Answered step by step

Verified Expert Solution

Question

1 Approved Answer

..par value of $1000, and selling at $1018. Assuming that one-year rates undergo a lognormal random walk with volatility s, and s is assumed to

..par value of $1000, and selling at $1018. Assuming that one-year rates undergo a lognormal random walk with volatility s, and s is assumed to be 12% . It is given that the one year spot rate is 5.03%.

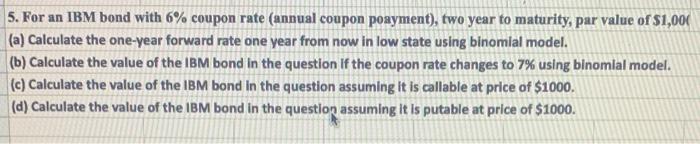

5. For an IBM bond with 6% coupon rate (annual coupon poayment), two year to maturity, par value of $1,000 (a) Calculate the one-year forward rate one year from now in low state using binomial model. (b) Calculate the value of the IBM bond in the question If the coupon rate changes to 7% using binomial model. (c) Calculate the value of the IBM bond in the question assuming It is callable at price of $1000. (d) Calculate the value of the IBM bond in the question assuming It is putable at price of $1000 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Multinational Business Finance

Authors: David K. Eiteman, Arthur I. Stonehill, Michael H. Moffett

10th Edition

0201785676, 9780201785678