Question

Overview You are working for an investment bank and you are responsible for three high net worth clients. The first has a share portfolio valued

Overview

You are working for an investment bank and you are responsible for three high net worth clients. The first has a share portfolio valued at approximately $1,000,000 and is concerned that the share market might fall. The second client acts on behalf of a large Australian company which is looking to invest in a major project at the end of the year and is concerned that interest rates may rise. The third client works for a large Queensland manufacturing company whose major expense is electricity. This client is concerned about a rise in electricity prices.

Description Question 1 (6 Marks)

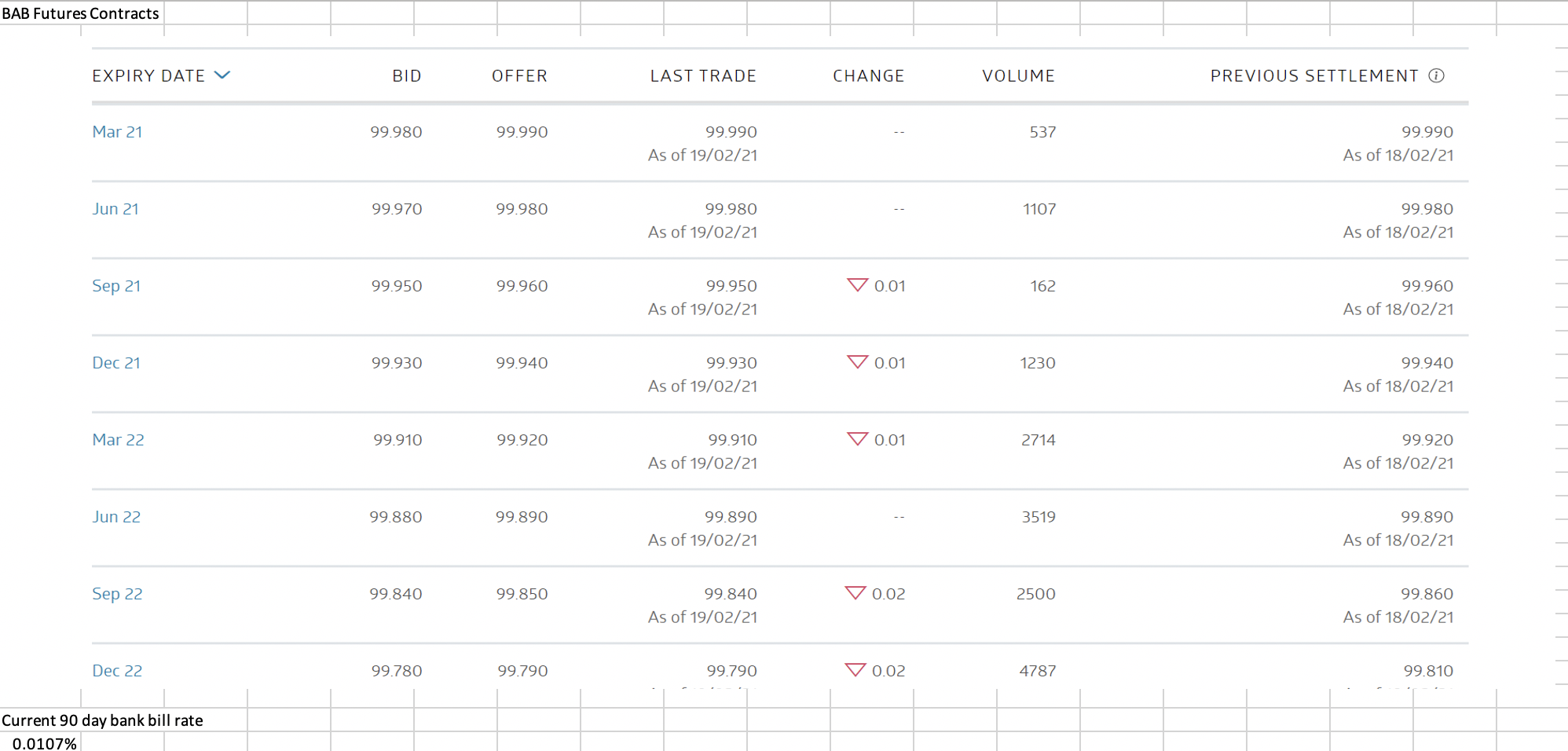

On January 1st, 2017, your first client established a portfolio with $1,000,000. They purchased the top 10 Australian shares at the time, giving them proportions according to the market capitalisation. They have recently become concerned about a potential market downturn over the next three months due to a mutated COVID strain and has asked you to set up a hedge for her using SPI200 futures contracts. The contract will be established today (19thFebruary 2021) and should be in place until at least May 19th, 2021.

Step 1 Determine the beta of the portfolio.

Data from Yahoo!Finance for the 10 shares in the portfolio as well as the combined portfolio and the ASX200 is provided in the Assignment_Part_A Data and Results.xlsx spreadsheet on Blackboard. Determine the beta of the portfolio.

Step 2 Choose an appropriate futures contract.

A snapshot of SPI200 futures prices as of February 19th is provided. Determine which contract should be chosen stating the day of expiry for the contract. Calculate the theoretical value for the contract, state all assumptions and provide the source of your assumptions. Discuss any differences between the theoretical value you have calculated and the listed value of the forward contract.

Step 3 Determine the number of futures contracts required.

Determine the initial value of the futures contract and the number of contracts that should be purchased to hedge this position. Be sure to state whether they should be buy or sell positions and hence whether you have used a bid or offer price.

Step 4 Provide the financial outcome for two (2) potential future scenarios.

Determine the financial outcome for your client assuming two different potential future outcomes: 1) an ending SPI200 price of 6000 and 2) an ending SPI200 price of 7500.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The China Model Experience And Challenges

Authors: Yongnian Zheng

1st Edition

1433172003, 1433190214, 9781433190216