Answered step by step

Verified Expert Solution

Question

1 Approved Answer

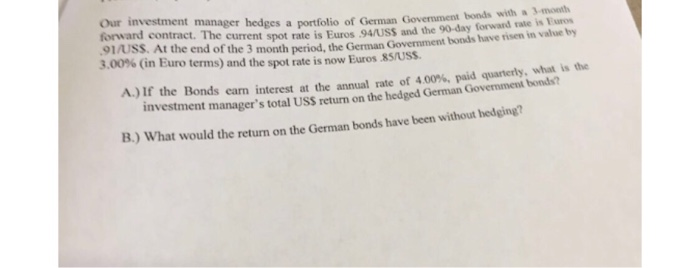

Our investment manager hedges a portfolio of German forward contract. The current Government bonds with a J.month spot rate is Euros 94/USs and the 90-day

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Brilliant Book Keeping How To Keep Your Business Efficient And Cost Effective

Authors: Martin Quinn

1st Edition

0273731785,0273746707