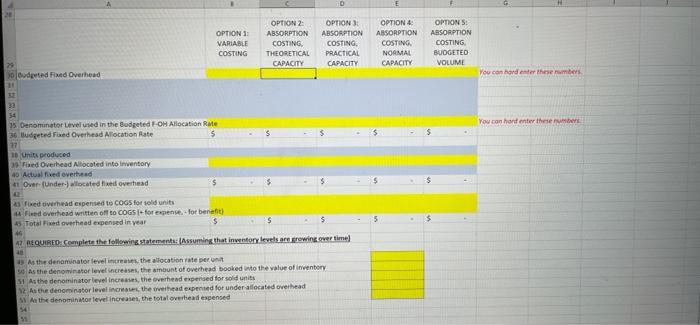

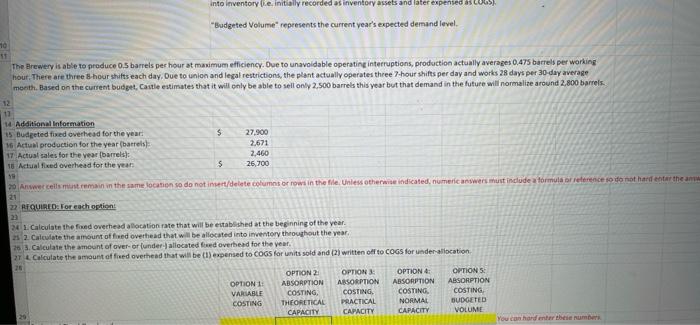

OPTION 1 VARIABLE COSTING OPTION 2: ABSORPTION COSTING THEORETICAL CAPACITY OPTION : ABSORPTION COSTING PRACTICAL CAPACITY OPTION: ABSORPTION COSTING NORMAL CAPACITY OPTIONS: ABSORPTION COSTING BUDGETED VOLUME 90 dpted Red Overhead You can handle these numbers 33 You can hand enter these $ 15 Denominator Level used in the Budgeted F-OH Allocation Rate 36 Budgeted Fed Overhead Allocation Rate 5 $ 27 1 Units produced 30 Pixed Overhead Allocated into Inventory 40 Actualid overhead 41 Over funder-) located at overhead fied overhead expensed to COGS for sold units Fedoverhead written off to COGS I for expense for benefit 45 Totale overhead expensed in year $ $ REQUIRED. Complete the following statement Assuming that inventory levels are growing over time) 5 $ 46 As the denominator level in the allocation rate per 50 As the denominator level increases the amount of overhead booked into the value of inventory S1 As the denominator level increases, the overhead expended for sold units 12 As the denominator level in the overhead expensed for under allocated overhead 31 Anthe denominato level increases, the total overhead expensed 51 into inventory le. Initially recorded as inventory assets and later expensed COGS "Budgeted Volume represents the current year's expected demand level 10 The Brewery is able to produce 0.5 barrels per hour at maximum efficiency. Due to unavoidable operating interruptions, production actually averages 0.475 barrels per working hour. There are three hour shifts each day. Due to union and legal restrictions, the plant actually operates three-hour shifts per day and works 28 days per 30 day average month. Based on the current budget, Castle estimates that it will only be able to sell only 2.500 barrels this year but that demand in the future will normalize around 2,800 barrels. $ 14 Additional Information 15 Budgeted fixed overhead for the year 16 Actual production for the year (barrels 17 Actual sales for the year (barrels 18 Actual fixed overhead for the years 27,900 2,671 2,460 26 700 5 20 Answer cells mit remain in the same location so do not insert/delete columns or rows in the file. Unless otherwise indicated, numeric answers must include a formula barreterence to do not harder the an 21 22 REQUIRED.Eoreach option 23 24. Calculate the foed overhead allocation rate that will be established at the beginning of the year 22. Calculate the amount offwed overhead that will be allocated into inventory throughout the year 26.3.Calculate the amount of overorlunder allocated feed overhead for the year. 2T L. Calculate the amount of fixed overhead that will be (1) expensed to COGS for units sold and (2) written off to COGS for under allocation OPTION 11 VARIABLE COSTING OPTION 2 ABSORPTION COSTING THEORETICAL CAPACITY OPTION : ABSORPTION COSTING PRACTICAL CAPACITY OPTION : ABSORPTION COSTING NORMAL CAPACITY OPTIONS ABSORPTION COSTING BUDGETED VOLUME You can hard enter the number OPTION 1 VARIABLE COSTING OPTION 2: ABSORPTION COSTING THEORETICAL CAPACITY OPTION : ABSORPTION COSTING PRACTICAL CAPACITY OPTION: ABSORPTION COSTING NORMAL CAPACITY OPTIONS: ABSORPTION COSTING BUDGETED VOLUME 90 dpted Red Overhead You can handle these numbers 33 You can hand enter these $ 15 Denominator Level used in the Budgeted F-OH Allocation Rate 36 Budgeted Fed Overhead Allocation Rate 5 $ 27 1 Units produced 30 Pixed Overhead Allocated into Inventory 40 Actualid overhead 41 Over funder-) located at overhead fied overhead expensed to COGS for sold units Fedoverhead written off to COGS I for expense for benefit 45 Totale overhead expensed in year $ $ REQUIRED. Complete the following statement Assuming that inventory levels are growing over time) 5 $ 46 As the denominator level in the allocation rate per 50 As the denominator level increases the amount of overhead booked into the value of inventory S1 As the denominator level increases, the overhead expended for sold units 12 As the denominator level in the overhead expensed for under allocated overhead 31 Anthe denominato level increases, the total overhead expensed 51 into inventory le. Initially recorded as inventory assets and later expensed COGS "Budgeted Volume represents the current year's expected demand level 10 The Brewery is able to produce 0.5 barrels per hour at maximum efficiency. Due to unavoidable operating interruptions, production actually averages 0.475 barrels per working hour. There are three hour shifts each day. Due to union and legal restrictions, the plant actually operates three-hour shifts per day and works 28 days per 30 day average month. Based on the current budget, Castle estimates that it will only be able to sell only 2.500 barrels this year but that demand in the future will normalize around 2,800 barrels. $ 14 Additional Information 15 Budgeted fixed overhead for the year 16 Actual production for the year (barrels 17 Actual sales for the year (barrels 18 Actual fixed overhead for the years 27,900 2,671 2,460 26 700 5 20 Answer cells mit remain in the same location so do not insert/delete columns or rows in the file. Unless otherwise indicated, numeric answers must include a formula barreterence to do not harder the an 21 22 REQUIRED.Eoreach option 23 24. Calculate the foed overhead allocation rate that will be established at the beginning of the year 22. Calculate the amount offwed overhead that will be allocated into inventory throughout the year 26.3.Calculate the amount of overorlunder allocated feed overhead for the year. 2T L. Calculate the amount of fixed overhead that will be (1) expensed to COGS for units sold and (2) written off to COGS for under allocation OPTION 11 VARIABLE COSTING OPTION 2 ABSORPTION COSTING THEORETICAL CAPACITY OPTION : ABSORPTION COSTING PRACTICAL CAPACITY OPTION : ABSORPTION COSTING NORMAL CAPACITY OPTIONS ABSORPTION COSTING BUDGETED VOLUME You can hard enter the number