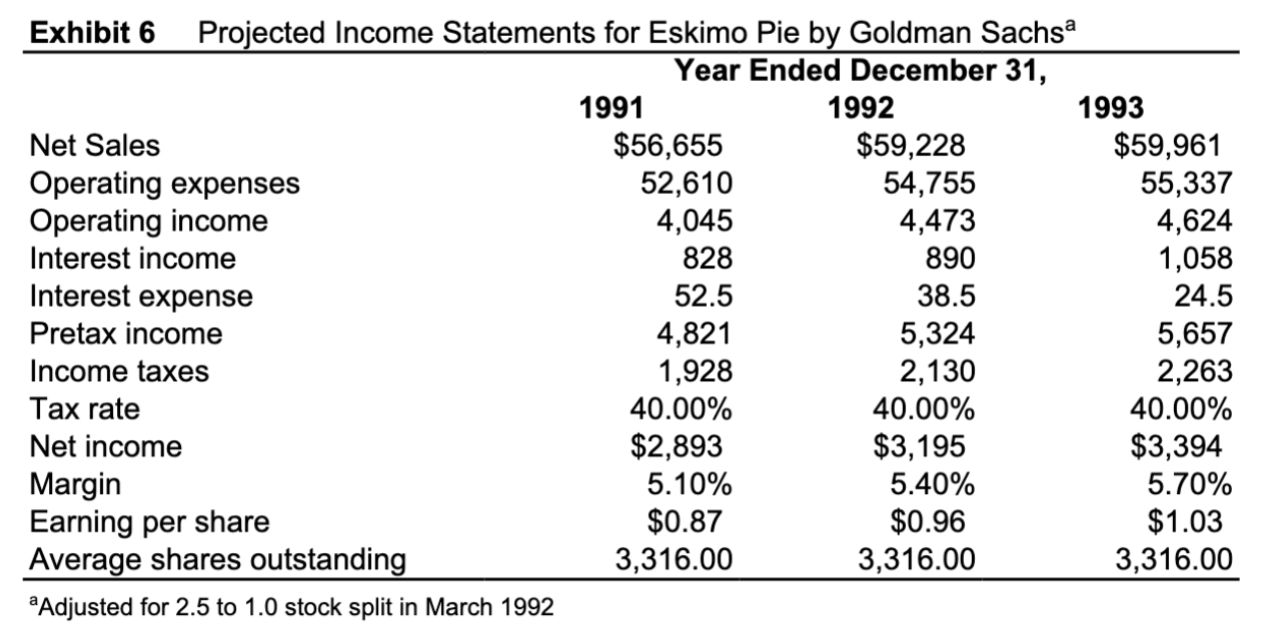

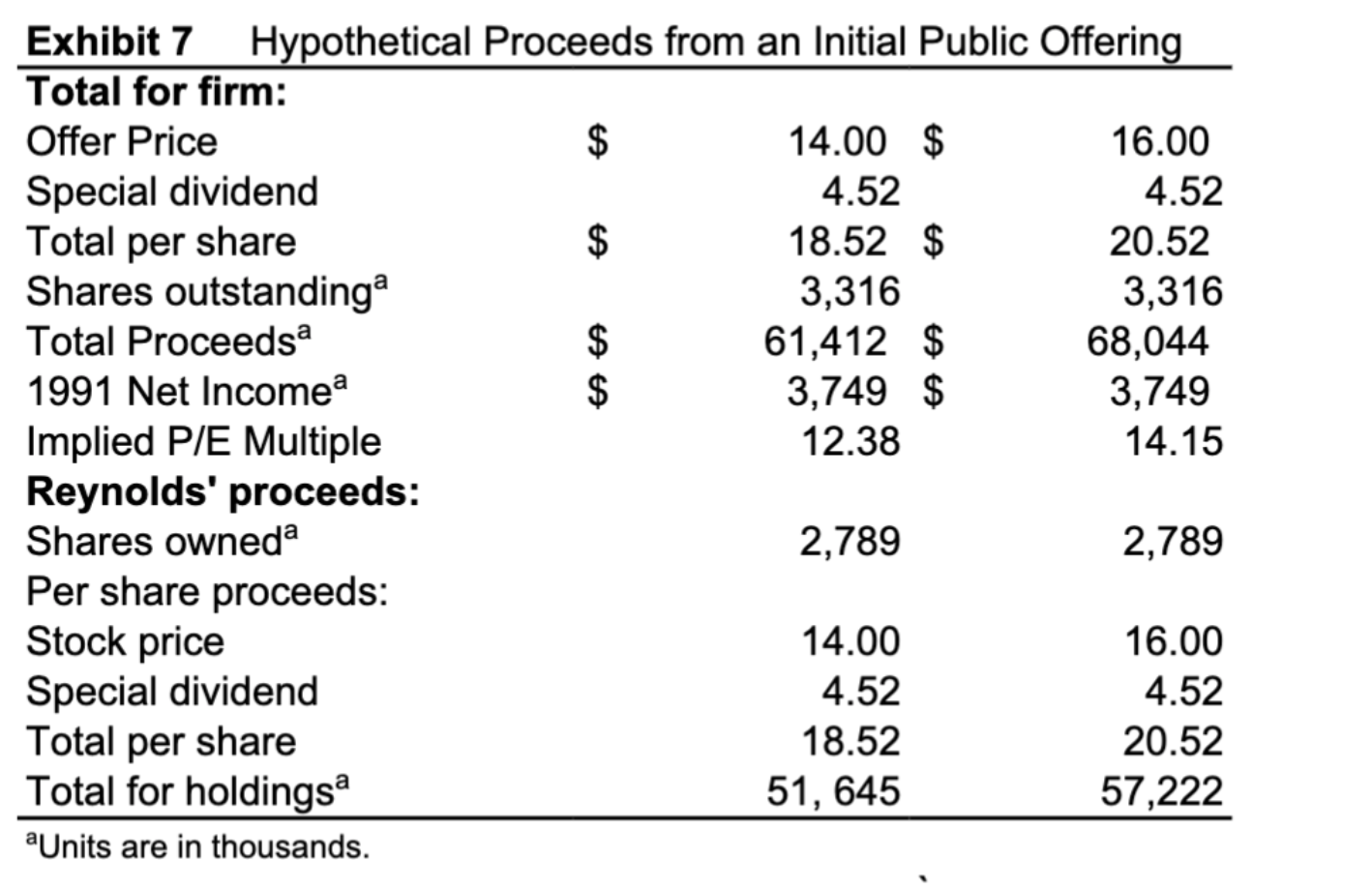

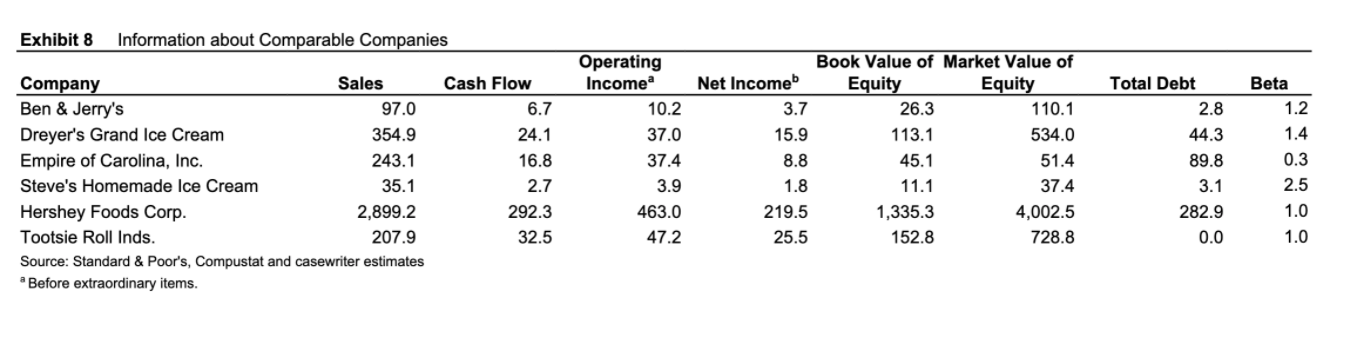

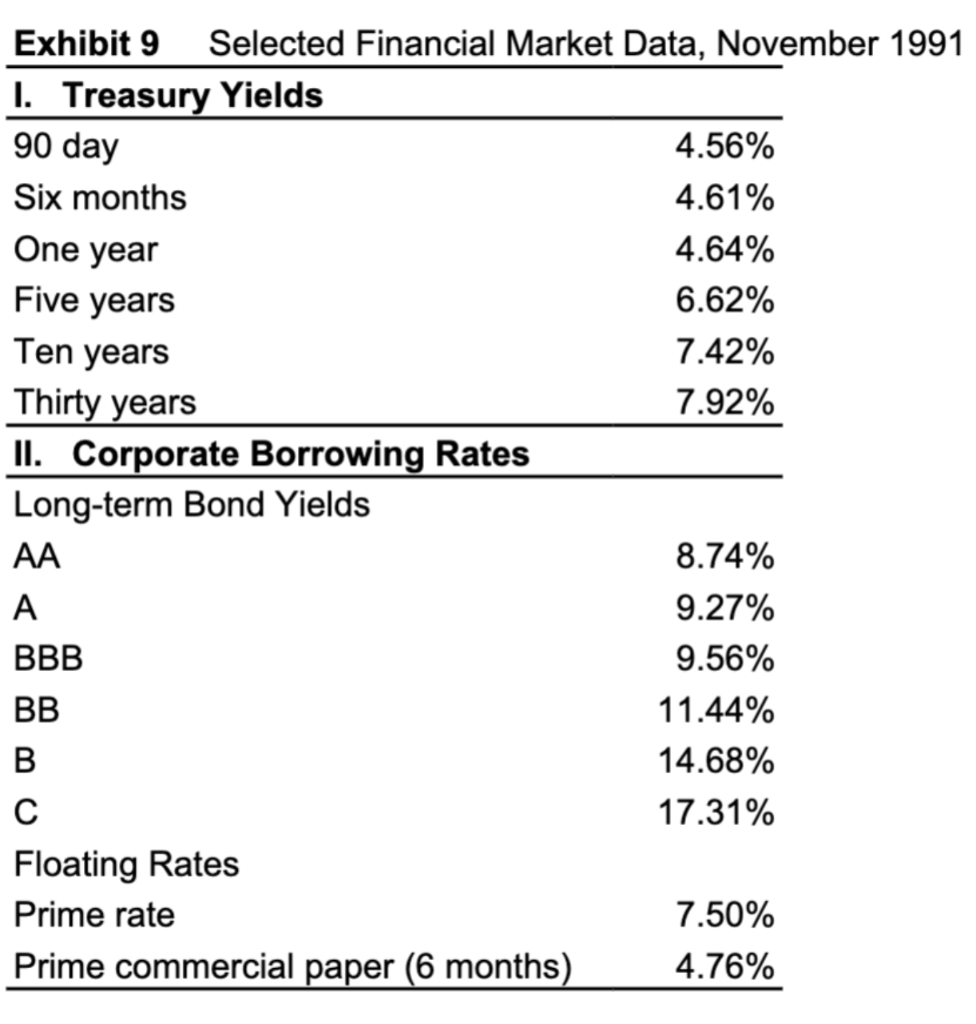

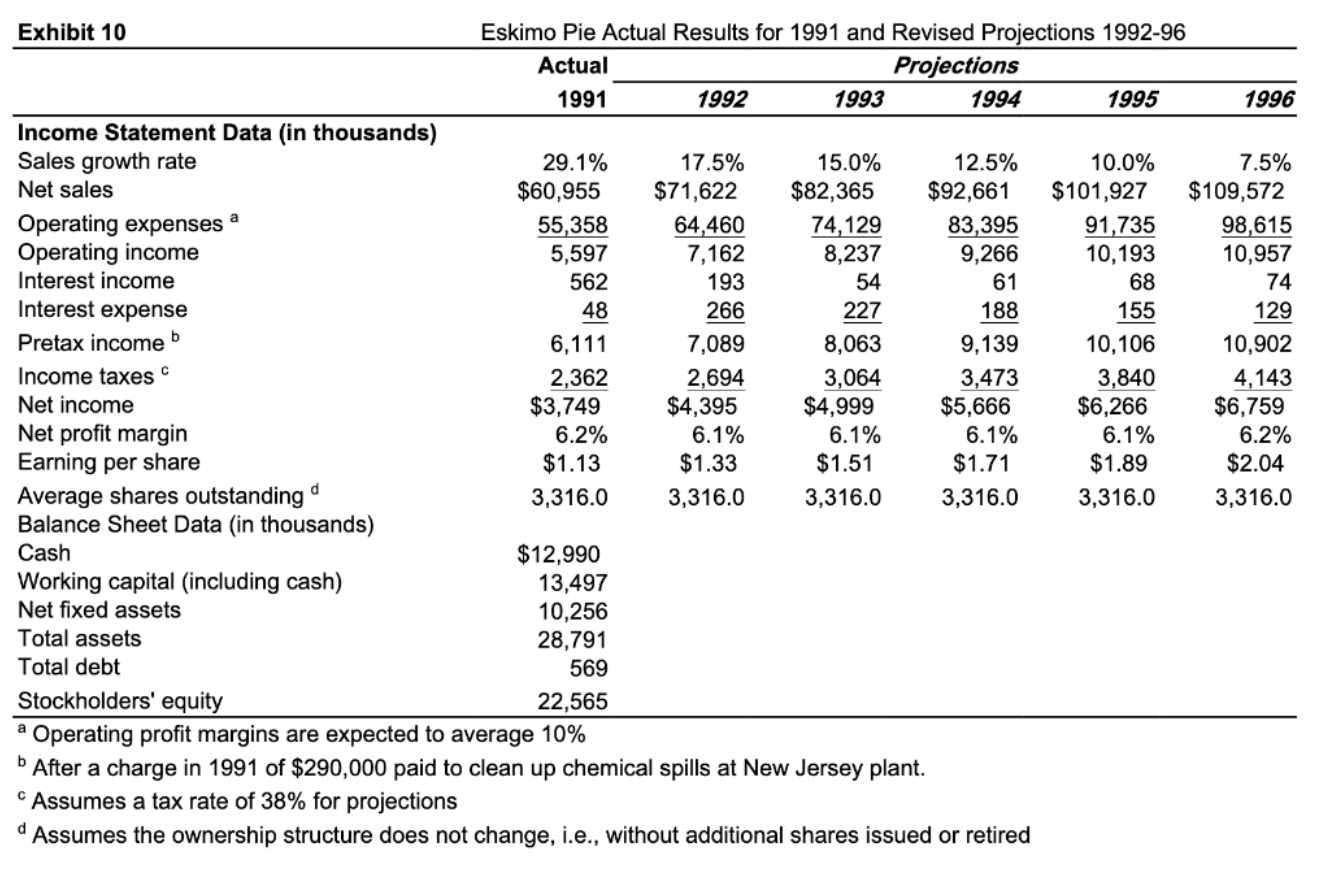

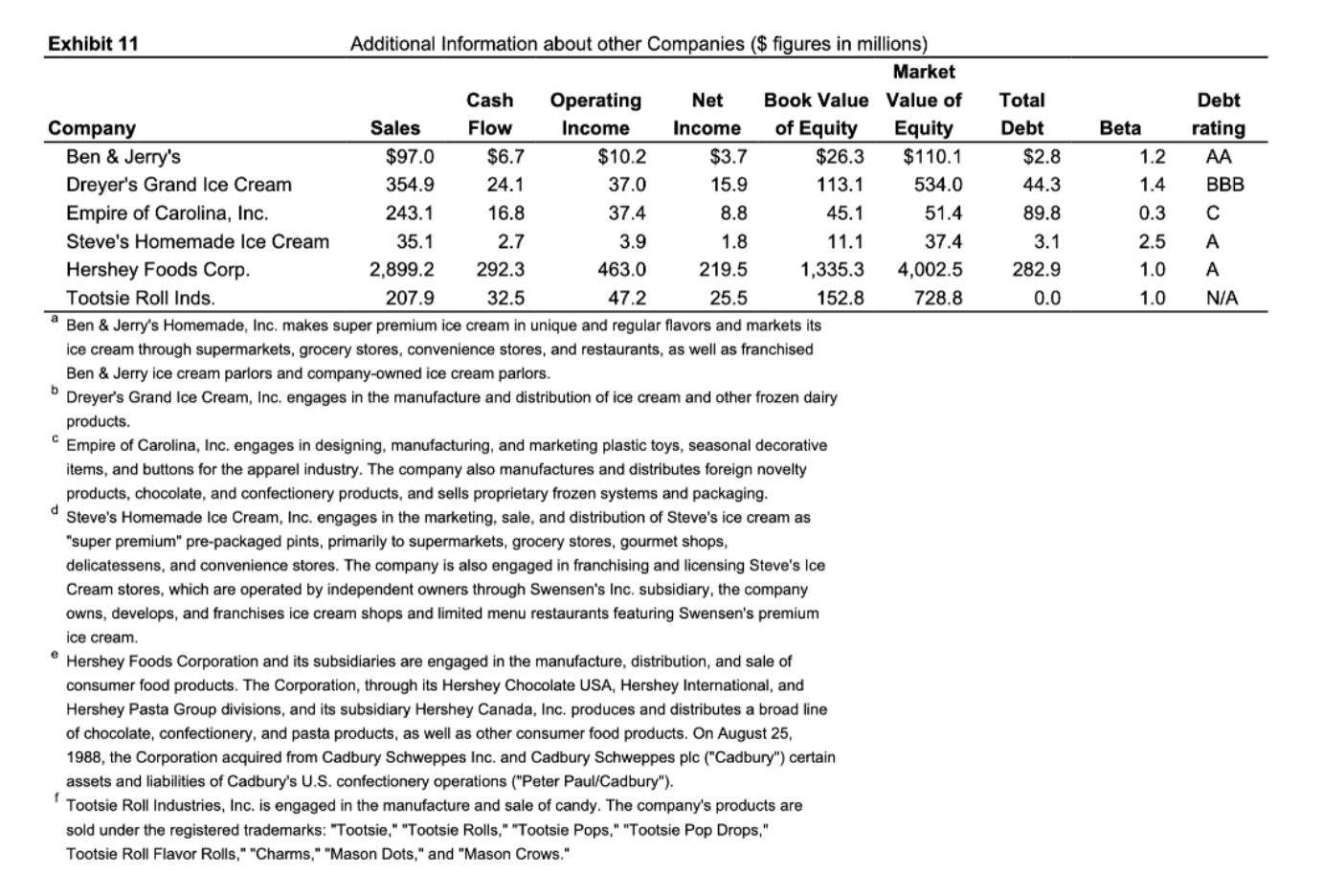

Eskimo Pie Corporation Full Firm Valuation: IPOs Instructions: This group case is due before 9:30am on Monday, November 23, 2020. Your group should upload a copy to Canvas via Assignments/Case 4 Submission. Each group is expected to provide solutions to all the questions except the discussion questions. Presenters are encouraged to include a concise case background at the beginning of their presentations. Case Update In January 1992, Eskimo Pie reported 1991 sales of $60,955,000 and net income of $3,749,000. Based on this record performance, David Clark was hopeful that he could convince Reynolds executives that an IPO of their company's shares of Eskimo Pie stock was more attractive than a sale of the company to Nestle. Reynolds executives imposed several conditions before they would entertain a revised proposal. 1. The cash dividend of $4.52 per share to existing shareholders would be paid from the excess cash balances Eskimo Pie had accumulated and from additional borrowing prior to the IPO. The new borrowing would be required in order to assure that Eskimo Pies operating cash balances were no less than 1% of annual sales, the minimum target balance. Once the offering had been completed, Eskimo Pie management could make further changes in the capital structure to achieve whatever targets they deemed appropriate. 2. The IPO would be restricted to the sale of the shares already outstanding and would not permit the Greenshoe Clause which would have allowed Eskimo Pie the option to offer additional, newly created shares. Thus, the offering would be restricted to the 3,316,000 shares that were currently outstanding. Any shareholder would have the right to sell his or her shares as part of the IPO or to continue to hold those shares after the IPO when the shares could be traded in more liquid, public capital markets. Reynolds would agree to sell all of its shares as would the Reynolds Foundation, guaranteeing that at least 88% of the shares would be placed in the hands of the public. 3. Clark and the bankers from Wheat First would have to present their financial estimates to the Reynolds board who would, in turn, decide between the IPO and the sale to Nestle on the basis of which alternative would provide them with the most cash for their shares. 4. Preliminary discussions with Nestle indicated that the $61 million offer for the Eskimo Pie shares was firm despite the record profit and sales achieved in 1991. (Nestle officials claimed their own internal valuation had anticipated the improvements irrespective of the Goldman Sachs analysis.) The offer of $61 million for all Eskimo Pie shares was still on the table but would not be increased. No dividends or other distributions would be permitted prior to the closing of the sale. Assignment Assume the role of advisor to the Reynolds board. You are asked to value Eskimo Pie as a stand-alone firm as of the date of the IPO (i.e., standing at the end of 1991 valuing the estimated free cash flows starting in 1992 and onwards). Assume all cash flows occur at the end of each calendar year. Your free cash flow estimates should be based on the revised year- end results and estimates presented in Exhibit 10. (Note: Exhibits 10 and 11 have been added but are not in the original case. Exhibit 