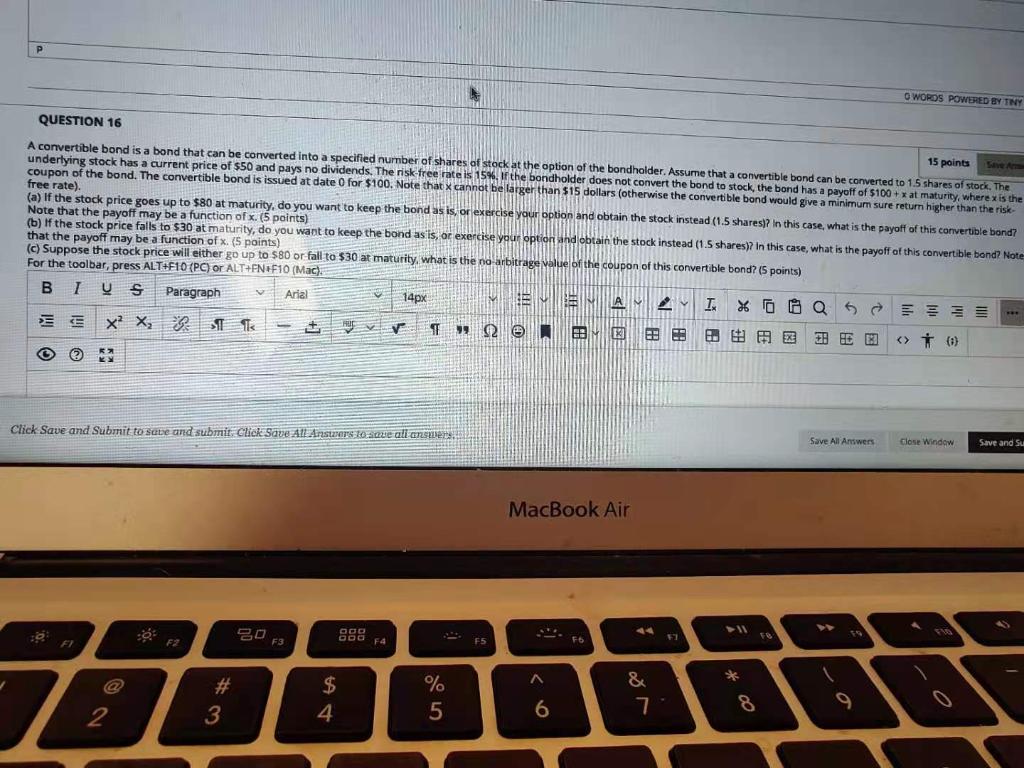

P O WORDS POWERED BY TINY QUESTION 16 15 points A convertible bond is a bond that can be converted into a specified number of shares of stock at the option of the bondholder. Assume that a convertible bond can be converted to 15 shares of stock. The underlying stock has a current price of $50 and pays no dividends. The risk-free rate is 15%. If the bondholder does not convert the bond to stock, the bond has a payoff of 5100 + x at maturity, where is the coupon of the bond. The convertible bond is issued at date 0 for $100. Note that cannot be larger than $15 dollars (otherwise the convertible bond would give a minimum sure return higher than the risk free rate) (a) If the stock price goes up to $80 at maturity, do you want to keep the bond as is, or exercise your option and obtain the stock instead (1.5 shares in this case, what is the payoff of this convertible band? Note that the payoff may be a function of x. (5 points) (b) If the stock price falls to $30 at maturity, do you want to keep the bond as is, or exercise your option and obtain the stock instead (1.5 shares)? In this case, what is the payoff of this convertible band? Note that the payoff may be a function of x. (5 points) (c) Suppose the stock price will either go up to $80 or fall to $30 at maturity, what is the no arbitrage value of the coupon of this convertible bond? (5 points) For the toolbar, press ALT+F10 (PC) or ALT+FN+F10 (Mac). BI y s Paragraph Arial 14px MIAM AMIZI % OH Q Q5 x? X v T 12 e BE 3 ! E ( * ) Click Save and Submit to see and submit Click Save All Artes e ali answer Save All Answers Close Window Save and su MacBook Air RO F3 QOD OOO 57 F4 F5 F6 A t $ # 3 % 5 & 7 9 2 4 8 6 P O WORDS POWERED BY TINY QUESTION 16 15 points A convertible bond is a bond that can be converted into a specified number of shares of stock at the option of the bondholder. Assume that a convertible bond can be converted to 15 shares of stock. The underlying stock has a current price of $50 and pays no dividends. The risk-free rate is 15%. If the bondholder does not convert the bond to stock, the bond has a payoff of 5100 + x at maturity, where is the coupon of the bond. The convertible bond is issued at date 0 for $100. Note that cannot be larger than $15 dollars (otherwise the convertible bond would give a minimum sure return higher than the risk free rate) (a) If the stock price goes up to $80 at maturity, do you want to keep the bond as is, or exercise your option and obtain the stock instead (1.5 shares in this case, what is the payoff of this convertible band? Note that the payoff may be a function of x. (5 points) (b) If the stock price falls to $30 at maturity, do you want to keep the bond as is, or exercise your option and obtain the stock instead (1.5 shares)? In this case, what is the payoff of this convertible band? Note that the payoff may be a function of x. (5 points) (c) Suppose the stock price will either go up to $80 or fall to $30 at maturity, what is the no arbitrage value of the coupon of this convertible bond? (5 points) For the toolbar, press ALT+F10 (PC) or ALT+FN+F10 (Mac). BI y s Paragraph Arial 14px MIAM AMIZI % OH Q Q5 x? X v T 12 e BE 3 ! E ( * ) Click Save and Submit to see and submit Click Save All Artes e ali answer Save All Answers Close Window Save and su MacBook Air RO F3 QOD OOO 57 F4 F5 F6 A t $ # 3 % 5 & 7 9 2 4 8 6