Answered step by step

Verified Expert Solution

Question

1 Approved Answer

part 2 only Part 1 [worth 20 marks] Individual A has utility-of-wealth function U(W)=eW. a) Obtain an expression for individual A's coefficient of absolute risk

part 2 only

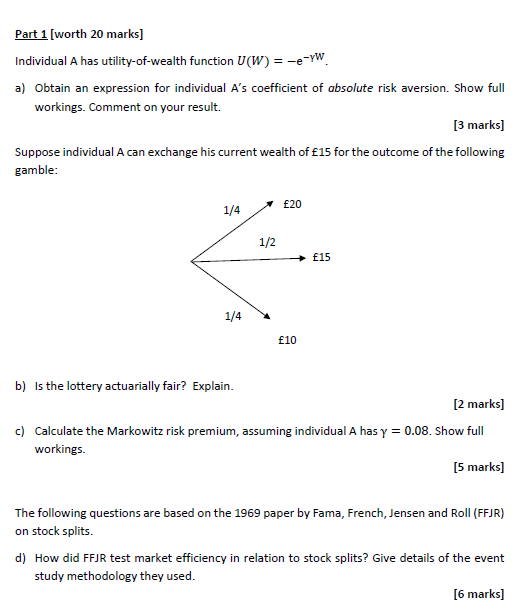

Part 1 [worth 20 marks] Individual A has utility-of-wealth function U(W)=eW. a) Obtain an expression for individual A's coefficient of absolute risk aversion. Show full workings. Comment on your result. [3 marks] Suppose individual A can exchange his current wealth of f15 for the outcome of the following gamble: b) Is the lottery actuarially fair? Explain. [2 marks] c) Calculate the Markowitz risk premium, assuming individual A has =0.08. Show full workings. [5 marks] The following questions are based on the 1969 paper by Fama, French, Jensen and Roll (FFJR) on stock splits. d) How did FFJR test market efficiency in relation to stock splits? Give details of the event study methodology they used. [6 marks] The following questions are based on the 1969 paper by Fama, French, Jensen and Roll (FFJR) on stock splits. d) How did FFJR test market efficiency in relation to stock splits? Give details of the event study methodology they used. [6 marks] (Question 4 continues on the next page) Page 11 of 15 IB2350_B e) FFJR find evidence that the announcement of a stock split: (i) is associated with negative abnormal returns; and (ii) supports the strong form efficiency hypothesis. For each of (i) and (ii), explain whether the statement is true or false. t 2 [worth 20 marks] Use the Black Scholes formula to answer the following: (i) Draw a graph illustrating how the value of a European call option with strike price X and time to expiry T depends on the current value S of the underlying asset. Give a formula for the lower bound of this European call option and add this to the graph. [3 marks] (ii) Draw a graph illustrating how the value of a European put option with strike price X and time to expiry T depends on the current value S of the underlying asset. Give a formula for the lower bound of this European call option and add this to the graph. [3 marks] (iii) Derive the limits of the Black-Scholes formula for a European call option as the option becomes more and more deeply in-the-money. (Hint: calculate the limit as the moneyness ratio tends to infinity). What happens to the risk-neutral probability of exercise for the European call in this case? [3 marks] (iv) Derive the limits of the Black-Scholes formula for a European put option as the option becomes more and more deeply in-the-money. (Hint: use put-call parity to determine the Black-Scholes formula for a European put, and calculate the limit as the moneyness ratio tends to zero). What happens to the risk-neutral probability of exercise for the European put in this case? [3 marks] Part 1 [worth 20 marks] Individual A has utility-of-wealth function U(W)=eW. a) Obtain an expression for individual A's coefficient of absolute risk aversion. Show full workings. Comment on your result. [3 marks] Suppose individual A can exchange his current wealth of f15 for the outcome of the following gamble: b) Is the lottery actuarially fair? Explain. [2 marks] c) Calculate the Markowitz risk premium, assuming individual A has =0.08. Show full workings. [5 marks] The following questions are based on the 1969 paper by Fama, French, Jensen and Roll (FFJR) on stock splits. d) How did FFJR test market efficiency in relation to stock splits? Give details of the event study methodology they used. [6 marks] The following questions are based on the 1969 paper by Fama, French, Jensen and Roll (FFJR) on stock splits. d) How did FFJR test market efficiency in relation to stock splits? Give details of the event study methodology they used. [6 marks] (Question 4 continues on the next page) Page 11 of 15 IB2350_B e) FFJR find evidence that the announcement of a stock split: (i) is associated with negative abnormal returns; and (ii) supports the strong form efficiency hypothesis. For each of (i) and (ii), explain whether the statement is true or false. t 2 [worth 20 marks] Use the Black Scholes formula to answer the following: (i) Draw a graph illustrating how the value of a European call option with strike price X and time to expiry T depends on the current value S of the underlying asset. Give a formula for the lower bound of this European call option and add this to the graph. [3 marks] (ii) Draw a graph illustrating how the value of a European put option with strike price X and time to expiry T depends on the current value S of the underlying asset. Give a formula for the lower bound of this European call option and add this to the graph. [3 marks] (iii) Derive the limits of the Black-Scholes formula for a European call option as the option becomes more and more deeply in-the-money. (Hint: calculate the limit as the moneyness ratio tends to infinity). What happens to the risk-neutral probability of exercise for the European call in this case? [3 marks] (iv) Derive the limits of the Black-Scholes formula for a European put option as the option becomes more and more deeply in-the-money. (Hint: use put-call parity to determine the Black-Scholes formula for a European put, and calculate the limit as the moneyness ratio tends to zero). What happens to the risk-neutral probability of exercise for the European put in this case? [3 marks]Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Sustainable Finance

Authors: Dirk Schoenmaker, Willem Schramade

1st Edition

0198826605, 978-0198826606