11 replicates most of Exhibit 8 and adds additional information.) . Valuation Assumptions Estimated sales growth rate for 1991-1996 are provided in Exhibit 10. After 1996, assume that sales are expected to grow at 5% into the foreseeable future. Assume that expected operating profit margin is 10%, but during adverse economic circumstances such as a recession, the firm's operating profit margin could be as low as 1% of sales. Project necessary cash at 1% of sales. Assume that working capital requirements (including necessary cash) are 2% of sales starting in 1992. Note that the level of working capital for 1991 shown in Ex. 10 contains all cash on the balance sheet. Net Fixed Assets (including net PP&E and related items) will grow by $250,000 between 1991 and 1992 and by the same amount between 1992 and 1993. (This number is the net amount over and above depreciation whereas the $1 million capital expenditure mentioned in the case is a gross figure). From 1993 to 1994 and onwards, Net Fixed Assets should be projected to grow in proportion to sales. Because you lack more detailed information, you must assume that the comps in Exhibit 11 do not have excess cash or other non-operating assets. The tax rate is 38% for the projections and for all companies in Exhibit 8 and Exhibit 11. You should completely ignore Exhibit 2 in conducting your valuation. Assume the market risk premium is 5%. Questions 1. Estimate the year-by-year free cash flows for the forecast period, 1992 through 1996. 2. Estimate the optimal capital structure for Eskimo. 3. Assume Eskimo's management will set the capital structure at the optimal level (i.e., the level you found in question 2). What is the appropriate WACC we should use to discount the FCFF? 4. Estimate the residual value using the perpetuity with growth and the competitive markets assumptions. 5. Complete the valuation of Eskimo Pie as of the IPO date (i.e. straight after the $4.52 per share dividend is paid and any borrowing required to pay this dividend had occurred). Estimate the likely price per share at which Wheat First could expect to offer the stock of Eskimo Pie to the public (ignore any flotation costs and the Greenshoe option). 6. Based on your valuation, should Reynolds' approve the IPO or should it complete the sale to Nestle? Explain. Table B 1991 Leading Frozen Novelty Brands Brand Company Unit Share Popsicle Unilever 7.6% Klondike Empire of Carolina 5.4% Eskimo Pie Eskimo Pie 5.3% Snickers Mars 4.8% Weight Watchers H.J. Heinz 4.3% Exhibit 1 Historical Financial Information Year Ended December 31, 1987 1988 1989 1990 Income Statement Data (in thousands): Net salesa $ 30,769 $ 36,695 $ 46,709 $ 47,198 Cost of goods sold 21,650 25,635 31,957 31,780 Gross profite 9,119 11,060 14,752 15,418 Advertising and sales promotions 4,742 4,241 5,030 5,130 General and administrative 6,068 5,403 6,394 7,063 Operating income (loss) (1,691) 1,416 3,328 3,225 Interest income 308 550 801 1,004 Interest expense (88) (107) (88) (67) Other income (expense)-net 1,738 (77) (108) (20) Income taxes 96 729 1,511 1,616 Net income $ 171 $ 1,053 $ 2,422 $ 2,526 Balance Sheet Data (in thousands): Cash 5,550 $ 8,109 $ 10,723 $ 13,191 Working capital 9,342 11,107 10,830 11,735 Total assets 20,857 23,006 26,159 29,518 Long-term debt 1,269 1,094 919 744 Stockholders' equity 16,162 17,215 18,215 19,496 Per Share Data: Weighted average number of common shares outstanding 3,316 3,316 3,316 3,316 Net income per share $ 0.05 $ 0.32 $ 0.73 $ 0.76 Cash dividend per