Answered step by step

Verified Expert Solution

Question

1 Approved Answer

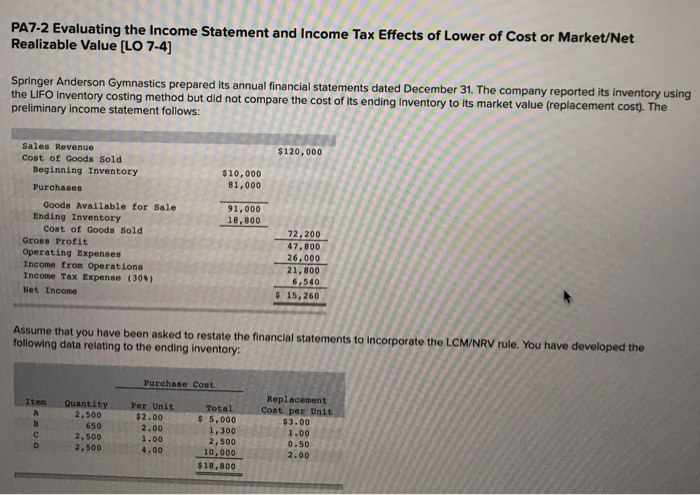

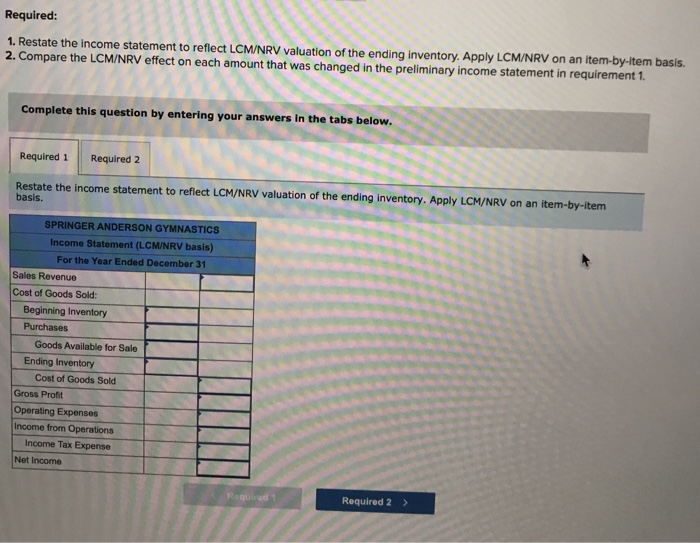

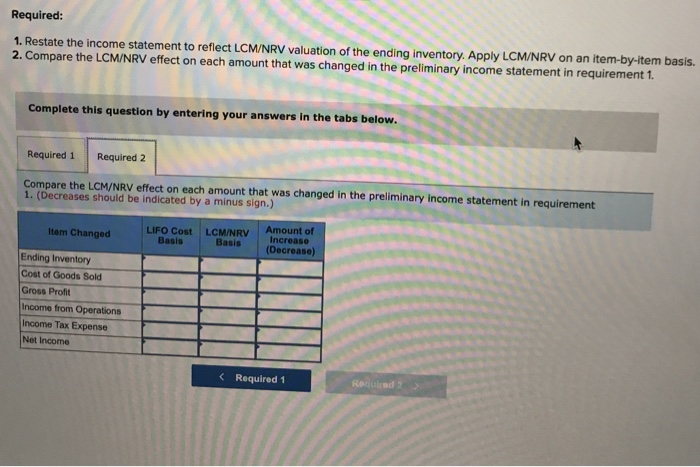

PA7-2 Evaluating the Income Statement and Income Tax Effects of Lower of Cost or Market/Net Realizable Value (LO 7-4) Springer Anderson Gymnastics prepared its annual

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

How To Do Energy Audit Of Your Home The Complete WorkBook For Young Mind

Authors: Pranab Nath

1st Edition

B0C2S47K82, 979-8391164623