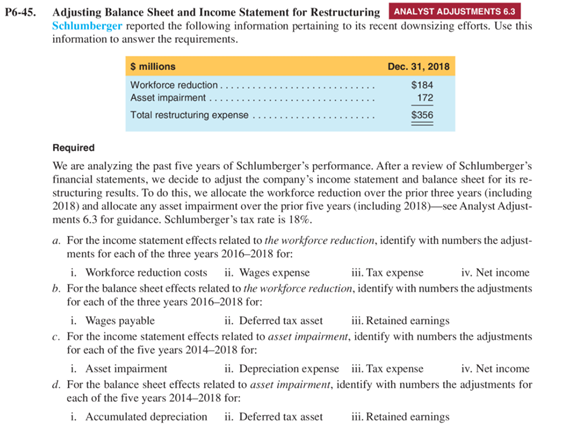

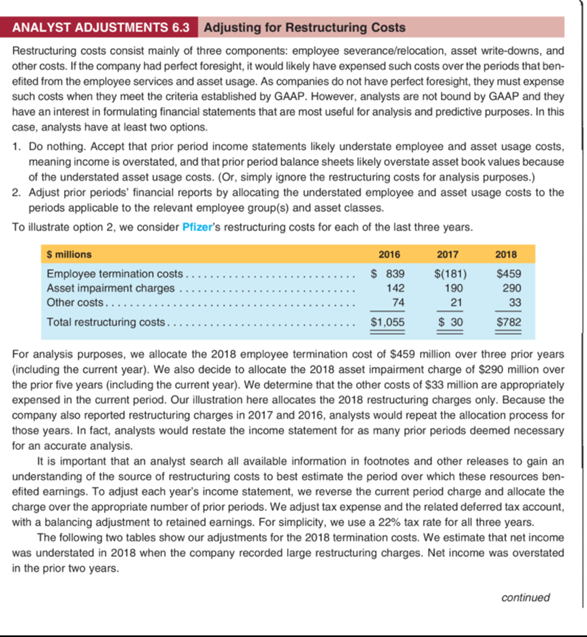

P6-45. Adjusting Balance Sheet and Income Statement for Restructuring ANALYST ADJUSTMENTS 6.3 Schlumberger reported the following information pertaining to its recent downsizing efforts. Use this information to answer the requirements. $ millions Dec. 31, 2018 Workforce reduction Asset impairment. 172 Total restructuring expenso $356 $184 Required We are analyzing the past five years of Schlumberger's performance. After a review of Schlumberger's financial statements, we decide to adjust the company's income statement and balance sheet for its re- structuring results. To do this, we allocate the workforce reduction over the prior three years (including 2018) and allocate any asset impairment over the prior five years (including 2018)-see Analyst Adjust- ments 6.3 for guidance. Schlumberger's tax rate is 18%. a. For the income statement effects related to the workforce reduction, identify with numbers the adjust- ments for each of the three years 2016-2018 for: i. Workforce reduction costs ii. Wages expense iii. Tax expense iv. Net income b. For the balance sheet effects related to the workforce reduction, identify with numbers the adjustments for each of the three years 2016-2018 for: i. Wages payable ii. Deferred tax asset iii. Retained earnings c. For the income statement effects related to asset impairment, identify with numbers the adjustments for each of the five years 2014-2018 for: i. Asset impairment ii. Depreciation expense iii. Tax expense iv. Net income d. For the balance sheet effects related to asset impairment, identify with numbers the adjustments for cach of the five years 2014-2018 for: i. Accumulated depreciation ii. Deferred tax asset iii. Retained earnings ANALYST ADJUSTMENTS 6.3 Adjusting for Restructuring Costs Restructuring costs consist mainly of three components: employee severance/relocation, asset write-downs, and other costs. If the company had perfect foresight, it would likely have expensed such costs over the periods that ben- efited from the employee services and asset usage. As companies do not have perfect foresight, they must expense such costs when they meet the criteria established by GAAP. However, analysts are not bound by GAAP and they have an interest in formulating financial statements that are most useful for analysis and predictive purposes. In this case, analysts have at least two options. 1. Do nothing. Accept that prior period income statements likely understate employee and asset usage costs, meaning income is overstated, and that prior period balance sheets likely overstate asset book values because of the understated asset usage costs. (Or, simply ignore the restructuring costs for analysis purposes.) 2. Adjust prior periods' financial reports by allocating the understated employee and asset usage costs to the periods applicable to the relevant employee group(s) and asset classes. To illustrate option 2, we consider Pfizer's restructuring costs for each of the last three years. S millions 2016 2017 Employee termination costs. $ 839 $(181) $459 Asset impairment charges. 142 190 290 Other costs.... 74 21 33 Total restructuring costs. $1,055 $ 30 $782 2018 For analysis purposes, we allocate the 2018 employee termination cost of $459 million over three prior years (including the current year). We also decide to allocate the 2018 asset impairment charge of $290 million over the prior five years (including the current year). We determine that the other costs of $33 million are appropriately expensed in the current period. Our illustration here allocates the 2018 restructuring charges only. Because the company also reported restructuring charges in 2017 and 2016, analysts would repeat the allocation process for those years. In fact, analysts would restate the income statement for as many prior periods deemed necessary for an accurate analysis. It is important that an analyst search all available information in footnotes and other releases to gain an understanding of the source of restructuring costs to best estimate the period over which these resources ben- efited earnings. To adjust each year's income statement, we reverse the current period charge and allocate the charge over the appropriate number of prior periods. We adjust tax expense and the related deferred tax account, with a balancing adjustment to retained earnings. For simplicity, we use a 22% tax rate for all three years. The following two tables show our adjustments for the 2018 termination costs. We estimate that net income was understated in 2018 when the company recorded large restructuring charges. Net income was overstated in the prior two years. continued