share $ 0.40 $ 0.40 aBeginning in 1991 the Company increased prices for products and assumed responsibility for advertising and sales promotion costs previously shared with licensees. This change in business practice accounts for approximately one-half of the increase in net sales for 1991 with a similar impact on 1991 gross profit. bincludes the gain on sale of building of approximately $1,700,000 in 1987. Exhibit 3 Distribution and Market Share of Eskimo Pie, Heath, and Welch's Frozen Novelties 1987 1988 1989 1990 1991 Distribution of at least one Eskimo product at U.S. Grocery Stores 76.3% 78.1% 91.2% 95.6% 97.9% Unit Market Share of Eskimo products 3.3 3.9 6.8 7.5 5.7 Exhibit 4 Industry Information for Frozen Novelties Industry Units Revenues Sold % Change Year (millions) (millions) in Sales 1980 $590 NA 1981 680 N/A 15.3% 1982 770 457 13.2 1983 940 525 22.1 1984 1,100 577 17.0 1985 1,300 643 18.2 1986 1,400 681 7.7 1987 1,500 717 7.1 1988 1,355 637 -9.7 1989 1,332 623 -1.7 1990 1,321 590 -0.8 Average Price N/A N/A $1.69 1.79 1.90 2.02 2.06 2.09 2.13 2.19 2.24 Advertising Spending (millions) $2 4 17 23 32 44 77 38 26 40 21 Exhibit 6 Projected Income Statements for Eskimo Pie by Goldman Sachsa Year Ended December 31, 1991 1992 1993 Net Sales $56,655 $59,228 $59,961 Operating expenses 52,610 54,755 55,337 Operating income 4,045 4,473 4,624 Interest income 828 890 1,058 Interest expense 52.5 38.5 24.5 Pretax income 4,821 5,324 5,657 Income taxes 1,928 2,130 2,263 Tax rate 40.00% 40.00% 40.00% Net income $2,893 $3,195 $3,394 Margin 5.10% 5.40% 5.70% Earning per share $0.87 $0.96 $1.03 Average shares outstanding 3,316.00 3,316.00 3,316.00 Adjusted for 2.5 to 1.0 stock split in March 1992 $ Exhibit 7 Hypothetical Proceeds from an Initial Public Offering Total for firm: Offer Price $ 14.00 $ 16.00 Special dividend 4.52 4.52 Total per share 18.52 $ 20.52 Shares outstandinga 3,316 3,316 Total Proceedsa 61,412 $ 68,044 1991 Net Incomea $ 3,749 $ 3,749 Implied P/E Multiple 12.38 14.15 Reynolds' proceeds: Shares owneda 2,789 2,789 Per share proceeds: Stock price 14.00 16.00 Special dividend 4.52 4.52 Total per share 18.52 20.52 Total for holdings 51, 645 57,222 aUnits are in thousands. Exhibit 8 Information about Comparable Companies Company Sales Ben & Jerry's 97.0 Dreyer's Grand Ice Cream 354.9 Empire of Carolina, Inc. 243.1 Steve's Homemade Ice Cream 35.1 Hershey Foods Corp. 2,899.2 Tootsie Roll Inds. 207.9 Source: Standard & Poor's, Compustat and casewriter estimates Before extraordinary items. Cash Flow 6.7 24.1 16.8 2.7 292.3 32.5 Operating Incomea 10.2 37.0 37.4 3.9 463.0 47.2 Book Value of Market Value of Net Income Equity Equity 3.7 26.3 110.1 15.9 113.1 534.0 8.8 45.1 51.4 1.8 11.1 37.4 219.5 1,335.3 4,002.5 25.5 152.8 728.8 Total Debt 2.8 44.3 89.8 3.1 282.9 0.0 Beta 1.2 1.4 0.3 2.5 1.0 1.0 Exhibit 9 Selected Financial Market Data, November 1991 I. Treasury Yields 90 day 4.56% Six months 4.61% One year 4.64% Five years 6.62% Ten years 7.42% Thirty years 7.92% II. Corporate Borrowing Rates Long-term Bond Yields AA 8.74% A 9.27% BBB 9.56% BB 11.44% B 14.68% 17.31% Floating Rates Prime rate 7.50% Prime commercial paper (6 months) 4.76% Exhibit 10 Eskimo Pie Actual Results for 1991 and Revised Projections 1992-96 Actual Projections 1991 1992 1993 1994 1995 1996 Income Statement Data (in thousands) Sales growth rate 29.1% 17.5% 15.0% 12.5% 10.0% 7.5% Net sales $60,955 $71,622 $82,365 $92,661 $101,927 $109,572 Operating expenses 55,358 64,460 74,129 83,395 91,735 98,615 