Answered step by step

Verified Expert Solution

Question

1 Approved Answer

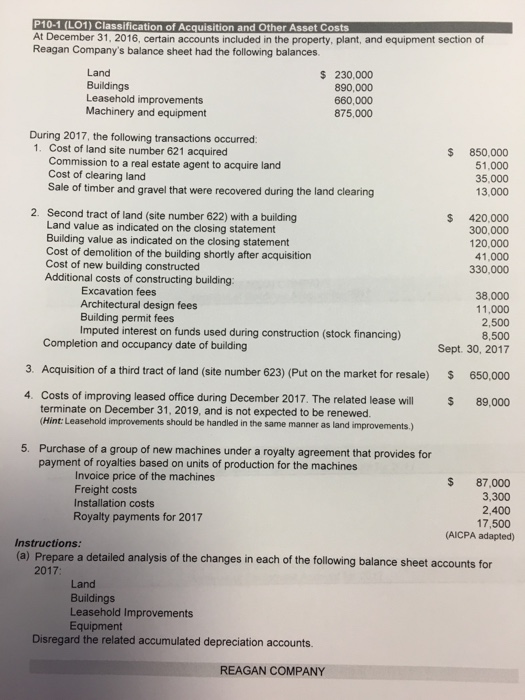

P10-1 (L01) Classification of Acquisition and Other Asset Costs At December 31, 2016, certain accounts included in the property, plant, and equipment section of Reagan

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Environmental Responsibility Accounting And Corporate Finance In The EU

Authors: Panagiotis Dimitropoulos, Konstantinos Koronios

1st Edition

3030727726, 9783030727727