Answered step by step

Verified Expert Solution

Question

1 Approved Answer

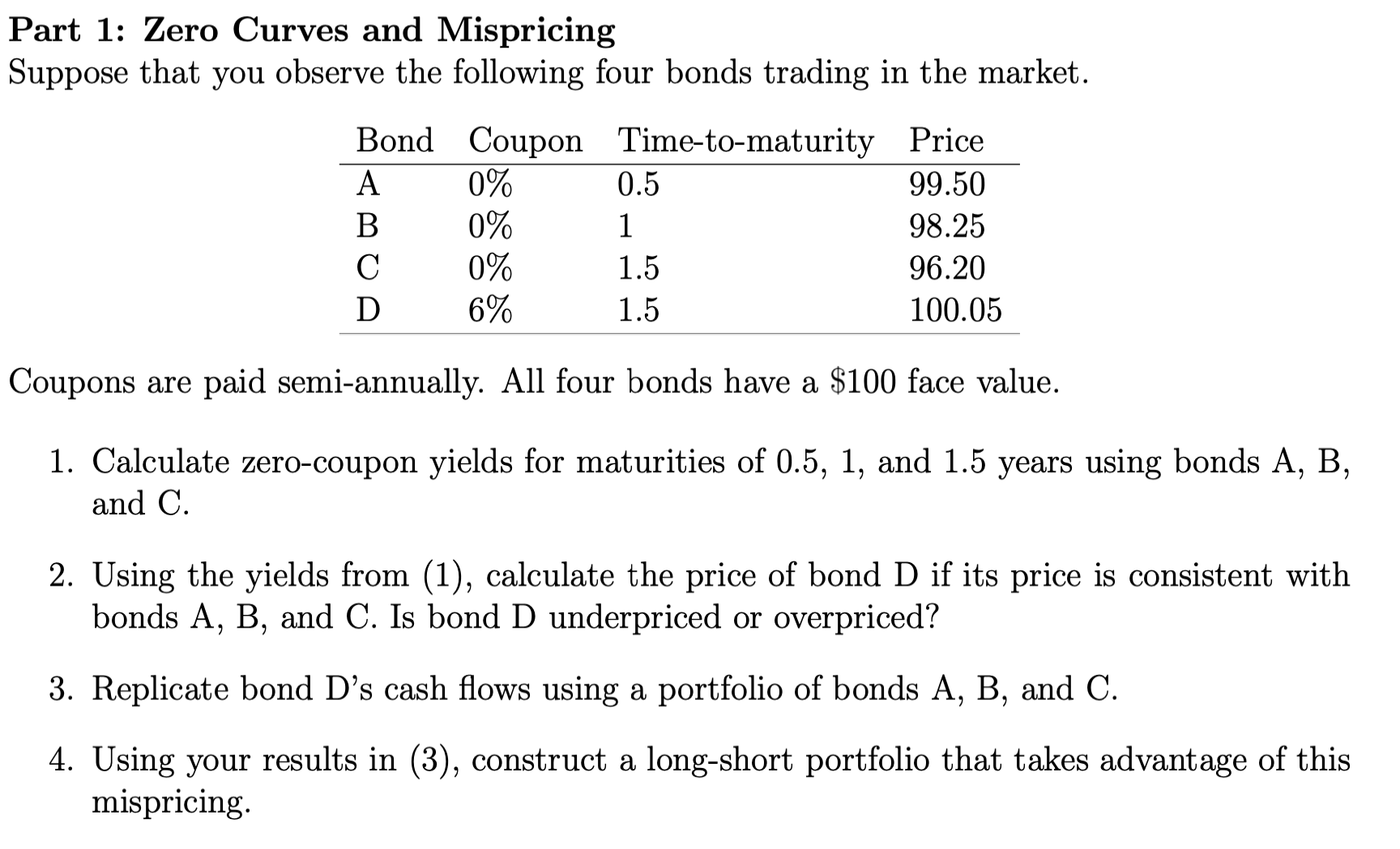

Part 1: Zero Curves and Mispricing Suppose that you observe the following four bonds trading in the market. Coupons are paid semi-annually. All four bonds

Part 1: Zero Curves and Mispricing Suppose that you observe the following four bonds trading in the market. Coupons are paid semi-annually. All four bonds have a $100 face value. 1. Calculate zero-coupon yields for maturities of 0.5,1, and 1.5 years using bonds A, B, and C. 2. Using the yields from (1), calculate the price of bond D if its price is consistent with bonds A,B, and C. Is bond D underpriced or overpriced? 3. Replicate bond D's cash flows using a portfolio of bonds A, B, and C. 4. Using your results in (3), construct a long-short portfolio that takes advantage of this mispricing

Part 1: Zero Curves and Mispricing Suppose that you observe the following four bonds trading in the market. Coupons are paid semi-annually. All four bonds have a $100 face value. 1. Calculate zero-coupon yields for maturities of 0.5,1, and 1.5 years using bonds A, B, and C. 2. Using the yields from (1), calculate the price of bond D if its price is consistent with bonds A,B, and C. Is bond D underpriced or overpriced? 3. Replicate bond D's cash flows using a portfolio of bonds A, B, and C. 4. Using your results in (3), construct a long-short portfolio that takes advantage of this mispricing

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Urban Public Finance

Authors: D. Wildasin

1st Edition

0415851882, 978-0415851886