Operating income 5,597 7,162 8,237 9,266 10,193 10,957 Interest income 562 193 54 61 68 74 Interest expense 48 266 227 188 155 129 Pretax income b 6,111 7,089 8,063 9,139 10,106 10,902 Income taxes 2,362 2,694 3,064 3,473 3,840 4,143 Net income $3,749 $4,395 $4,999 $5,666 $6,266 $6,759 Net profit margin 6.2% 6.1% 6.1% 6.1% 6.1% 6.2% Earning per share $1.13 $1.33 $1.51 $1.71 $1.89 $2.04 Average shares outstanding a 3,316.0 3,316.0 3,316.0 3,316.0 3,316.0 3,316.0 Balance Sheet Data (in thousands) Cash $12,990 Working capital (including cash) 13,497 Net fixed assets 10,256 Total assets 28,791 Total debt 569 Stockholders' equity 22,565 a Operating profit margins are expected to average 10% After a charge in 1991 of $290,000 paid to clean up chemical spills at New Jersey plant. Assumes a tax rate of 38% for projections d Assumes the ownership structure does not change, i.e., without additional shares issued or retired b Beta Debt rating AA BBB Total Debt $2.8 44.3 89.8 3.1 282.9 0.0 1.2 1.4 0.3 2.5 1.0 1.0 N/A Exhibit 11 Additional Information about other Companies ($ figures in millions) Market Cash Operating Net Book Value Value of Company Sales Flow Income Income of Equity Equity Ben & Jerry's $97.0 $6.7 $10.2 $3.7 $26.3 $110.1 Dreyer's Grand Ice Cream 354.9 24.1 37.0 15.9 113.1 534.0 Empire of Carolina, Inc. 243.1 16.8 37.4 8.8 45.1 51.4 Steve's Homemade Ice Cream 35.1 2.7 3.9 1.8 11.1 37.4 Hershey Foods Corp. 2,899.2 292.3 463.0 219.5 1,335.3 4,002.5 Tootsie Roll Inds. 207.9 32.5 47.2 25.5 152.8 728.8 Ben & Jerry's Homemade, Inc. makes super premium ice cream in unique and regular flavors and markets its ice cream through supermarkets, grocery stores, convenience stores, and restaurants, as well as franchised Ben & Jerry ice cream parlors and company-owned ice cream parlors. Dreyer's Grand Ice Cream, Inc. engages in the manufacture and distribution of ice cream and other frozen dairy products. Empire of Carolina, Inc. engages in designing, manufacturing, and marketing plastic toys, seasonal decorative items, and buttons for the apparel industry. The company also manufactures and distributes foreign novelty products, chocolate, and confectionery products, and sells proprietary frozen systems and packaging. d Steve's Homemade Ice Cream, Inc. engages in the marketing, sale, and distribution of Steve's ice cream as "super premium" pre-packaged pints, primarily to supermarkets, grocery stores, gourmet shops, delicatessens, and convenience stores. The company is also engaged in franchising and licensing Steve's Ice Cream stores, which are operated by independent owners through Swensen's Inc. subsidiary, the company owns, develops, and franchises ice cream shops and limited menu restaurants featuring Swensen's premium ice cream Hershey Foods Corporation and its subsidiaries are engaged in the manufacture, distribution, and sale of consumer food products. The Corporation, through its Hershey Chocolate USA, Hershey International, and Hershey Pasta Group divisions, and its subsidiary Hershey Canada, Inc. produces and distributes a broad line of chocolate, confectionery, and pasta products, as well as other consumer food products. On August 25, 1988, the Corporation acquired from Cadbury Schweppes Inc. and Cadbury Schweppes plc ("Cadbury") certain assets and liabilities of Cadbury's U.S. confectionery operations ("Peter Paul/Cadbury"). Tootsie Roll Industries, Inc. is engaged in the manufacture and sale of candy. The company's products are sold under the registered trademarks: "Tootsie," "Tootsie Rolls," "Tootsie Pops," "Tootsie Pop Drops," Tootsie Roll Flavor Rolls," "Charms," "Mason Dots," and "Mason Crows." Eskimo Pie Corporation Full Firm Valuation: IPOs Instructions: This group case is due before 9:30am on Monday, November 23, 2020. Your group should upload a copy to Canvas via Assignments/Case 4 Submission. Each group is expected to provide solutions to all the questions except the discussion questions. Presenters are encouraged to include a concise case background at the beginning of their presentations. Case Update In January 1992, Eskimo Pie reported 1991 sales of $60,955,000 and net income of $3,749,000. Based on this record performance, David Clark was hopeful that he could convince Reynolds executives that an IPO of their company's shares of Eskimo Pie stock was more attractive than a sale of the company to Nestle. Reynolds executives imposed several conditions before they would entertain a revised proposal. 1. The cash dividend of $4.52 per share to existing shareholders would be paid from the excess cash balances Eskimo Pie had accumulated and from additional borrowing prior to the IPO. The new borrowing would be required in order to assure that Eskimo Pies operating cash balances were no less than 1% of annual sales, the minimum target balance. Once the offering had been completed, Eskimo Pie management could make further changes in the capital structure to achieve whatever targets they deemed appropriate. 2. The IPO would be restricted to the sale of the shares already outstanding and would not permit the Greenshoe Clause which would have allowed Eskimo Pie the option to offer additional, newly created shares. Thus, the offering would be restricted to the 3,316,000 shares that were currently outstanding. Any shareholder would have the right to sell his or her shares as part of the IPO or to continue to hold those shares after the IPO when the shares could be traded in more liquid, public capital markets. Reynolds would agree to sell all of its shares as would the Reynolds Foundation, guaranteeing that at least 88% of the shares would be placed in the hands of the public. 3. Clark and the bankers from Wheat First would have to present their financial estimates to the Reynolds board who would, in turn, decide between the IPO and the sale to Nestle on the basis of which alternative would provide them with the most cash for their shares. 4. Preliminary discussions with Nestle indicated that the $61 million offer for the Eskimo Pie shares was firm despite the record profit and sales achieved in 1991. (Nestle officials claimed their own internal valuation had anticipated the improvements irrespective of the Goldman Sachs analysis.) The offer of $61 million for all Eskimo Pie shares was still on the table but would not be increased. No dividends or other distributions would be permitted prior to the closing of the sale. Assignment Assume the role of advisor to the Reynolds board. You are asked to value Eskimo Pie as a stand-alone firm as of the date of the IPO (i.e., standing at the end of 1991 valuing the estimated free cash flows starting in 1992 and onwards). Assume all cash flows occur at the end of each calendar year. Your free cash flow estimates should be based on the revised year- end results and estimates presented in Exhibit 10. (Note: Exhibits 10 and 11 have been added but are not in the original case. Exhibit 11 replicates most of Exhibit 8 and adds additional information.) . Valuation Assumptions Estimated sales growth rate for 