Question

Options for blank #1 - and no bundled with a and a separate Options for blank #2 and a separate bundled with a and no

Options for blank #1 -

and no

bundled with a

and a separate

Options for blank #2

and a separate

bundled with a

and no

Options for blank #3

and no

and a separate

bundled with a

Options for blank #4

savings

pure insurance

Options for blank #5

savings

pure insurance

Options for blank #6

market-based

fixed

Options for blank #7

term

whole

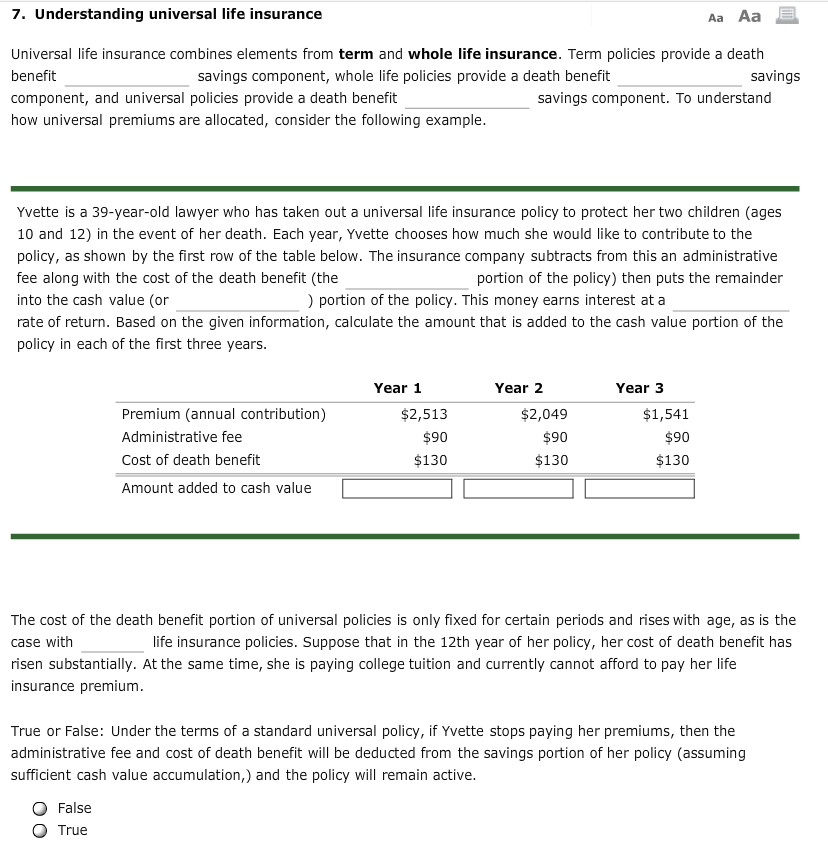

7. Understanding universal life insurance Aa Aa E Universal life insurance combines elements from term and whole life insurance. Term policies provide a death benefit savings component, whole life policies provide a death benefit savings component, and universal policies provide a death benefit savings component. To understand how universal premiums are allocated, consider the following example. Yvette is a 39-year-old lawyer who has taken out a universal life insurance policy to protect her two children (ages 10 and 12) in the event of her death. Each year, Yvette chooses how much she would like to contribute to the policy, as shown by the first row of the table below. The insurance company subtracts from this an administrative fee along with the cost of the death benefit (the portion of the policy) then puts the remainder into the cash value (or portion of the policy. This money earns interest at a rate of return. Based on the given information, calculate the amount that is added to the cash value portion of the policy in each of the first three years. Premium (annual contribution) Administrative fee Cost of death benefit Amount added to cash value Year 1 $2,513 $90 $130 Year 2 $2,049 $90 $130 Year 3 $1,541 $90 $130 The cost of the death benefit portion of universal policies is only fixed for certain periods and rises with age, as is the case with life insurance policies. Suppose that in the 12th year of her policy, her cost of death benefit has risen substantially. At the same time, she is paying college tuition and currently cannot afford to pay her life insurance premium. True or False: Under the terms of a standard universal policy, if Yvette stops paying her premiums, then the administrative fee and cost of death benefit will be deducted from the savings portion of her policy (assuming sufficient cash value accumulation, and the policy will remain active. False True O 7. Understanding universal life insurance Aa Aa E Universal life insurance combines elements from term and whole life insurance. Term policies provide a death benefit savings component, whole life policies provide a death benefit savings component, and universal policies provide a death benefit savings component. To understand how universal premiums are allocated, consider the following example. Yvette is a 39-year-old lawyer who has taken out a universal life insurance policy to protect her two children (ages 10 and 12) in the event of her death. Each year, Yvette chooses how much she would like to contribute to the policy, as shown by the first row of the table below. The insurance company subtracts from this an administrative fee along with the cost of the death benefit (the portion of the policy) then puts the remainder into the cash value (or portion of the policy. This money earns interest at a rate of return. Based on the given information, calculate the amount that is added to the cash value portion of the policy in each of the first three years. Premium (annual contribution) Administrative fee Cost of death benefit Amount added to cash value Year 1 $2,513 $90 $130 Year 2 $2,049 $90 $130 Year 3 $1,541 $90 $130 The cost of the death benefit portion of universal policies is only fixed for certain periods and rises with age, as is the case with life insurance policies. Suppose that in the 12th year of her policy, her cost of death benefit has risen substantially. At the same time, she is paying college tuition and currently cannot afford to pay her life insurance premium. True or False: Under the terms of a standard universal policy, if Yvette stops paying her premiums, then the administrative fee and cost of death benefit will be deducted from the savings portion of her policy (assuming sufficient cash value accumulation, and the policy will remain active. False True OStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Global Corporate Finance A Focused Approach

Authors: Kenneth Kim, Suk Kim

3rd Edition

9811207119, 9789811207112