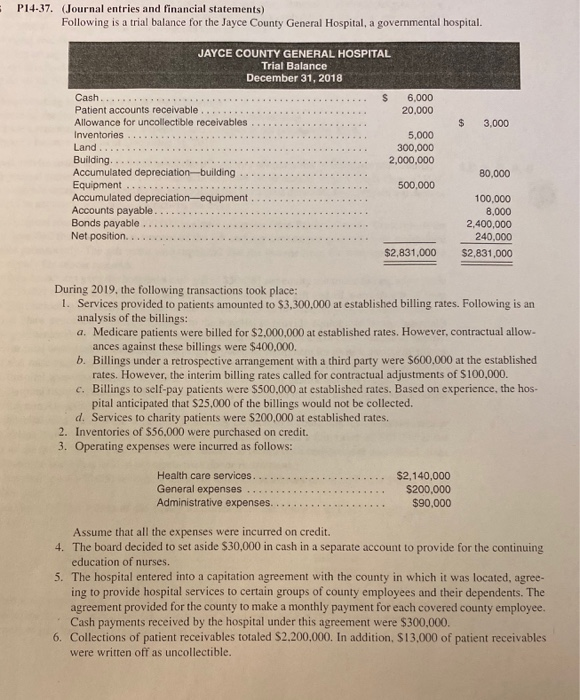

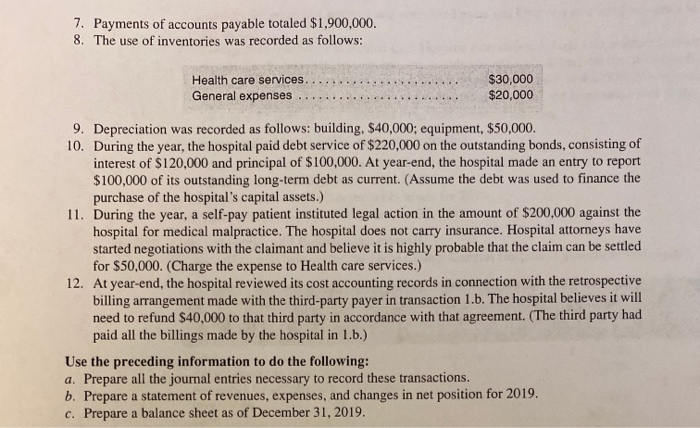

: P14-37. (Journal entries and financial statements) Following is a trial balance for the Jayce County General Hospital, a governmental hospital. JAYCE COUNTY GENERAL HOSPITAL Trial Balance December 31, 2018 $ 6,000 20.000 $ 3,000 5,000 300,000 2,000,000 Cash Patient accounts receivable.. Allowance for uncollectible receivables.. Inventories.. Land... Building....... . Accumulated depreciation-building Equipment Accumulated depreciation-equipment Accounts payable..... Bonds payable .... Net position........... 80,000 500,000 100,000 8.000 2,400,000 240,000 $2,831,000 $2,831,000 During 2019. the following transactions took place: 1. Services provided to patients amounted to $3,300.000 at established billing rates. Following is an analysis of the billings: a. Medicare patients were billed for $2,000,000 at established rates. However, contractual allow ances against these billings were $400,000. b. Billings under a retrospective arrangement with a third party were $600.000 at the established rates. However, the interim billing rates called for contractual adjustments of $100,000. c. Billings to self-pay patients were $500,000 at established rates. Based on experience, the hos pital anticipated that $25,000 of the billings would not be collected. d. Services to charity patients were $200,000 at established rates. 2. Inventories of $56,000 were purchased on credit. 3. Operating expenses were incurred as follows: Health care services. . . . . ... General expenses Administrative expenses... $2,140,000 $200,000 $90,000 Assume that all the expenses were incurred on credit. 4. The board decided to set aside $30,000 in cash in a separate account to provide for the continuing education of nurses. 5. The hospital entered into a capitation agreement with the county in which it was located, agree ing to provide hospital services to certain groups of county employees and their dependents. The agreement provided for the county to make a monthly payment for each covered county employee. Cash payments received by the hospital under this agreement were $300.000 6. Collections of patient receivables totaled $2.200,000. In addition, $13,000 of patient receivables were written off as uncollectible. 7. Payments of accounts payable totaled $1,900,000. 8. The use of inventories was recorded as follows: Health care services.... General expenses.... $30,000 $20,000 9. Depreciation was recorded as follows: building, $40,000; equipment, $50,000. 10. During the year, the hospital paid debt service of $220,000 on the outstanding bonds, consisting of interest of $120,000 and principal of $100,000. At year-end, the hospital made an entry to report $100,000 of its outstanding long-term debt as current. (Assume the debt was used to finance the purchase of the hospital's capital assets.) 11. During the year, a self-pay patient instituted legal action in the amount of $200,000 against the hospital for medical malpractice. The hospital does not carry insurance. Hospital attorneys have started negotiations with the claimant and believe it is highly probable that the claim can be settled for $50,000. (Charge the expense to Health care services.) 12. At year-end, the hospital reviewed its cost accounting records in connection with the retrospective billing arrangement made with the third-party payer in transaction 1.b. The hospital believes it will need to refund $40,000 to that third party in accordance with that agreement. (The third party had paid all the billings made by the hospital in 1.b.) Use the preceding information to do the following: a. Prepare all the journal entries necessary to record these transactions. b. Prepare a statement of revenues, expenses, and changes in net position for 2019. c. Prepare a balance sheet as of December 31, 2019