1991-1996 are provided in Exhibit 10. After 1996, assume that sales are expected to grow at 5% into the foreseeable future. Assume that expected operating profit margin is 10%, but during adverse economic circumstances such as a recession, the firm's operating profit margin could be as low as 1% of sales. Project necessary cash at 1% of sales. Assume that working capital requirements (including necessary cash) are 2% of sales starting in 1992. Note that the level of working capital for 1991 shown in Ex. 10 contains all cash on the balance sheet. Net Fixed Assets (including net PP&E and related items) will grow by $250,000 between 1991 and 1992 and by the same amount between 1992 and 1993. (This number is the net amount over and above depreciation whereas the $1 million capital expenditure mentioned in the case is a gross figure). From 1993 to 1994 and onwards, Net Fixed Assets should be projected to grow in proportion to sales. Because you lack more detailed information, you must assume that the comps in Exhibit 11 do not have excess cash or other non-operating assets. The tax rate is 38% for the projections and for all companies in Exhibit 8 and Exhibit 11. You should completely ignore Exhibit 2 in conducting your valuation. Assume the market risk premium is 5%. Questions 1. Estimate the year-by-year free cash flows for the forecast period, 1992 through 1996. 2. Estimate the optimal capital structure for Eskimo. 3. Assume Eskimo's management will set the capital structure at the optimal level (i.e., the level you found in question 2). What is the appropriate WACC we should use to discount the FCFF? 4. Estimate the residual value using the perpetuity with growth and the competitive markets assumptions. 5. Complete the valuation of Eskimo Pie as of the IPO date (i.e. straight after the $4.52 per share dividend is paid and any borrowing required to pay this dividend had occurred). Estimate the likely price per share at which Wheat First could expect to offer the stock of Eskimo Pie to the public (ignore any flotation costs and the Greenshoe option). 6. Based on your valuation, should Reynolds' approve the IPO or should it complete the sale to Nestle? Explain. Table B 1991 Leading Frozen Novelty Brands Brand Company Unit Share Popsicle Unilever 7.6% Klondike Empire of Carolina 5.4% Eskimo Pie Eskimo Pie 5.3% Snickers Mars 4.8% Weight Watchers H.J. Heinz 4.3% Exhibit 1 Historical Financial Information Year Ended December 31, 1987 1988 1989 1990 Income Statement Data (in thousands): Net salesa $ 30,769 $ 36,695 $ 46,709 $ 47,198 Cost of goods sold 21,650 25,635 31,957 31,780 Gross profite 9,119 11,060 14,752 15,418 Advertising and sales promotions 4,742 4,241 5,030 5,130 General and administrative 6,068 5,403 6,394 7,063 Operating income (loss) (1,691) 1,416 3,328 3,225 Interest income 308 550 801 1,004 Interest expense (88) (107) (88) (67) Other income (expense)-net 1,738 (77) (108) (20) Income taxes 96 729 1,511 1,616 Net income $ 171 $ 1,053 $ 2,422 $ 2,526 Balance Sheet Data (in thousands): Cash 5,550 $ 8,109 $ 10,723 $ 13,191 Working capital 9,342 11,107 10,830 11,735 Total assets 20,857 23,006 26,159 29,518 Long-term debt 1,269 1,094 919 744 Stockholders' equity 16,162 17,215 18,215 19,496 Per Share Data: Weighted average number of common shares outstanding 3,316 3,316 3,316 3,316 Net income per share $ 0.05 $ 0.32 $ 0.73 $ 0.76 Cash dividend per share $ 0.40 $ 0.40 aBeginning in 1991 the Company increased prices for products and assumed responsibility for advertising and sales promotion costs previously shared with licensees. This change in business practice accounts for approximately one-half of the increase in net sales for 1991 with a similar impact on 1991 gross profit. bincludes the gain on sale of building of approximately $1,700,000 in 1987. Exhibit 3 Distribution and Market Share of Eskimo Pie, Heath, and Welch's Frozen Novelties 1987 1988 1989 1990 1991 Distribution of at least one Eskimo product at U.S. Grocery Stores 76.3% 78.1% 91.2% 95.6% 97.9% Unit Market Share of Eskimo products 3.3 3.9 6.8 7.5 5.7 Exhibit 4 Industry Information for Frozen Novelties Industry Units Revenues Sold % Change Year (millions) (millions) in Sales 1980 $590 NA 1981 680 N/A 15.3% 1982 770 457 13.2 1983 940 525 22.1 1984 1,100 577 17.0 1985 1,300 643 18.2 1986 1,400 681 7.7 1987 1,500 717 7.1 1988 1,355 637 -9.7 1989 1,332 623 -1.7 1990 1,321 590 -0.8 Average Price N/A N/A $1.69 1.79 1.90 2.02 2.06 2.09 2.13 2.19 2.24 Advertising Spending (millions) $2 4 17 23 32 44 77 38 26 40 21 Exhibit 6 Projected Income Statements for Eskimo Pie by Goldman Sachsa Year Ended December 31, 1991 1992 1993 Net Sales $56,655 $59,228 $59,961 Operating expenses 52,610 54,755 55,337 Operating income 4,045 4,473 4,624 Interest income 828 890 1,058 Interest expense 52.5 38.5 24.5 Pretax income 4,821 5,324 5,657 Income taxes 1,928 2,130 2,263 Tax rate 40.00% 40.00% 40.00% Net income $2,893 $3,195 $3,394 Margin 5.10% 5.40% 5.70% Earning per share $0.87 $0.96 $1.03 Average shares outstanding 3,316.00 3,316.00 3,316.00 Adjusted for 2.5 to 1.0 stock split in March 1992 $ Exhibit 7 Hypothetical Proceeds from an Initial Public Offering Total for firm: Offer Price $ 14.00 $ 16.00 Special dividend 4.52 4.52 Total per share 18.52 $ 20.52 Shares outstandinga 3,316 3,316 Total Proceedsa 61,412 $ 68,044 1991 Net Incomea $ 3,749 $ 3,749 Implied P/E Multiple 12.38 14.15 Reynolds' proceeds: Shares owneda 2,789 2,789 Per share proceeds: Stock price 14.00 16.00 Special dividend 4.52 4.52 Total per share 18.52 20.52 Total for holdings 51, 645 57,222 aUnits are in thousands. Exhibit 8 Information about Comparable Companies Company Sales Ben & Jerry's 97.0 Dreyer's Grand Ice Cream 354.9 Empire of Carolina, Inc. 243.1 Steve's Homemade Ice Cream 35.1 Hershey Foods Corp. 2,899.2 Tootsie Roll Inds. 207.9 Source: Standard & Poor's, Compustat and casewriter estimates Before extraordinary items. Cash Flow 6.7 24.1 16.8 2.7 292.3 32.5 Operating Incomea 10.2 37.0 37.4 3.9 463.0 47.2 Book Value of Market Value of Net Income Equity Equity 3.7 26.3 110.1 15.9 113.1 534.0 8.8 45.1 51.4 1.8 11.1 37.4 219.5 1,335.3 4,002.5 25.5 152.8 728.8 Total Debt 2.8 44.3 89.8 3.1 282.9 0.0 Beta 1.2 1.4 0.3 2.5 1.0 1.0 Exhibit 9 Selected Financial Market Data, November 1991 I. Treasury Yields 90 day 4.56% Six months 4.61% One year 4.64% Five years 6.62% Ten years 7.42% Thirty years 7.92% II. Corporate Borrowing Rates Long-term Bond Yields AA 8.74% A 9.27% BBB 9.56% BB 11.44% B 14.68% 17.31% Floating Rates Prime rate 7.50% Prime commercial paper (6 months) 4.76% Exhibit 10 Eskimo Pie Actual Results for 1991 and Revised Projections 1992-96 Actual Projections 1991 1992 1993 1994 1995 1996 Income Statement Data (in thousands) Sales growth rate 29.1% 17.5% 15.0% 12.5% 10.0% 7.5% Net sales $60,955 $71,622 $82,365 $92,661 $101,927 $109,572 Operating expenses 55,358 64,460 74,129 83,395 91,735 98,615 Operating income 5,597 7,162 8,237 9,266 10,193 10,957 Interest income 562 193 54 61 68 74 Interest expense 48 266 227 188 155 129 Pretax income b 6,111 7,089 8,063 9,139 10,106 10,902 Income taxes 2,362 2,694 3,064 3,473 3,840 4,143 Net income $3,749 $4,395 $4,999 $5,666 $6,266 $6,759 Net profit margin 6.2% 6.1% 6.1% 6.1% 6.1% 6.2% Earning per share $1.13 $1.33 $1.51 $1.71 $1.89 $2.04 Average shares outstanding a 3,316.0 3,316.0 3,316.0 3,316.0 3,316.0 3,316.0 Balance Sheet Data (in thousands) Cash $12,990 Working capital (including cash) 13,497 Net fixed assets 10,256 Total assets 28,791 Total debt 569 Stockholders' equity 22,565 a Operating profit margins are expected to average 10% After a charge in 1991 of $290,000 paid to clean up chemical spills at New Jersey plant. Assumes a tax rate of 38% for projections d Assumes the ownership structure does not change, i.e., without additional shares issued or retired b Beta Debt rating AA BBB Total Debt $2.8 44.3 89.8 3.1 282.9 0.0 1.2 1.4 0.3 2.5 1.0 1.0 N/A Exhibit 11 Additional Information about other Companies ($ figures in millions) Market Cash Operating Net Book Value Value of Company Sales Flow Income Income of Equity Equity Ben & Jerry's $97.0 $6.7 $10.2 $3.7 $26.3 $110.1 Dreyer's Grand Ice Cream 354.9 24.1 37.0 15.9 113.1 534.0 Empire of Carolina, Inc. 243.1 16.8 37.4 8.8 45.1 51.4 Steve's Homemade Ice Cream 35.1 2.7 3.9 1.8 11.1 37.4 Hershey Foods Corp. 2,899.2 292.3 463.0 219.5 1,335.3 4,002.5 Tootsie Roll Inds. 207.9 32.5 47.2 25.5 152.8 728.8 Ben & Jerry's Homemade, Inc. makes super premium ice cream in unique and regular flavors and markets its ice cream through supermarkets, grocery stores, convenience stores, and restaurants, as well as franchised Ben & Jerry ice cream parlors and company-owned ice cream parlors. Dreyer's Grand Ice Cream, Inc. engages in the manufacture and distribution of ice cream and other frozen dairy products. Empire of Carolina, Inc. engages in designing, manufacturing, and marketing plastic toys, seasonal decorative items, and buttons for the apparel industry. The company also manufactures and distributes foreign novelty products, chocolate, and confectionery products, and sells proprietary frozen systems and packaging. d Steve's Homemade Ice Cream, Inc. engages in the marketing, sale, and distribution of Steve's ice cream as "super premium" pre-packaged pints, primarily to supermarkets, grocery stores, gourmet shops, delicatessens, and convenience stores. The company is also engaged in franchising and licensing Steve's Ice Cream stores, which are operated by independent owners through Swensen's Inc. subsidiary, the company owns, develops, and franchises ice cream shops and limited menu restaurants featuring Swensen's premium ice cream Hershey Foods Corporation and its subsidiaries are engaged in the manufacture, distribution, and sale of consumer food products. The Corporation, through its Hershey Chocolate USA, Hershey International, and Hershey Pasta Group divisions, and its subsidiary Hershey Canada, Inc. produces and distributes a broad line of chocolate, confectionery, and pasta products, as well as other consumer food products. On August 25, 1988, the Corporation acquired from Cadbury Schweppes Inc. and Cadbury Schweppes plc ("Cadbury") certain assets and liabilities of Cadbury's U.S. confectionery operations ("Peter Paul/Cadbury"). Tootsie Roll Industries, Inc. is engaged in the manufacture and sale of candy. The company's products are sold under the registered trademarks: "Tootsie," "Tootsie Rolls," "Tootsie Pops," "Tootsie Pop Drops," Tootsie Roll Flavor Rolls," "Charms," "Mason Dots," and "Mason Crows